As 2025 came to a close, 3M was no longer judged on whether improvement was possible, but on how sustainable that improvement could be. Years of legal overhangs, portfolio reshaping, and margin pressure had reshaped investor expectations, shifting the focus from headline recovery to operational credibility.

The fourth quarter delivered an important signal. Earnings growth and margin expansion suggest that restructuring efforts are beginning to translate into day-to-day execution. Just as importantly, the numbers offer early evidence that the company’s reset under new leadership may be creating a path toward consistent value creation beyond a single cycle.

How was the last quarter?

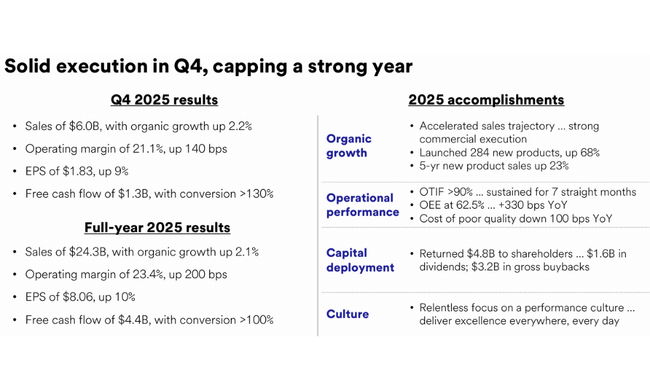

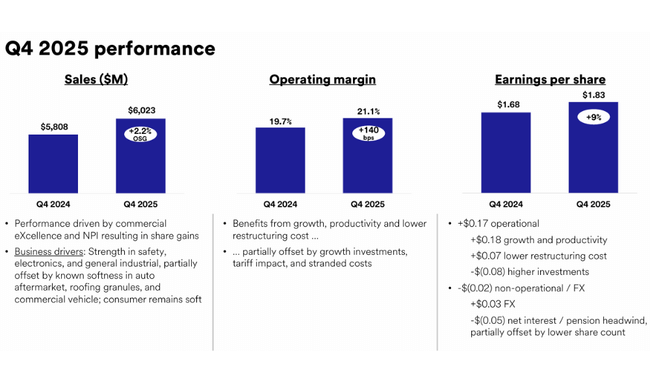

In the fourth quarter of 2025, 3M $MMM reported solid operating performance, which at first blush hides a significant difference between GAAP and adjusted numbers, but it is the adjusted metric that better illustrates the true state of the business. GAAP revenue was $6.1 billion, which represented 2.1% year-over-year growth, while adjusted revenue was $6.0 billion and, when adjusted for PFAS products, delivered 2.2% organic growth. This is particularly important in the context of an increasingly weak industrial macro where 3M managed to grow faster than the market.

The fundamental shift was in margin structure. While GAAP operating margin fell to 13.0% due to exceptional items, adjusted operating margin rose to 21.1%, a 140 basis point improvement year-over-year. This shift confirms the return of operating leverage - a combination of disciplined cost control, price execution and improved product mix.

Earnings per share showed the same story. GAAP EPS was $1.07, down 20% year-over-year, but adjusted EPS was $1.83, up 9% year-over-year. This clearly shows that the core business is generating growing profits while the pressure is coming primarily from one-time and transformation costs.

Cash flow was also a strength in the quarter. Operating cash flow was $1.6 billion and adjusted free cash flow was $1.3 billion, allowing 3M to return approximately $0.9 billion to shareholders through dividends and buybacks. It is the combination of growing profitability and solid cash flow that confirms that the transformation is not just an accounting exercise, but is having a real impact on the company's financial stability.

CEO commentary

Bill Brown identified 2025 as a key "foundation-building" year, laying the foundations for long-term sustainable growth. In his comments, he repeatedly emphasized that 3M was able to grow above macro levels, significantly improve margins, and achieve solid cash conversion, the very metrics that have been the company's weakness in recent years.

Strategically, Brown is moving 3M toward areas with higher structural momentum, such as data centers, electrification and energy infrastructure, including nuclear power. At the same time, he is emphasizing accelerating innovation, commercial execution and operational discipline, which is already starting to translate into improved margins. His rhetoric towards 2026 is confident but underpinned by concrete operational improvements, not just cyclical recovery.

