Nvidia’s latest quarter confirms something investors were still quietly questioning: the company is no longer just riding an AI wave — it is defining the infrastructure cycle itself. Revenue expansion is now happening at a scale where most large-cap tech firms would inevitably slow down. Nvidia did not. Instead, it accelerated, proving that hyperscalers, sovereign AI projects, and enterprise platforms are still competing for capacity faster than supply can realistically expand.

What makes this phase different is not just demand, but quality of earnings. Margins remain structurally elevated, capital intensity is being absorbed without stress, and cash generation is reaching levels that fundamentally change Nvidia’s financial flexibility. This is no longer a growth story driven by anticipation. It is a cash machine operating at full load, with visibility that stretches well beyond a single product cycle.

How was the last quarter?

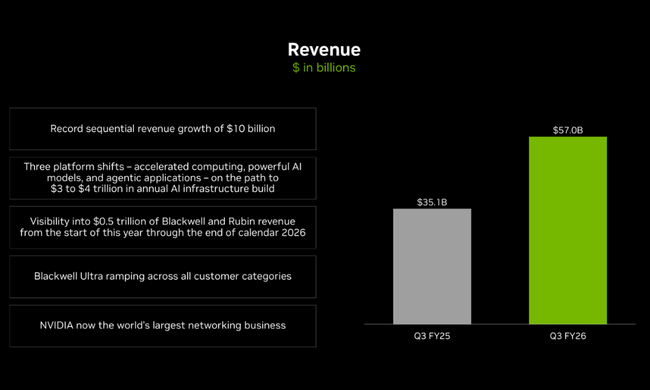

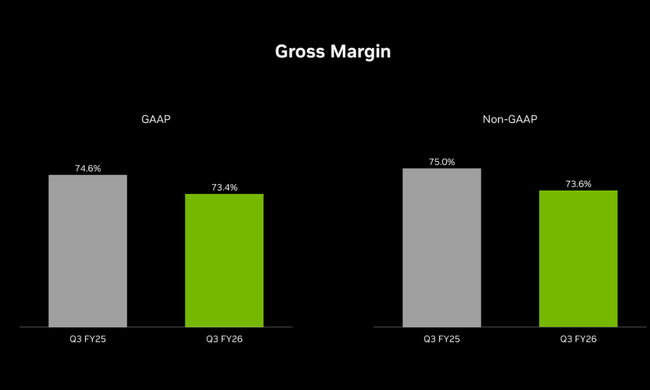

From a purely numerical perspective, Q3 was another record quarter. But more important is the pace and quality of growth. Revenues of $57.0 billion were more than $10 billion higher than the previous quarter and nearly $22 billion higher than a year ago. Such rapid growth in absolute terms is exceptional for a company of this size. Yet gross margin remains near all-time highs - 73.4% on a GAAP basis and 73.6% on a non-GAAP basis. While margins are down slightly year-over-year, they have improved quarter-over-quarter, which is important in a period of massive ramp-up of a new generation of products.

Profitability grew even faster than revenue. Operating profit was $36.0 billion, up 65% year-on-year and 27% quarter-on-quarter. Net profit of $31.9 billion was 21% higher than Q2 and also 65% higher than a year ago. Earnings per share of $1.30 represented growth of 20% from last quarter and 67% year-over-year. On the positive side, GAAP and non-GAAP EPS are virtually identical, which increases confidence in the quality of the reported results.

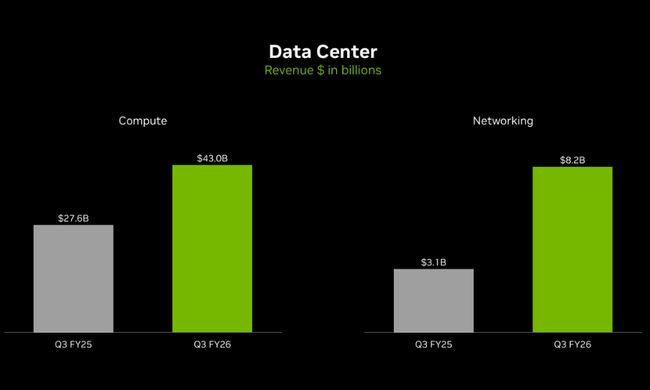

The main driver remains the datacenter segment. Revenues of $51.2 billion are up 25% vs. Q2 and 66% YoY. In other words, NVIDIA added more than $10 billion in sales in this segment alone in the three months. CEO Jensen Huang commented bluntly that Blackwell sales are "off the chart" and cloud GPUs are sold out. This clearly shows that the main limit to growth is not demand, but available production capacity, giving the company a strong bargaining position going into the next quarters.

