For years, Tesla was valued as a hyper-growth manufacturer, where delivery momentum and earnings expansion moved in lockstep. That framework is quietly breaking down. As global EV markets mature and pricing pressure becomes structural rather than temporary, profitability is no longer driven by volume acceleration, but by how efficiently capital, software, and energy assets are deployed across the ecosystem. In this phase, headline earnings volatility matters less than the direction of operating leverage.

That shift is becoming visible beneath the surface. While the automotive segment is adjusting to a more normalized margin environment, other pillars of the business are absorbing a growing share of strategic attention. Energy storage is scaling at a pace that reshapes cash generation, while autonomy, AI, and robotics increasingly define long-term optionality rather than near-term earnings. The tension for investors is clear: the short-term profit profile looks constrained, but the business model itself is becoming broader, more resilient, and harder to value through traditional automotive lenses.

How was the last quarter?

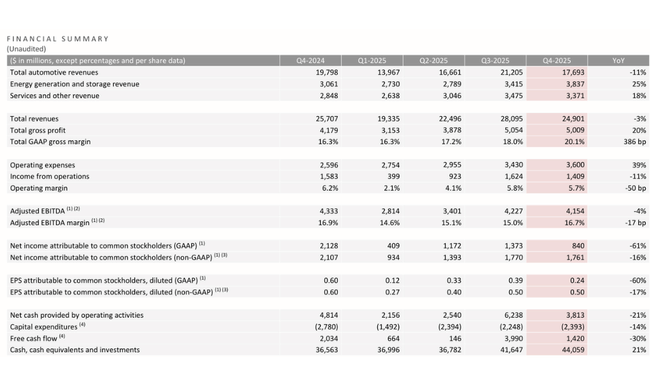

Q4 2025 at Tesla delivered a combination of weaker volumes and sales, but significantly improved gross margins, exactly the type of quarter that looks "worse" on the surface, but in the details shows that the company can drive efficiencies even in a price-tight environment. Total revenue in Q4 was $24.9 billion, -3% YoY vs Q4 2024 ($25.7 billion) and also -11% QoQ vs Q3 2025 ($28.1 billion). The biggest drag was the automotive sector: automotive sales of USD 17.7bn, -11% YoY and -16.6% QoQ, while the Energy sector, on the other hand, continued to grow, partially cushioning the decline in autos - energy generation & storage of USD 3.84bn, +25% YoY and +12.4% QoQ. Services & Other was USD 3.37bn, +18% YoY but slightly -3% QoQ, so the Energy segment was almost exclusively the driver of the quarter in terms of revenue growth.

At the profitability level, the most important signal is in gross margin. Total gross profit was $5.01bn, +20% YoY but -0.9% QoQ. However, the key takeaway is that Tesla was able to increase GAAP gross margin to 20.1%, +386 bp YoY (from 16.3%) and +210 bp QoQ (from 18.0%). In other words, even though it sold less and earned less than in Q3, there is improvement on unit economics and mix. However, the operating level is not so optimistic anymore, as the cost base growth continued: operating expenses of $3.60bn were +39% YoY and +5% QoQ, which put the brakes on operating leverage. The result was income from operations of USD 1.41bn, -11% YoY and -13% QoQ, while the operating margin of 5.7% was -50bp YoY and slightly -10bp QoQ. At the EBITDA level, the picture is more stable: Adjusted EBITDA of USD 4.15bn is -4% YoY and -1.7% QoQ, but Adjusted EBITDA margin of 16.7% is holding solid at just -17 bp YoY, even +170 bp QoQ vs Q3.

Cash flow is the biggest "twist" of the quarter and the reason why the market often reacts better than net income would suggest. Operating cash flow of $3.813bn was -21% YoY and also -39% QoQ (Q3 was $6.238bn). Yet Tesla remained FCF positive: free cash flow of $1.42bn is -30% YoY and significantly -64% QoQ (Q3 $3.99bn). Capex was USD 2.393bn, -14% YoY but up slightly from Q3 (c. +6% QoQ), so part of the FCF weakness is simply attributable to weaker OCF in the quarter. At the same time, the balance sheet remains extremely strong: cash, cash equivalents & investments of USD 44.1bn, +21% YoY and +5.8% QoQ.

Operationally, Q4 was weaker in autos but record in energy. Total deliveries of 418,227 were -16% YoY and -15.9% QoQ, while production was 434,358, -5% YoY and roughly -2.9% QoQ. Inventories increased: days of supply 15 is +25% YoY and +50% QoQ (up from 10 in Q3), suggesting a less "tight" balance between production and demand at the end of the year. Against this stands energy: storage deployed of 14.2 GWh was +29% YoY and +13.6% QoQ, a record quarter even with a clear acceleration. And software monetization continues: Active FSD subscriptions of 1.1m is +38% YoY and +10% QoQ. Infrastructure continues to grow at a pace that confirms the long-term "moat": supercharger stations +17% YoY and connectors +19% YoY.

