NextEra Energy ended 2025 in a position many utilities would envy. A regulated Florida business paired with one of the largest renewable energy pipelines in North America continues to offer a rare mix of stability and growth. That very combination, however, has pushed expectations structurally higher.

The fourth-quarter results confirm operational strength and a long runway of projects, yet they also underline the core challenge for the stock. At today’s valuation, investors are less focused on quarterly beats and more on flawless execution—balancing capital intensity, project timing, and shareholder returns over the coming years.

How was the last quarter?

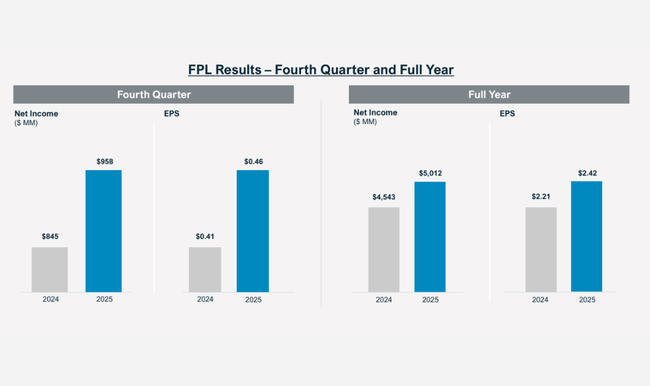

In the fourth quarter of 2025, NextEra Energy $NEE reported GAAP net income of $1.535 billion, equivalent to earnings of $0.73 per share. Compared to the same period in 2024, this is a significant improvement from $1.203 billion and $0.58 per share. On an adjusted basis, earnings were $1.133 billion and $0.54 per share, respectively, representing modest but steady year-over-year growth.

For the full year 2025, the company reported GAAP earnings of $6.835 billion, or $3.30 per share, while on an adjusted basis, earnings were $7.683 billion and $3.71 per share. Thus, adjusted EPS grew approximately 8.2% year-over-year, which is above the high end of the previously announced range. This confirms that the growth story is not driven by accounting effects, but by actual operating performance.

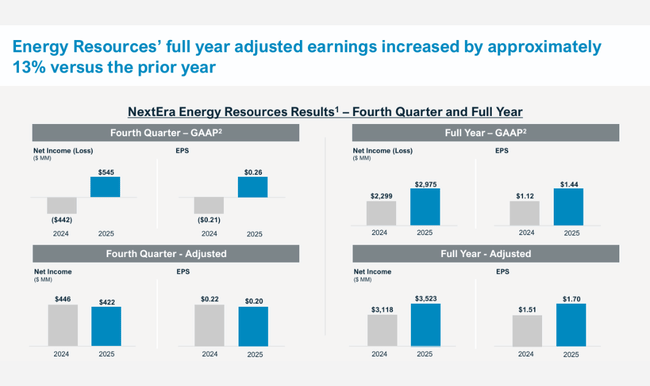

Structurally, the distribution of performance between the main segments is important. Florida Power & Light increased net income to $958 million in the fourth quarter and for the full year reached $5.012 billion, an increase of approximately 10% year-over-year. Growth was driven primarily by expansion of the regulatory base, which increased 8.1% year-over-year, and continued investment in infrastructure. NextEra Energy Resources, on the other hand, showed significant improvement on a GAAP basis, with quarterly results swinging from a deep loss to a $545 million profit, while on an adjusted basis, results remained slightly weaker year-over-year. However, this does not change the fact that the segment continues to generate record new project volume.

CEO commentary

CEO John Ketchum particularly emphasized the company's long-term visibility of growth and unique position in the energy transition. In his words, NextEra Energy has not only surpassed the high end of its own outlook in 2025, but has also set the stage for another decade of expansion. Crucially, growth is spread between FPL's regulated business and long-term contracted projects within Energy Resources, reducing volatility in results.

