Global banks today operate far beyond traditional lending. They function as financial infrastructure, earning across payments, markets, asset management, and risk transfer—especially when the economic cycle becomes less forgiving. JPMorgan Chase continues to set the benchmark, combining balance-sheet strength with a willingness to deploy capital when others hesitate.

The fourth quarter of 2025 illustrates that advantage clearly. Record-level earnings are only part of the story. More important is how the bank reallocates capital toward fee-based growth while maintaining credit discipline. The expanded role of Apple Card reflects this logic: a long-term consumer platform bet embedded within a broader, highly diversified earnings engine.

What was the last quarter like?

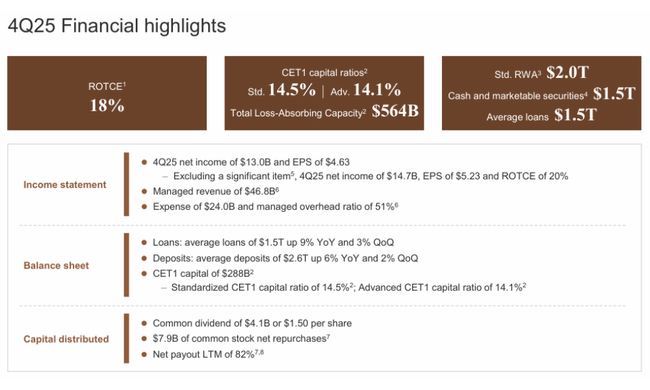

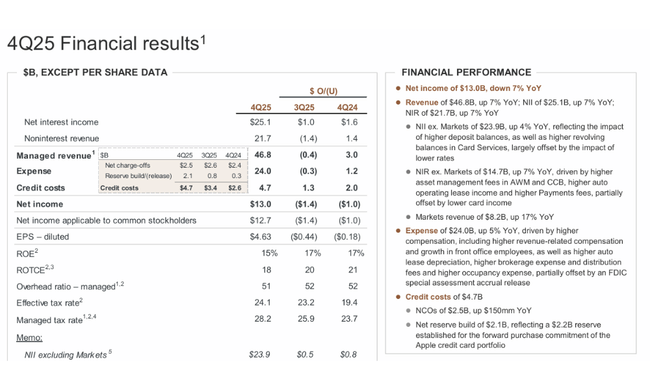

JPMorgan $JPM reported net income of $13.0 billion and EPS of $4.63 for Q4 2025, with the bank reporting earnings of $14.7 billion and EPS of $5.23 after adjusting for a significant item (more on that below). On a revenue level, it's a very robust quarter: reported revenue of $45.8 billion and $46.8 billion on a "managed" basis, up about 7% year-over-year. In the context of a large bank, that's a pace you don't usually do with one trick - several things have to come together: market activity, fees, payment volumes, a stable deposit base, and the ability to monetize the client base across segments.

The revenue structure shows exactly why JPMorgan excels. Net interest income (NII) of $25.1 billion was up year-over-year, but at the same time, management explicitly acknowledges that some of the growth was driven by the lower rate environment and pressure on deposit margins. The non-interest component is all the more important: non-interest income of USD 21.7 billion grew at a similar rate to the whole, signalling that the bank is not just dependent on the interest rate curve. The most visible driver was traditionally CIB, where Markets delivered 17% growth and Equity Markets in particular +40%, exactly the type of result that comes from a combination of volatility, client activity and a good position in funding and prime services in banks.

But at the same time, the quarter showed the other side of the story: the price of growth and the price of risk. Costs (noninterest expense) of $24.0 billion were up year-over-year, not only because of "wage inflation" but also because JPMorgan has been hiring in the front office and investing in capacity to keep pace in banking, markets and wealth management for a long time. Crucially, the bank is maintaining very decent efficiency despite rising costs: an overhead ratio of around 51-52%. This is still an excellent level for a universal bank in such a broad business.