Outlook for 2026

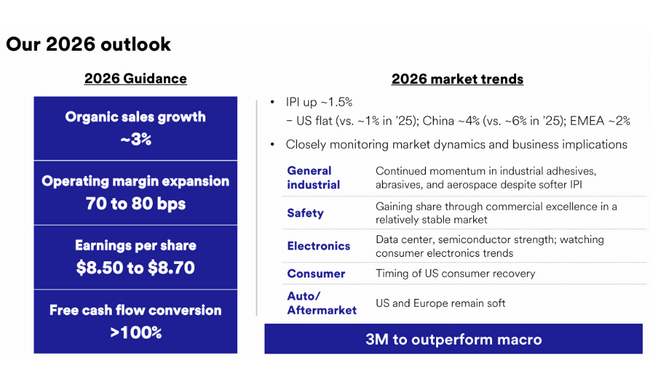

The outlook for 2026 is one of the strongest points in the entire report. Management expects adjusted revenue growth of around 4%, with organic growth of around 3%. This implies a continued ability to grow faster than the wider industry environment.

Further margin expansion is a key element. Adjusted operating margin should increase by 70 to 80 basis points, confirming the continued return of operating leverage. Adjusted earnings per share are projected in the range of $8.50 to $8.70, representing further year-over-year growth from an already strong 2025 base.

From a cash perspective, 3M expects adjusted operating cash flow to be between $5.6 billion and $5.8 billion and more than 100% conversion to free cash flow. This creates room for both continued return of capital to shareholders and investment in growth areas without increasing financial risk.

Long-term results and structural developments

A long-term view of 3M's results shows that 2022 to 2024 was a period of significant volatility and cleansing. Revenues declined from levels of over $35 billion in 2021 to approximately $24.6 billion in 2024, with 2023 heavily impacted by restructuring, legal reserves and extraordinary write-downs. The result was even a deep loss and negative EPS.

However, 2024 and especially 2025 represent a clear turning point. Operating profit increased by more than 20% in 2024 and net income returned to more than $4 billion. EPS jumped to $7.58, marking more than 160% year-over-year growth, and EBITDA was back above $7 billion. This turnaround wasn't driven by a one-off cycle, but by a combination of a lower cost base, a stabilized portfolio, and better pricing discipline.

Over the long term, the key is that 3M has significantly reduced operating cost volatility, stabilized margins, and restored its ability to generate consistent EBIT and EBITDA. This sets the stage for the company to return to gradual earnings growth in the years ahead without being dependent on aggressive financial engineering.

Shareholding structure

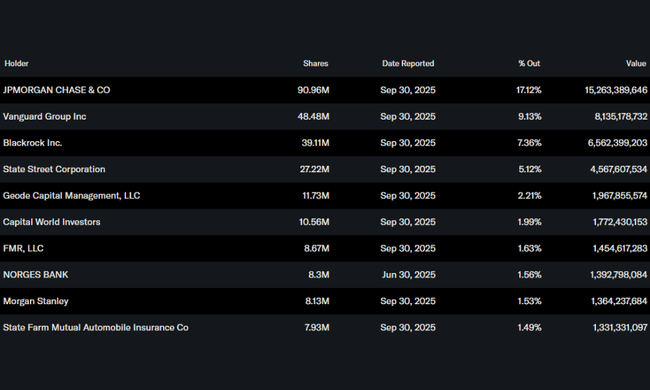

The shareholder structure remains highly institutional, with approximately 74% of the shares held by institutions. JPMorgan Chase is the largest shareholder with over 17%, followed by Vanguard, BlackRock and State Street. The low insider stake of around 0.1% underscores the fact that capital discipline and return on capital at 3M are primarily driven by institutional investor expectations.

Analyst expectations

Analyst consensus has shifted towards cautious optimism following the Q4 2025 results. The key arguments in favor of the stock are the return of margin expansion, stable cash flow, and a clearly communicated 2026 outlook. Analysts continue to monitor legal risks and growth rates in the industrial segments, but improving operating metrics and the ability to meet guidance reduce the discount that has been applied to the stock in recent years.