Agricultural demand is cooling, and Deere is no exception. Farmers are delaying equipment upgrades, construction activity is moderating, and order books no longer reflect the urgency seen during the post-pandemic boom. Yet what stands out this quarter is not the slowdown itself, but how little damage it has done to Deere’s underlying economics so far.

Margins remain resilient, cash generation is still strong, and management continues to prioritize pricing discipline over volume chasing. Instead of forcing growth, Deere is clearly positioning itself for the next phase of the cycle—protecting profitability now, preserving balance sheet flexibility, and ensuring that when demand returns, it does so into a structurally stronger business than before.

How was the last quarter?

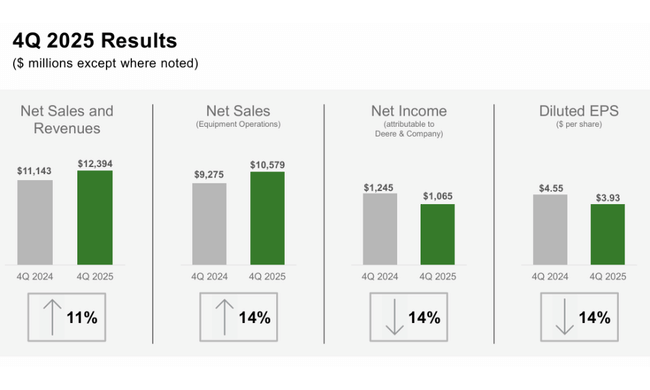

The fourth fiscal quarter of 2025 delivered $DE lower year-over-year profitability, reflecting cooling demand, particularly in the large agricultural equipment segment. Net income was $1.065 billion, compared to $1.245 billion in the same period last year. Earnings per share thus fell from USD 4.55 to USD 3.93. This development is in line with market and management expectations, which have repeatedly warned throughout the year of a gradual weakening of commodity prices and pressure on farmers' investment activity.

However, at the revenue level, the quarter showed relative stability. Total sales and earnings rose 11% year-on-year to USD 12.4 billion, with net sales reaching USD 10.6 billion. This suggests that despite the cyclical downturn, demand in some segments, particularly in the smaller agriculture and construction sectors, remains solid. The company also benefited from geographic diversification and a broader customer base.

Discipline on the cost side was an important element of the quarter. While margins faced pressure, Deere was able to maintain operating efficiencies through production optimization, inventory management and an emphasis on a Smart Industrial operating model. This allowed the company to get through the quarter without significant cash flow erosion, which is key in a down cycle.

CEO commentary

CEO John May called fiscal 2025 one of the most challenging fiscal years in recent memory, but also emphasized that the company achieved "the best results for this phase of the cycle." He said the structural changes Deere has implemented in recent years, particularly greater manufacturing flexibility, a stronger link to services and technology, and better working with capital, have taken full effect.

May reiterated that the goal is not to maximize volumes at any cost, but to protect return on capital and long-term shareholder value. This approach is evident not only in the results, but also in the cautious tone of the outlook, which reflects the realities of the market without undue optimism.

Outlook

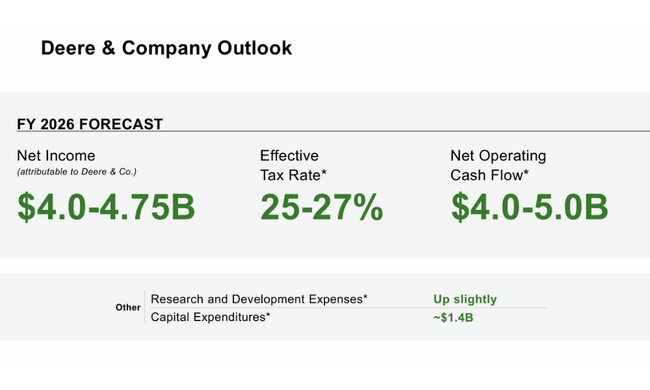

For fiscal 2026, management expects net income to be in the range of $4.0 billion to $4.75 billion, which would represent a further year-over-year decline from fiscal 2025. This outlook is based on the assumption that the large agricultural equipment segment will be near a cyclical low in 2026, while the smaller agriculture, turf and construction segments should gradually show signs of improvement.

The firm also notes continued pressure on margins due to tariffs, higher costs and geopolitical risks. On the other hand, it is betting on tight inventory control, limited capital expenditure and continued operational improvements to cushion the negative impact of weaker demand. Management expects 2026 to represent a stabilization phase rather than a return to growth.

Long-term results

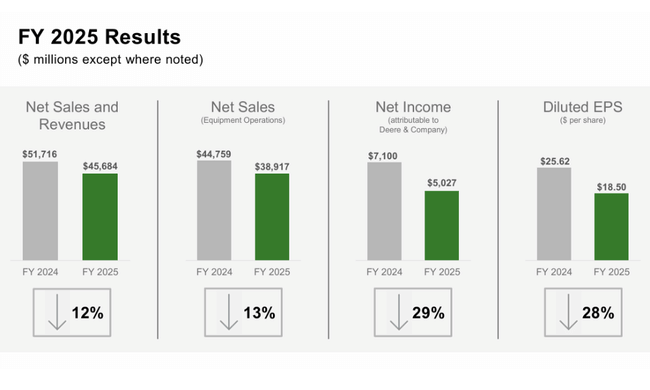

Looking at a longer time series, it is apparent how significantly Deere's results have fluctuated with the cycle in recent years. Fiscal 2024 brought a decline in sales to $50.5 billion from the previous $60.2 billion, clearly showing a retreat from record levels. Profitability declined even more sharply, with net income down more than 30% year-over-year to $7.1 billion and EPS falling from $34.8 to $25.7.

But at the same time, the long-term data shows that even after this decline, Deere remains structurally stronger than in previous cycles. Both operating profit and EBITDA are still well above 2021-2022 levels, suggesting that the company has been able to move its performance base higher. Higher contributions from software, services, precision farming and better pricing discipline are playing a significant role.

Shareholding structure

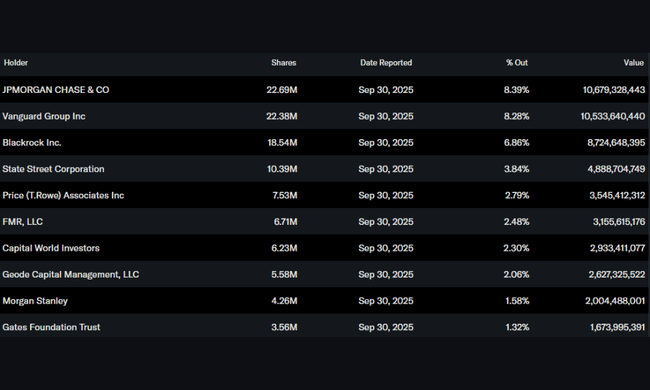

Deere's shareholder structure is stable and strongly institutional. The institution holds approximately 83% of the stock, with JPMorgan Chase, Vanguard, BlackRock and State Street among the largest investors. Insider participation is minimal, which is typical for a firm of this size and nature. High institutional participation also increases the emphasis on capital discipline, returns and long-term strategy.

Analyst expectations

Analysts view Deere as a firm that is at the bottom of the cycle, not in structural decline. The consensus consensus is that 2026 will be a transition year, with limited growth and pressure on profitability, but with the potential for improvement in the years ahead as farm income and farmer investment stabilize.

Commodity prices, global trade policy, tariff developments and the company's ability to further develop its high-margin technology and service segments remain key drivers going forward. It is these that may determine how quickly and how strongly Deere can rebound from the next cycle.