Naturally, however, credit losses and provisions attract the most attention. Credit costs USD 4.7 billion, of which net charge-offs USD 2.5 billion and net reserve build USD 2.1 billion. Need to read the numbers right here: the bulk of the "build" is not classic portfolio deterioration, but a one-time Apple Card-related provision. Even so, the signal from the credit cycle is clear - normalisation is gradually taking hold in consumer credit after strong years, although JPMorgan still comes across as an institution that has risk under control and is working ahead.

CEO commentary

Jamie Dimon built the quarterly story on a simple thesis: the bank finished the year strongly, he said, because "every line of business worked" and the performance was the result of long-term investment, good execution and the ability to take advantage of the market environment. What's important in the communication is that Dimon presents the results not as a "once-in-a-lifetime quarter" but as evidence that the universal bank model makes sense precisely when the economy and markets are behaving illegibly - margins are squeezed somewhere, activity is rising somewhere, credit is deteriorating somewhere, fees are flowing somewhere.

But at the same time, Dimon typically adds a caveat: markets, he says, may be underestimating risks such as geopolitics, "sticky" inflation and high asset valuations. This is consistent at JPMorgan: the bank wants to maintain its reputation as an institution that can be aggressive in growth but conservative in framing risks. And that's exactly where the Apple Card fits in: the deal is presented as a thoughtful deployment of excess capital into an attractive opportunity, but at the same time a significant cushion is built in at the very first step so that the credit profile doesn't change "blindly."

Outlook

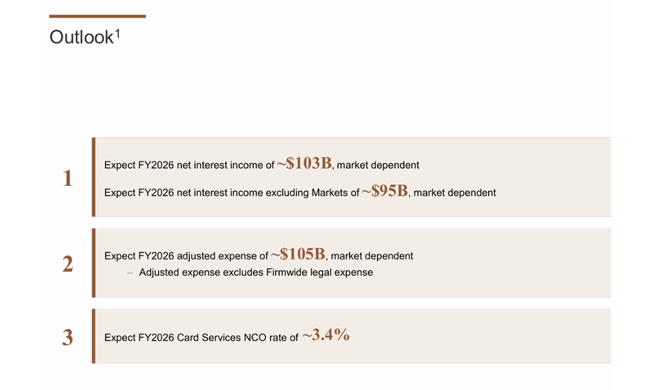

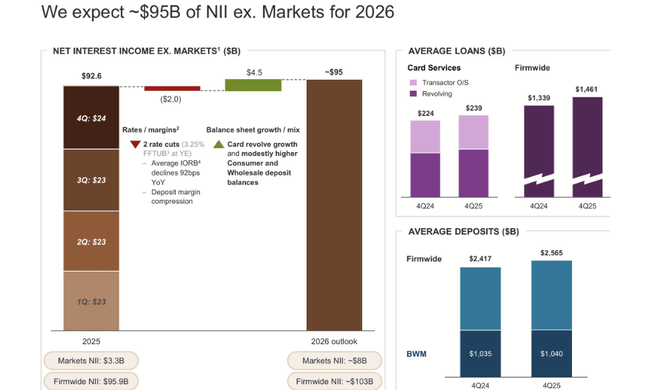

At the operational outlook level, the key is that the bank continues to grow its balance sheet: average loans +9% YoY, deposits +6% YoY. This is a double-edged sword for 2026: on the one hand, it feeds NII and fee income (as client "monetisation" increases with volumes), on the other hand, it increases sensitivity to delinquency on some consumer portfolios later in the cycle. In Q4, you can already see this in credit costs and it's fair to expect 2026 to be more about risk management than a "free sprint".

The Apple Card will be a theme in itself in the coming quarters. It's already clear that the bank has made a $2.2 billion provision for forward purchase commitments, which has reduced EPS by about $0.60. Important: What JPMorgan is really saying is that it doesn't want to make the portfolio acquisition look like a pure growth story with no costs. So the market will be looking mainly at three things in 2026: how quickly the portfolio integrates, how the charge-off trend in the cards plays out, and whether the economics of the product can be brought to a level that makes sense after accounting for the cost of the client acquisition.