The other segments today operate more as a complement to AI infrastructure, but their development remains solid. Gaming brought in $4.3 billion, slightly weaker quarter-over-quarter but up 30% year-over-year. Professional Visualization reached $760 million, very strong quarter-over-quarter and year-over-year growth. The Automotive segment reported $592 million and continues to deliver consistent growth that reinforces NVIDIA's long-term optionality in autonomy, robotics, and physical AI.

On the cost side, the company continues to invest aggressively, but operating leverage remains exceptionally strong. Operating expenses grew at a double-digit rate, but relative to revenue and operating profit, this is a clear demonstration of the scalability of the business. At the same time, NVIDIA continues to make massive share buybacks. In the first nine months of the year, it returned $37 billion to shareholders and still has more than $62 billion under authorization.

CEO commentary

Jensen Huang emphasized in his comments that NVIDIA has entered what he called the "virtuous cycle of AI." The demand for computing power is self-reinforcing, he said, as AI rapidly expands into other industries, regions and application types. Importantly, both training and inference workloads are growing exponentially, making AI a long-term infrastructure investment, not a one-off technology experiment.

Huang also made it clear that Blackwell is not just the next generation of chips, but a fundamental platform leap. The sell-out of cloud GPUs and the push for capacity confirm that NVIDIA remains a key infrastructure supplier for hyperscalers, AI labs and government projects.

Outlook

The outlook for the fourth quarter suggests further acceleration. NVIDIA expects revenue of around $65 billion, another significant increase from an already record Q3. Gross margins should move even higher, to around 75%, which combined with growing volume is a very strong signal. Operating costs are set to continue to rise, reflecting investment in platform, ecosystem and manufacturing, but the guidance structure suggests that operating leverage will remain.

For investors, it is key that the company is simultaneously increasing sales and margins. This typically means an improving product mix, a strong pricing position and a gradually stabilising supply chain. If NVIDIA delivers on this outlook, the thesis that Blackwell represents a long-term highly profitable platform, not a short-term cycle, will be confirmed.

Long-term results

The long-term view shows an extreme shift in the company's scale and profitability. Revenues for 2024 reached $60.9 billion, more than double from 2023 and nearly quadruple from 2021. Gross profit rose to $44.3 billion and operating profit to nearly $33 billion. The net profit of $29.8 billion shows how dramatically the company's economics have changed in a very short period of time.

The evolution of costs is also crucial. While revenues grew by more than 125% in 2024, operating expenses remained almost unchanged. This is a prime example of operating leverage and one of the main reasons why NVIDIA has become the most profitable company of the AI era. In addition, the share count has been declining slightly over the long term, increasing the impact of earnings growth on EPS.

News

The third quarter was packed with strategic announcements. NVIDIA confirmed that Blackwell is delivering top results in independent benchmarks and delivering significant improvements in power efficiency. The strategic partnership with OpenAI, which envisions deploying a minimum of 10 GW of NVIDIA systems, significantly increases long-term demand visibility. Also important is Anthropic's decision to scale its models on NVIDIA infrastructure.

The company is also deepening integration with cloud players, expanding the networking layer, strengthening the role of NVLink as a standard, and entering the areas of quantum and physical AI systems. These moves move NVIDIA from its role as a chip supplier to a comprehensive infrastructure partner.

Shareholder Structure

NVIDIA's shareholder structure is highly institutional. Approximately 69% of shares are held by institutions and more than 72% of the free float is held by professional investors. The largest shareholders include Vanguard, BlackRock, Fidelity and State Street. The company's stock is held by nearly 7,000 institutions, confirming its position as a key global position in both index and actively managed portfolios.

Analyst expectations

Following these results, analysts are primarily focused on the sustainability of the pace of data center growth, the evolution of margins in the Blackwell era, and the company's ability to increase supply in an environment where demand is outpacing supply. Guidance for Q4 pushes expectations higher again and supports the narrative that AI infrastructure investments are not a short-term boom but a multi-year cycle.

If NVIDIA continues to deliver results of this type, the market consensus will increasingly lean towards the view that the company is not just a winner of one technology wave, but a key building block of the new digital infrastructure.