As 2025 drew to a close, the banking sector faced mounting uncertainty. Interest-rate trajectories, consumer resilience, and credit quality all remained under scrutiny, making it increasingly difficult to separate structural strength from cyclical delay. Many institutions were still operating in risk-management mode rather than positioning for growth.

Bank of America’s fourth-quarter results tell a different story. Stable revenue generation, resilient loan demand, easing credit losses, and improving operating efficiency suggest the bank is entering the next phase of the cycle from a position of strength. The narrative is no longer about protecting capital, but about selectively redeploying it as conditions normalize.

How was the last quarter?

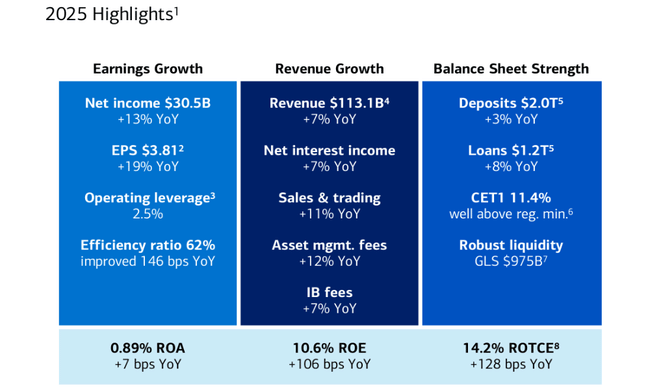

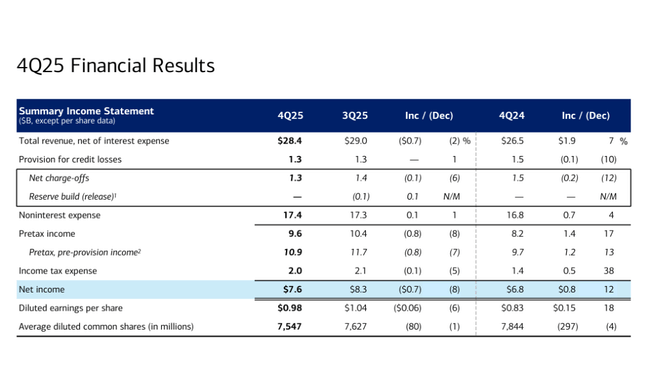

The fourth quarter of 2025 brought Bank of America $BAC s net income to $7.6 billion, up roughly 12% year-over-year and an increase in earnings per share to $0.98. Total revenue, adjusted for interest expense, was $28.4 billion, up 7% from the same period last year. The key driver was the growth in net interest income, which rose 10% to $15.8 billion, despite the gradual decline in rates.

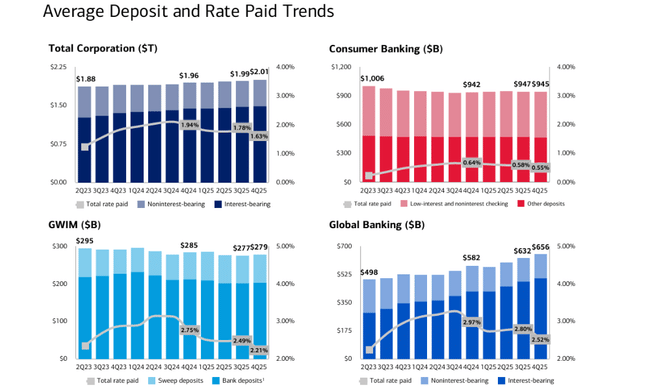

The evolution of lending activity was also a positive sign. Average loans and leases rose 8% year-on-year to $1.17 trillion, with growth evident in all major segments - from consumer loans to small business to corporate clients. Average deposits reached $2.01 trillion and grew for the tenth consecutive quarter, confirming the Bank's strong funding position.

On the risk side, there was a slight improvement. Loan loss provisioning fell to $1.3 billion and net charge-offs declined to the same level, indicating a stabilization of the credit cycle. At the same time, operating efficiency improved, with the cost-to-income ratio falling to 61%, an improvement of almost two percentage points year-on-year.

Segment performance

Consumer Banking remained the largest pillar of the Group. This segment generated net income of $3.3 billion on revenue of $11.2 billion, up 5% year-on-year. The Bank continued to strengthen its dominant position in the US deposit and retail banking market. Combined card payments reached $255 billion, up 6% year-on-year, and digital channels accounted for nearly 70% of all sales.

The Wealth and Investment Management division benefited from favorable capital markets. Segment net income reached $1.4 billion and revenue grew 10% to $6.6 billion. Client assets under management reached $4.8 trillion, up 12% year-on-year, and positive net capital inflows confirm the return of investor confidence.

Corporate and investment banking posted a solid performance. Net income of $2.1 billion was mainly supported by growth in transaction services and treasury products. Investment banking maintained its third place in the global fee rankings, while corporate deposits grew by 13%.

Markets trading contributed a net gain of $1 billion. Trading revenues grew 10%, with equity trading posting strong growth of 23%. Fixed income remained stable, reflecting lower volatility in bond markets.

CEO comment

In his comments, CEO Brian Moynihan highlighted that the bank closed 2025 with over $30 billion in net income and 19% year-over-year earnings per share growth. His words show that management views the results not only as evidence of resilience, but also as confirmation of the right strategic direction. Moynihan repeatedly highlighted the combination of revenue growth, positive operating leverage and improving efficiencies that have led to improved returns on capital.

