Disney closes fiscal 2025 as a fundamentally reshaped company, one that dokázal zvýšit profitability even in a quarter of flat revenue. The fourth quarter shows a business driven less by box-office volatility and more by stable, repeatable cash engines: parks, streaming and live sports. While revenue held steady at 22.5 billion dollars, operating income more than doubled and EPS expanded at a pace that would ještě před rokem působilo nepravděpodobně. For investors, it signals a company that finally nachází rovnováhu mezi kreativní produkcí a provozní efektivitou.

Beneath the headline numbers, Disney’s internal architecture is changing. Parks and Experiences continue to hit all-time highs thanks to global demand and disciplined reinvestment, streaming has entered a sustainable profit track, and ESPN’s stabilization brings long-awaited clarity to the sports segment. With segment operating income up 12 % for the full year and cash generation meaningfully stronger, Disney enters FY26 as a more predictable, more profitable and strategically focused enterprise než v jakékoli fázi poslední dekády.

How was the last quarter?

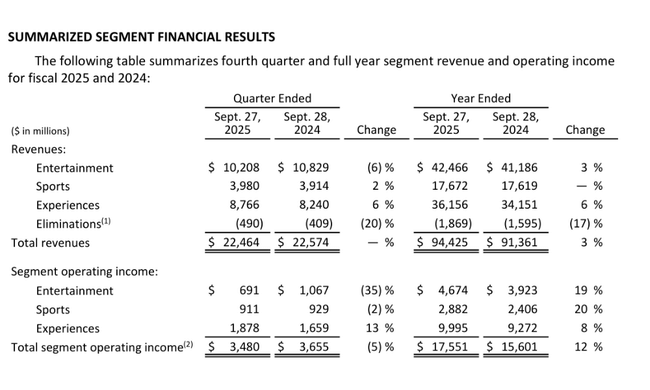

The fourth quarter of fiscal 2025 can be characterized as a period of stable sales but significantly higher profitability. Revenue of $22.5 billion was virtually comparable to Q4 2024, but pre-tax profit more than doubled to $2.0 billion. Total segment operating profit was down 5% year-on-year to $3.5 billion, reflecting a challenging comparative period, particularly in film distribution, but the bottom line benefited from improved efficiencies and business mix. Diluted EPS in the quarter jumped from $0.25 to $0.73, with adjusted EPS of $1.11, just 3% below the very strong Q4 2024.

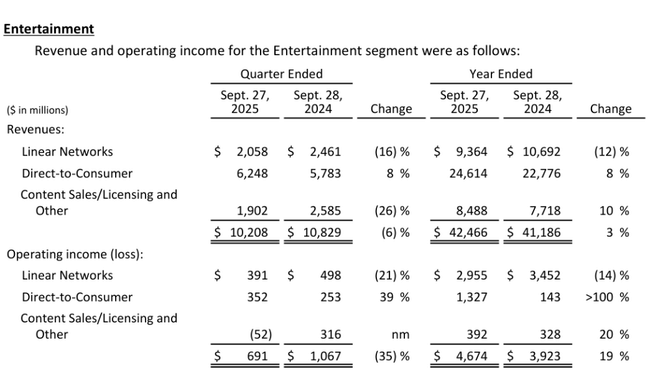

From a segment perspective, Q4 was mixed, but the overall picture for investors remains favorable. Entertainment took a noticeable hit due to tough comparisons to last year's record movie line-up, with the hugely successful titles Inside Out 2 and Deadpool & Wolverine entering the results. Entertainment's segment operating profit for the quarter was $691 million, down $376 million from a year ago. On the other hand, Direct-to-Consumer streaming continued its surprisingly rapid improvement, with DTC sales up 8% year-over-year (despite a roughly two-point negative impact from last year's inclusion of Disney+ Hotstar) and operating profit up $99 million to $352 million. Disney+ and Hulu together already have 196 million subscribers, up 12.4 million from the third quarter, with Disney+ alone adding 3.8 million to 132 million subscribers.

The sports segment remained relatively stable. Operating profit was $911 million, only slightly below last year's level, when higher marketing and programming costs outweighed growth in advertising and subscription revenue. Domestic ESPN reported a 3% decline in operating profit, but domestic advertising revenue grew 8%, a positive signal for the monetization of sports rights. The real driver of the quarter was Experiences. This division reported a record Q4 operating profit of $1.9 billion, up $219 million from last year. International Parks and Experiences increased profits 25% to $375 million, while Domestic Parks increased 9% to $920 million. Thus, from a portfolio-wide perspective, Disney has shown that even without extraordinary blockbusters, it can generate high profits, lean on growing parks and move streaming into the profitable phase.

CEO commentary

Bob Iger in his comments, emphasized that fiscal 2025 was another year of substantial strength for the company. He said Disney $DIS is successfully capitalizing on its creative and brand assets across its entire ecosystem - from theaters and TV channels to streaming to parks and experiences - while making tangible progress in turning its direct-to-consumer business into a profitable pillar. Iger's strategy is built on a combination of complementary businesses and a strong balance sheet that allows the company to continue to invest in premium content and experiences while increasing return on capital for shareholders.

The CEO also clearly articulated that the goal is not just short-term margin improvement, but more importantly, long-term anchoring of Disney in a new era of the entertainment industry dominated by streaming platforms, global franchises and the experience economy. Iger highlighted Experiences' record performance, DTC's gradual transition into a profitable business, and the fact that Disney has a unique portfolio of brands and IP that can be monetized across multiple channels. It is clear from his words that management is confident in the company's ability to sustain double-digit earnings growth in the years ahead.

