Airbnb entered the third quarter with a clear mission: accelerate growth while strengthening its position as one of the most profitable companies in global travel. The results show a company operating at full momentum. Revenue and bookings grew faster than expected, margins expanded to record levels, and user engagement continued to rise, powered by a strong mobile ecosystem and improved personalization. Q3 ultimately became one of the most profitable quarters in Airbnb’s history.

At the same time, Airbnb is laying the foundations for a much broader transformation. The introduction of AI-powered tools, expansion beyond traditional lodging, and early steps toward building social layers into the platform signal a long-term ambition to redefine what a travel marketplace can be. Combined with exceptionally strong free cash flow, these developments reinforce the company’s position as one of the most resilient and forward-looking players in the sector.

How was the last quarter?

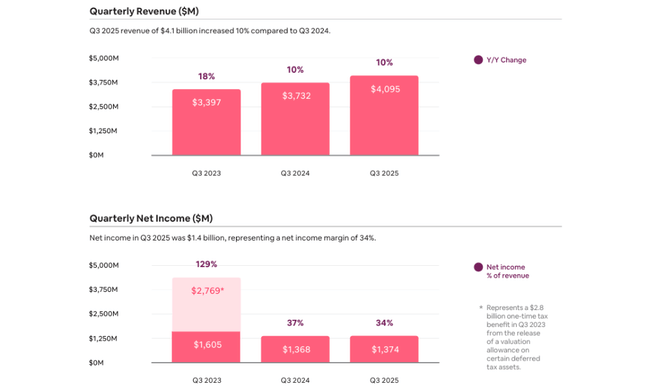

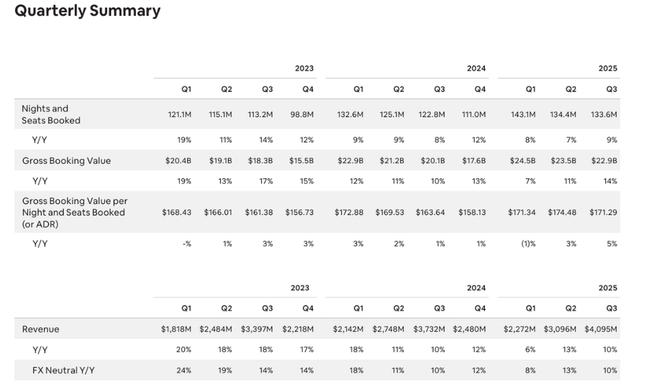

Airbnb $ABNB entered the third quarter with an ambition to accelerate growth after several quarters where comparative fundamentals made it difficult to interpret developments. However, the results showed that the platform is on solid footing. Revenues of nearly $4.1 billion represent solid double-digit growth in an environment where global travel demand is gradually normalizing. Airbnb has been able to combine steady growth in bookings with a modest increase in average nightly rate, while changes in product mix - the growing importance of longer stays and a higher proportion of mobile bookings - have contributed positively to improved overall monetisation.

One of the strongest signals is the development of Gross Booking Value, i.e. total bookings, which increased by 14% year-on-year. This growth not only outpaces revenue growth, but also demonstrates that Airbnb still has significant room for expansion in key regions. The fastest growing markets were outside of North America, which posted double-digit year-over-year growth in Nights & Seats Booked. In addition to traditionally strong Europe, the situation in Asia improved significantly, where new features, localised marketing campaigns and flexible payment options are increasing penetration.

It was an exceptional period in terms of profitability. Adjusted EBITDA reached a record $2.1 billion and margins of 50% are now among the highest in the global technology sector. This confirms that Airbnb's model has enormous operating leverage: new bookings are delivering significantly higher margins than traditional OTA platforms because the fixed cost base is not growing at the same rate as transaction volume. Investments in customer support automation have also had a positive impact, with the new AI-assistant significantly reducing the demands on human operators.

The cash flow profile has also improved strongly. Free cash flow of $1.3 billion clearly shows that the company is generating capital in excess of investment needs. This provides it with high flexibility to fund growth in new verticals (Services & Experiences), potential acquisitions and when considering future capital return programs. The fact that the travel player's FCF margin is 33% is unique to the sector.

Product enhancements have also been significant. The 'Reserve Now, Pay Later' option has led to an immediate increase in bookings, particularly among younger users. Updated cancellation policies reduce barriers to booking and increase trust on both sides of the transaction. Improved mapping cues deliver higher conversion and flexible carousels allow relevant offers to be displayed outside of the original guest filter. All of this has translated into a strong rebound in organic demand.