At the same time, Ketchum has been outspoken about the role of growing demand for electricity - particularly from data centers and hyperscalers - and the company's ability to meet that demand quickly and at a scale that competitors often don't have. In this context, he also mentioned the plan to bring the Duane Arnold nuclear power plant back on line through a long-term $GOOG contract, underscoring the company's strategic flexibility.

Outlook

The outlook remains one of the strongest pillars of NextEra Energy's investment story. Management expects adjusted earnings per share to reach $3.92 to $4.02 in 2026. At the same time, the company reaffirms its goal of growing adjusted EPS at a rate of at least 8% per year through 2032 and at the same rate thereafter from a 2032-2035 base year.

Dividend policy remains consistent with the growth profile - the company is targeting roughly 10% annual dividend growth through 2026 and then a rate of approximately 6% through 2028. Importantly for investors, this growth is backed by long-term contracts, a record backlog of projects and a stable regulatory base in Florida.

Long-term results

Looking at NextEra Energy' s performance over the past four years, it is evident that the company went through a growth phase from 2022-2023, but this was followed by a significant cooling in 2024 across virtually the entire income statement. After strong growth in 2023, when revenues jumped 34% year-on-year to $28.1 billion, they fell 11.9% to $24.8 billion in 2024. This decline is not cosmetic - it is a return to below 2022 levels and a clear signal that the pace of expansion has broken in the short term.

Gross profit has followed this trend even more closely. After a particularly strong year in 2023, when it grew 77% to $18 billion, there was a sharp 17% drop to $14.9 billion in 2024. This suggests that the slowdown was not just about volumes, but also about a worse mix, timing of projects and returns on some investments. Still, it is important to add that absolute gross profit levels remain well above 2021-2022, confirming the firm's structural shift.

At an operational level, the break is even more clear. Operating profit exploded by 151% to $10.2 billion in 2023, but was followed by a 27% decline to $7.5 billion in 2024. Although operating expenses fell 4.5% to $7.4 billion in 2024, it was not enough to offset weaker revenues. This shows that operating leverage has turned against the company in the short term, and investors are rightly watching to see when the effect will turn positive again.

Net income confirms the same story. After a jump in 2023, when it rose 76% year-on-year to $7.31 billion, came a decline of less than 5% to $6.95 billion in 2024.

Earnings per share only confirms this trend. EPS jumped more than 70% to $3.61 in 2023, while it fell about 6% to $3.38 in 2024. Moreover, the decline in EPS was compounded by modest growth in the number of shares outstanding, with the average number of shares rising to about 2.06 billion. That said, some of the pressure per share was not just operational, but also capital.

Shareholding structure

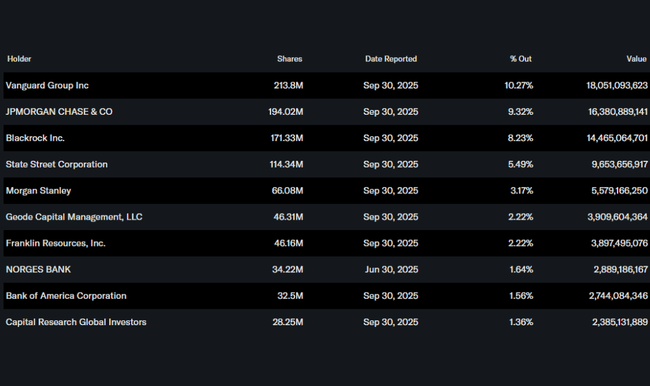

The shareholder structure is typical of a high-quality utility. Institutional investors hold over 83% of the stock and the largest owners include Vanguard, JPMorgan, BlackRock and State Street. The presence of long-term institutional investors supports the stability of the stock, but also increases sensitivity to changes in the outlook and interest rate expectations.

Analyst expectations

Analysts view NextEra Energy as one of the clear winners in the long-term trend of electrification and decarbonization. The consensus expects continued earnings growth in line with management's targets, with the pace of backlog execution and the ability to sustain returns on capital at high levels of investment remaining key themes. The prevailing recommendation is between 'hold' and 'buy', with an emphasis on the long-term horizon and dividend growth rather than short-term price upside.