Long-term results

Over the long term, JPMorgan remains an extremely profitable machine that can grow even in an environment where banks' earnings mix typically deteriorates. According to the long-term numbers, the firm has increased "total revenue" from roughly $127.2 billion (2021) to $270.8 billion (2024), while also growing operating profit and net income. Crucially, the growth was not "paper": EPS moved from 15.39 (2021) to 19.79 (2024), according to the same series, signalling that working with capital and the share count were also reflected in the result.

More important is the stability of the profitable core. While the years vary depending on whether trading or interest margin earns more, JPMorgan has long held the ability to generate high profits in various market regimes. This is why the title often acts more like a "quality compounder" than a classic cyclical bank. In 2026, therefore, the key question will not be whether there will be one weaker quarter, but whether the structural parameters will change: capital regulation, long-term interest levels, and consumer credit losses.

Moreover, from a per-share perspective, it is important that the bank combines organic growth with return on capital. If the firm continues to maintain discipline in costs and credit reserves while continuing to buyback, it can maintain solid EPS growth even in a weaker revenue growth environment.

News

The biggest specific news story of the quarter is clearly Apple Card. Not just because it is a media prominent product, but because it changes the structure of the card portfolio and adds a new source of growth in consumer finance. But at the same time, it's a deal where JPMorgan clearly doesn't want to risk a reputational or balance sheet surprise - which is why the big provision for forward purchase commitment came right away in Q4. In practice, this means that Apple Card will be a "live" story for investors in 2026, with measurable metrics: charge-offs, delinquencies, portfolio returns, and acquisition/servicing costs.

Alongside this, the robust activity in CIB, particularly in Markets, and record numbers in Payments (Dimon mentions record revenue in this area) are also worth noting. This is typical of JPMorgan's "quiet" strength: even when it's not exactly pulling investment banking fees, it can make up for it with market activity, prime services and a payments infrastructure that grows with client volumes.

Shareholder structure

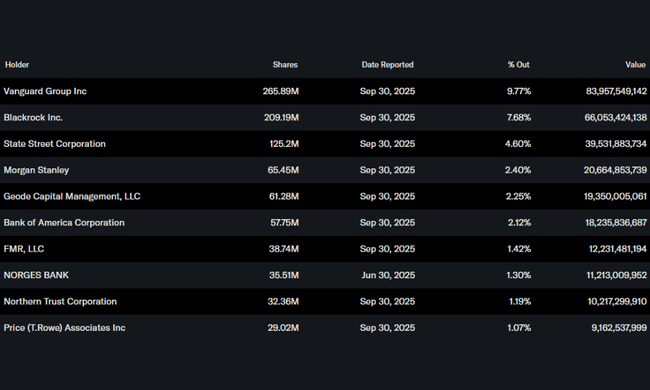

The ownership structure matches the profile of a "core" financial title: the institution holds roughly 74% of the stock, and insider holdings are low (around 0.37%). The largest institutional holders have traditionally included Vanguard (c. 9.77%), BlackRock (c. 7.68%) and State Street (c. 4.60%), which is standard for large banks - a high proportion of passive and quantitative holders increases the importance of index flows, but also typically stabilizes the ownership base.

Analysts' expectations

The analyst consensus is in "quality core holding" mode at JPMorgan, but with sensitivity to the credit cycle and to the pace of capital return higher than before after very strong years. Analysts typically value diversification of returns (CIB, AWM, Payments), the ability to hold efficiency even when investing for growth, and traditionally conservative risk management. However, they also warn that the combination of a benign market environment and high interest yields may be harder to replicate in 2026, and that investors will punish any sign of deterioration in consumer credit, particularly for cards, much more severely.

According to a consensus summary on MarketBeat, the title has a mostly positive rating and is tracked through a combination of price targets and expected EPS for the period ahead. MarketBeat lists a consensus target price of approximately $334.57, while also noting that one of the recent moves in coverage has been a target price move at Goldman Sachs to $386, for example.