Management commentary

Management (CEO Brian Chesky) emphasizes four main priorities: product improvement, expansion into new markets, broadening the offering, and deep integration of artificial intelligence. Features Reserve Now, Pay Later has significantly increased the number of bookings and will be further scaled globally. Changes to cancellation policies reduce booking barriers and improve conversion, while new mapping cues and flexible search results bring more relevant options to guests.

A strategy to diversify beyond the accommodation itself is also evident. Airbnb Experiences & Services attract not only new hosts, but also users who do not use accommodation services. This creates a new growth vertical that can change the revenue structure in the long term. At the same time, the company is moving strongly towards AI-native platformthat will personalise search, provide instant support and, in the future, allow users to plan their journey in a conversational way.

Outlook

- Revenue: USD 2.66-2.72 billion

- Year-on-year growth 7-10 %, slight positive FX effect - GBV: Growth low-double-digits year-on-year

- driven by higher price level (ADRs) and a steadily increasing number of bookings - Nights & Seats Booked: Growth mid-single-digits

- Significantly challenging comparative base after strong Q4 2024 - Implied take-rate: YoY stable, no major changes

- Profitability: Adjusted EBITDA will be approximately flat or slightly lower year-over-year,

as Airbnb invests in new features and development of Experiences and services.

Long-term results

Airbnb's long-term development shows the structural transformation of the platform from a pure growth player into one of the most efficient and profitable digital companies in the world. Revenues have grown at a consistent rate since 2021, reaching $11.1 billion in 2024, representing nearly 12% growth. This development is all the more remarkable given that the company has had to absorb the normalization of pandemic peak demand, tightening regulation in some major cities, and increased competitive pressure in key markets.

Meanwhile, the cost structure has improved significantly. Gross profit rose to $9.2 billion, and its growth far outpaced that of cost of sales. This confirms that both technology investments and process automation are lifting the platform's operational efficiency. Over the past few years, Airbnb has overhauled its internal infrastructure, improved antifraud systems, and deployed AI in both support and recommendation algorithms - and these steps are now delivering long-term margin improvements.

Operating profit rose to $2.55 billion in 2024, up 68% year-over-year. This result is due to a combination of savings, higher monetization of the service, a strong global brand and a shift in user behavior as they increasingly use the mobile app. EBITDA of $2.62 billion represents a significant shift from earlier years, when the company was just stabilizing its post-pandemic model and facing increased investment demands.

Today, Airbnb is a company with a very clean capital profile: reasonable debt, no significant equity investments, a stable number of shares outstanding and a high level of cash flow generated. This is a fundamental difference from traditional travel companies that carry high fixed costs in the form of property, aircraft or hotel infrastructure. Airbnb's platform model is one of the most efficient in the entire consumer sector in terms of return on capital.

News

- Global feature launch Reserve Now, Pay Laterwhich significantly boosted conversions in the US.

- Expansion of cancellation policy with a positive impact on customer experience and support utilization.

- New social features - Who's Going, Connections, direct messaging between Experiences participants.

- AI-assistant can resolve a portion of requests in seconds and reduces operator intervention by 15%.

- More than 110,000 new host requests for Experiences & Services.

- Local growth campaigns in Brazil, Korea and Japan resulted in double-digit increases in bookings.

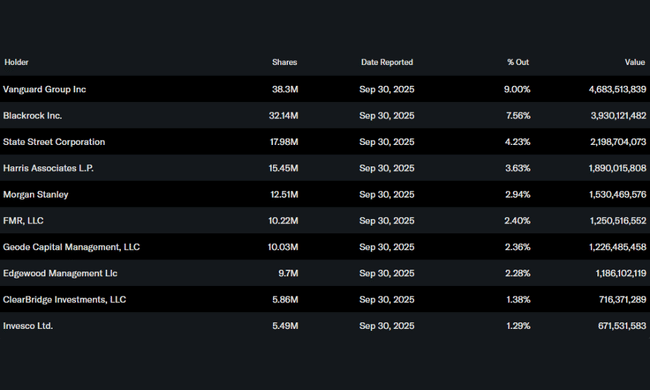

Shareholding structure

Institutional shareholding exceeds 85%, which is typical of strongly established technology companies. The largest shareholdings are held by:

- Vanguard Group - 9.00%

- BlackRock - 7.56%

- State Street - 4.23%

- Harris Associates - 3.63%

The stable institutional base provides long-term support for the stock.

Analyst expectations

DA Davidson reaffirmed the recommendation Buy for Airbnb stock and set a price target of $155, representing nearly 27% potential upside from current levels. The analysts highlight the extremely rapid growth of Airbnb's new Services division , which was only officially launched in May 2025. The number of available services in the 84 cities tracked is up 129% since June and 81% since September, with supply already slightly outpacing Experiences. This segment is growing fastest in the US and Europe, where Services already significantly outperform Experiences.