By the end of 2025, BlackRock occupies a position few asset managers can realistically challenge. The firm sits at the intersection of several long-term forces reshaping global finance: the continued financialisation of savings, the expansion of ETFs, the growing role of alternatives, and rising demand for data, analytics, and outsourced investment infrastructure.

Scale is a decisive advantage in this environment. While fee pressure remains a structural headwind across asset management, BlackRock’s breadth, distribution power, and technology stack allow it to grow both assets and absolute earnings. Fourth-quarter results reinforce the view that the company is not entering 2026 as a mature giant, but as a platform still expanding its economic reach.

How was the last quarter?

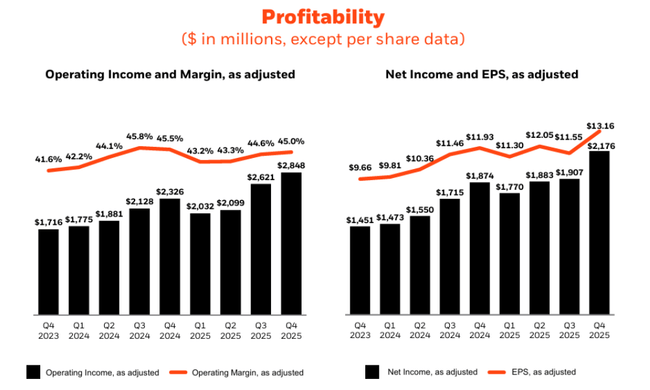

BlackRock's fourth-quarter EPS of $13.16 beat forecasts by 5.79%.

Revenue rose to $7 billion, up 23% year-over-year.

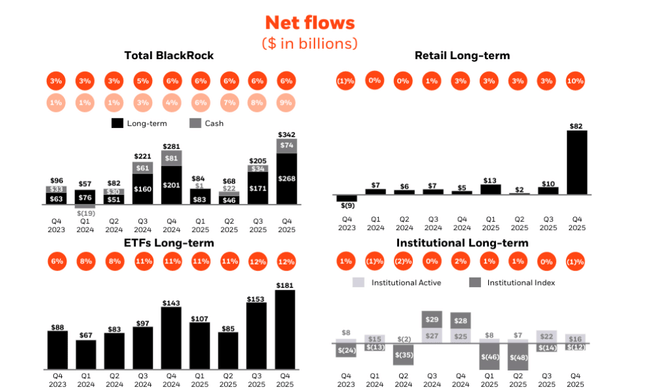

Record $527 billion in net inflows into the iShares ETF.

Dividend rose 10%, with $1.8 billion in share repurchases planned for 2026.

The fourth quarter of 2025 was strong for BlackRock $BLK, primarily in terms of capital inflows and organic fee growth. Assets under management grew to approximately $14 trillion, driven by net inflows of approximately $342 billion during the quarter alone. This confirms the firm's ability to attract capital across market cycles and regions.

At the operating level, the quarter was characterized by very strong growth in core fees, which grew 12% year-over-year in annualized terms. iShares ETFs, systematic active strategies, private markets and outsourcing services were the main drivers. The results also show that growth is not dependent on any one segment but is broadly spread across products and client groups.

On a GAAP basis, earnings were dampened by higher non-cash costs associated with acquisitions and a one-time charitable contribution, resulting in a year-over-year decline in reported EPS. However, after adjustments, operating performance remained very strong, with adjusted earnings per share of $13.16, confirming the company's robust internal earnings power.

CEO commentary

Larry Fink was clear in his comments that 2025 was the strongest year ever in terms of net capital inflows. He emphasized that BlackRock enters 2026 as a unified platform following the integration of GIP, HPS and Preqin, which significantly expands the firm's capabilities in private markets, data and alternative strategies.

Management also openly talks about long-term growth pillars - private markets, wealth management, active ETFs, digital assets and tokenization. The 10% dividend increase and the expansion of the buyback program are then a clear signal of confidence in medium-term growth in margins and profitability.

Long-term results

BlackRock's long-term development confirms that the firm is gradually moving from a traditional asset manager to a global investment and technology platform. Between 2022 and 2023, revenues remained more or less flat, reflecting weaker capital markets and lower asset valuations. From 2024, however, the company re-entered a phase of accelerated growth.

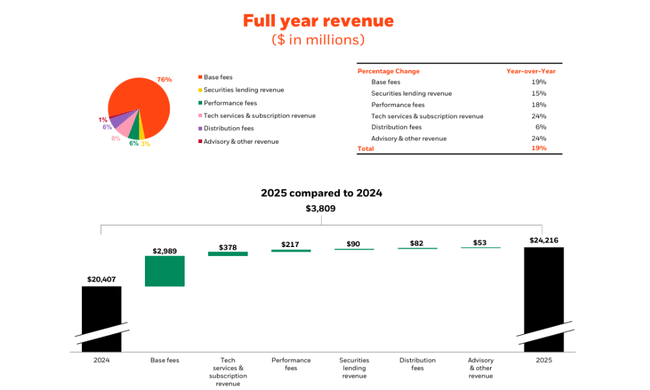

In 2025, total revenues grew nearly 19% to more than $24 billion, with gross profit growing even faster than revenues. This points to improving operating leverage and higher contribution from higher-than-average margin products, particularly in alternatives, technology and data services.

Net income on a GAAP basis was lower in 2025 than in 2024 due to one-time costs, but adjusted results clearly show increasing profitability. Both EBITDA and EBIT have been growing over the long term, confirming that BlackRock can monetize growth in assets under management even in an environment of fee pressures. From a long-term perspective, this is a high-quality, capital-efficient business with very stable cash flows.

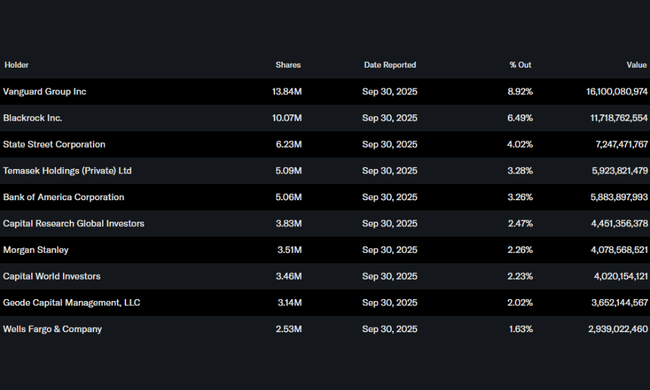

Shareholding structure

BlackRock's shareholder structure is typical of a high-quality institutional title. Over 80% of the shares are held by institutional investors, with Vanguard, State Street and other large asset managers being the dominant shareholders. The high level of institutional ownership contributes to the stock's low volatility and long-term stable investment profile.

Outlook

BlackRock enters 2026 with exceptionally strong momentum. Management expects continued double-digit organic base fee growth, further growth in assets under management and a gradual increase in margins due to higher private markets and technology services. The ambition to raise up to $400 billion in private markets by 2030 suggests that the firm's growth story is still at an earlier stage than its size would suggest.

Analyst expectations

Analyst consensus views BlackRock as one of the best-performing titles in the financial services sector. Expectations for 2026 work with continued earnings per share growth, supported by a combination of higher market valuations, strong net capital inflows and continued share buybacks. Analysts also highlight that BlackRock is one of the few players that can grow over the long term even in an environment of fee pressures, thanks to scale, technology and product diversification.