His view of the macroeconomic environment is also interesting. The CEO acknowledged lingering risks, but also said that consumers and businesses remain relatively healthy and that the bank enters 2026 with optimism about continued U.S. economic growth. This tone is important because it suggests that Bank of America does not feel defensive, but rather ready to take advantage of any improvement in economic activity.

Outlook

Bank of America's outlook for the period ahead rests on several key pillars. The first is the evolution of net interest income, which, even in an environment of gradually declining rates, should benefit from higher loan volumes and a stable deposit base. Management has repeatedly stressed that volume growth and balance sheet structure will play a bigger role in 2026 than the level of rates themselves.

The second pillar is cost control and efficiency gains. The improvement in the efficiency ratio to 61% in the fourth quarter shows that the bank can absorb some of the inflationary pressures while investing in technology and people. The third pillar is returning capital to shareholders. In the fourth quarter, the bank returned $8.4 billion to shareholders through dividends and share repurchases, underscoring management's confidence in the bank's capital strength.

Long-term results and trend

Looking at Bank of America through the lens of the past four years, we see a classic story of a bank undergoing a rapidly changing environment - from a post-covetous recovery to an inflation shock to a period when the market began to address what rate normalization would do to net interest income and credit quality. At the revenue level, the firm has strengthened significantly between 2021 and 2024: total revenue has grown from about $93.9 billion in 2021 to $192.4 billion in 2024. That in itself looks like a huge jump, but it needs to be read correctly - much of this growth has been driven by the interest rate component and "higher rates" as a macro tailwind. By 2023, the bank had already reported $171.9 billion, and then 2024 added another growth of just under 12%.

However, profitability was not linear over that period and that is what matters to investors. Operating profit fell between 2021 and 2022 (from roughly $34.0 billion to $31.0 billion), reflecting a combination of higher costs, changes in revenues, and a run-up in reserves in some part of the portfolio. In 2023, there was a further decline in operating profit to USD 28.3 billion, and only 2024 brought a slight improvement to USD 29.3 billion. In other words, revenue grew strongly but operating profit stabilised more sideways - a typical signature of an environment where banks are earning interest income but paying a "tax" in the form of investment, wage inflation, higher compliance costs and more careful credit risk management.

From a net profit perspective, the picture is similarly important. The bank has managed to keep net profit in a relatively narrow range: $32.0 billion in 2021, $27.5 billion in 2022, $26.5 billion in 2023 and $27.1 billion in 2024. That said, despite significantly higher revenues, net profit has not yet returned to 2021 levels. At first glance, this may look like a weakness, but the key to the long-term reading is that the bank was also intensively reducing the number of shares outstanding at the time, which supported earnings per share. The average number of shares fell from roughly 8.49 billion in 2021 to 7.74 billion in 2024. As a result, EPS in 2024 reached $3.25, slightly above 2023 ($3.10) and 2022 ($3.21). The bottom line is that even as absolute net income stagnates, some value materializes for shareholders through buybacks and higher EPS.

Another thing that stands out from the long-term data is the cost structure. Operating costs have been significantly "sticky" in recent years - $59.7bn in 2021, $61.4bn in 2022, $65.8bn in 2023 and $66.8bn in 2024. In practice, this means the bank is carrying a higher cost base into the next period and needs either further revenue growth or an acceleration in efficiency to start stretching margins again. That's why the shift in efficiency (efficiency ratio of 61% and year-on-year improvement) is so important in the current Q4 2025 - it's a signal that management is no longer just "holding on" but is gradually squeezing more productivity out of the cost base.

Shareholding structure

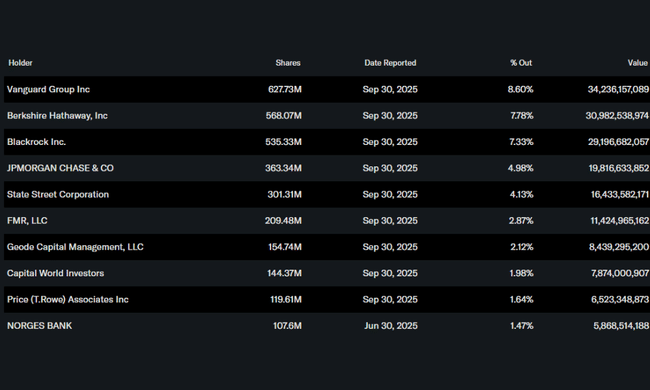

Bank of America's shareholder base is stable and strongly institutional. Approximately 70% of shares are held by institutional investors, with Vanguard, Berkshire Hathaway and BlackRock among the largest. Berkshire Hathaway's significant stake underscores the long-term confidence of conservative investors in the bank's business model. Insider ownership remains relatively low, which is standard for banks of this size.

Analyst expectations

Analysts enter 2026 with a mostly neutral to slightly positive outlook. The consensus expects modest earnings growth driven by a combination of higher loan volumes, stable asset quality and continued share buybacks. The bank's sensitivity to rate movements remains a key theme, but there is also a growing focus on fee income from wealth management, transactions and digital services.

A number of analyst houses have warned that if the US economy avoids a major recession in 2026, Bank of America could gradually improve its return on capital and return to pre-2022 levels. At the same time, however, the risk remains a potential deterioration in consumer credit or a faster decline in rates that could pressure net interest income.