Outlook

The outlook for fiscal 2026 and 2027 is ambitious but backed by concrete numbers and clearly defined milestones. For Q1 of fiscal year 2026, Disney expects DTC SVOD operating profit of around $375 million, confirming that streaming is no longer a "black hole" for capital but is becoming a regular contributor to profitability. On the other hand, the Entertainment segment will face a roughly $400m negative impact in Q1 due to weaker comparative movie releases, lower political ads (down $140m from last year) and also the absence of a contribution from Star India, which generated $73m of operating profit in Q1 last year. Experiences will be saddled with approximately $150 million of pre-opening and dry dock costs in the Disney Cruise Line division in the early part of the year.

For the full fiscal year 2026, management is targeting double-digit percentage growth in segment operating profit in Entertainment, weighted more toward the second half of the year, while achieving roughly 10% operating margin in DTC SVOD. Sports should grow in the low single-digit percentages, with the largest contribution expected in the fourth quarter due to the timing of sports rights costs. Experiences should add high single-digit percentage earnings despite $160 million of pre-opening costs and $120 million of dry dock costs. The company plans $24 billion of content investment across Entertainment and Sports, roughly $19 billion of operating cash flow, $9 billion of capex and a doubling of share buybacks to $7 billion. The dividend for 2026 will be $1.50 per share in two installments of $0.75. For fiscal 2027, Disney then expects another double-digit growth in adjusted EPS, underscoring management's confidence in its long-term profitability trajectory.

Long-term results

The long-term trend in Disney $DISresults shows a company that is successfully adapting to structural changes in the industry. Revenues have increased at a steady pace in recent years, reaching $94.4 billion in 2025, up 3.35% from 2024 and nearly 14% from 2022. The more significant change comes at the margin level. Gross profit is up more than 9% to $35.7 billion in 2025, while operating profit is up 16% to $13.8 billion. This builds on double-digit growth in previous years and points to a structural shift in profitability, driven largely by a more efficient mix between traditional TV channels, streaming and parks.

Most telling, however, is the evolution of net income and earnings per share. Net income has grown from $2.35 billion in 2023 to $4.97 billion in 2024 and to $12.4 billion in 2025. Diluted EPS has moved from $1.29 to $2.72 to $6.85 in two years, more than five times 2023 levels. In addition to higher operating profitability, tax factors also played a role, with a significant change in the tax burden in 2025, turning a positive levy in previous years into a tax benefit. EBITDA increased from roughly $12.0 billion to $19.1 billion over the 2022-2025 period, illustrating the company's strengthening cash-flow profile. The number of shares outstanding has been declining slightly over time, supporting EPS growth and showing that Disney is beginning to rely on share buybacks again as part of its return on capital.

News

In terms of strategic direction, fiscal 2025 brought several key highlights. The most notable is a clear shift in streaming - DTC SVOD gradually moved into the profit zone during the year, and Disney openly communicates targeting double-digit operating margins in the coming years. The growth in the total subscriber base to 196 million, coupled with tighter pricing and a focus on ARPU, shows that a model built on premium content and strong brands is working. At the same time, the company has completed transactions around Star India, which reduces the contribution of some linear channels in the short term, but helps to clean up the portfolio and focus on more profitable segments in the long term.

Accelerating capital allocation towards shareholders is also significant news. Disney has raised and stabilized its dividend, doubled its planned share repurchases to $7 billion for fiscal 2026, and further strengthened its cash-flow profile, with free cash flow for 2025 reaching over $10 billion. The Experiences division, including parks, resorts and cruise line, has established itself as a steady growth engine with record earnings, yet the company continues to invest in new Disney Adventure and Disney Destiny ships, which are expected to deliver further capacity and revenue growth in the coming years.

Shareholding structure

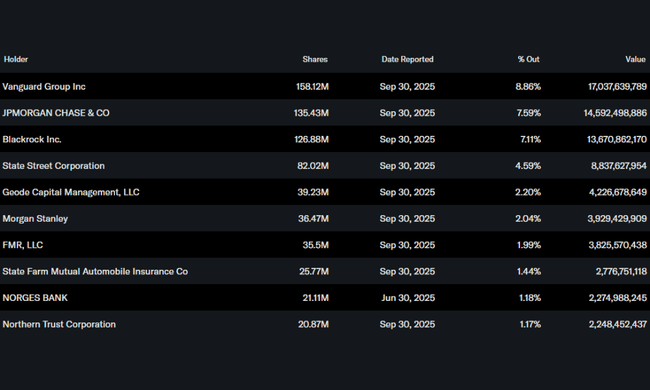

Disney's shareholder structure is distinctly institutional. Insiders hold only roughly 0.07% of the company's shares, while institutions control approximately 75.7% of all shares and virtually the same proportion of the free float. This confirms that Disney is a core position in the portfolios of many large global investors. The largest shareholder is Vanguard Group with approximately 8.86%, followed by JPMorgan Chase with 7.59%, BlackRock with 7.11% and State Street with 4.59%. In total, nearly four thousand institutional investors hold shares of the company. Such a concentrated and institutional ownership structure is common for large blue-chip companies and suggests a high degree of professional capital confidence in the long-term Disney story.

Analysts' expectations

BofA Securities reiterated its Buy rating on the stock. and $140.00 price target on the entertainment giant. The company has forecast double-digit growth in adjusted earnings per share for fiscal 2026, driven by low single-digit operating earnings growth in Sports, double-digit operating earnings growth in Entertainment, and high single-digit operating earnings growth in Experiences.