Operational metrics and ecosystem scaling

Tesla produced 1.65 million vehicles in 2025 (-7% YoY) and delivered 1.64 million vehicles (-9% YoY). The decline was primarily in other models outside of Model 3/Y, where deliveries fell 40% YoY. In contrast, the APAC region recorded record deliveries, confirming the geographic shift in demand.

The power sector saw record deployment of 46.7 GWh (+49% YoY), a fifth consecutive record quarter at the gross profit level, and a rapidly growing network of Virtual Power Plants, which already includes more than 1 million installed Powerwall units.

The infrastructure continues to expand, with Tesla operating 1,553 sites, 8,182 Supercharger stations and nearly 78,000 plugs, representing YoY growth of around 17-19%.

Outlook and strategic priorities

Tesla clearly declares that 2026 will not primarily be about maximizing automotive margins, but about building the infrastructure for the next wave of growth. The company plans to roll out six new production lines across vehicles, energy, batteries and robotics, including the launch of Cybercab and Tesla Semi production in the first half of 2026.

In autonomy, Tesla continues to iterate rapidly in FSD (Supervised), with active subscribers growing to 1.1 million (+38% YoY). The Robotaxi service launched in Austin in January 2026 with the phasing out of safety oversight, a key step toward monetizing autonomous software. In parallel, the company is investing in its own AI stack - the goal is to more than double AI training capacity in Texas during 1H 2026.

The energy segment is expected to be one of the main growth drivers. Tesla plans to start production of Megapack 3 and Megablock in Houston, while storage demand remains extremely strong due to growth in electricity consumption, data centers and AI infrastructure.

CEO commentary

In his comments, Elon Musk reiterated that short-term financial results are not the main measure of Tesla's value. Management, he said, is purposefully sacrificing a portion of automotive margins in favor of long-term volume growth, data collection, and building infrastructure for autonomous driving and AI. Musk has repeatedly stressed that Tesla's key asset is not the cars themselves, but the software, data and ability to scale the autonomous system globally.

At the same time, however, he struck a more realistic tone than in previous years. Executives acknowledged that the environment of price competition remains challenging and that a return to historic levels of automotive margins will not be quick. The focus was on cost control, more efficient production and a gradual increase in the proportion of revenue from higher value-added areas, particularly Full Self-Driving, energy solutions and future AI applications.

Long-term results

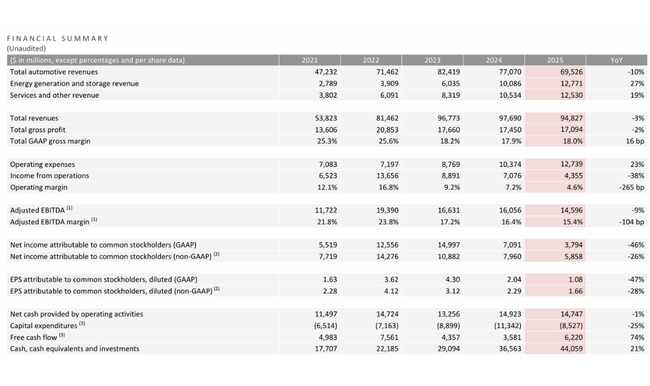

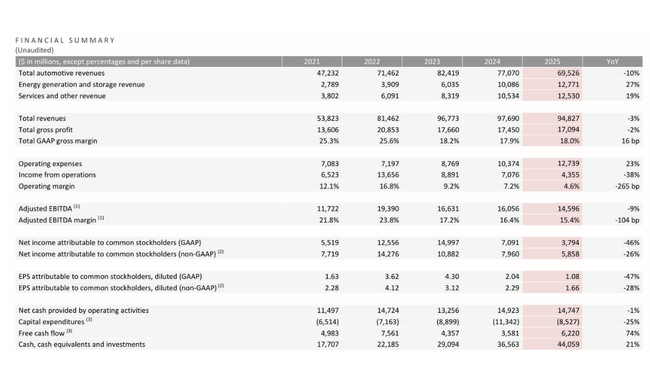

The long-term trend in Tesla's $TSLA results shows a very sharp contrast between the better phase of 2021-2022 and the significantly more challenging period of the last two years, when the company had to deal with demand normalization, the EV price war, and a sharp increase in its cost base. While Tesla will have spent $53.8 billion in 2021 and $81.5 billion in 2022, a year-on-year growth of over 50%, the momentum has gradually run out. The year 2023 still brought solid revenue growth to USD 96.8 billion (+18.8%), but 2024 marked a virtual stagnation, with sales reaching USD 97.7 billion, equivalent to a growth of less than 1%. This development clearly shows that Tesla has hit the limits of rapid volume expansion and that further growth will no longer be automatic, but will have to be 'earned' either by pricing or new segments.

An even more pronounced change is evident at the level of margins. Gross profit peaked in 2022 at USD 20.9 billion, but has been systematically declining since then - to USD 17.7 billion in 2023 and to USD 17.45 billion in 2024. The main problem is not just revenue stagnation, but the cost structure. Cost of revenue has risen from USD 40.2 billion in 2021 to USD 60.6 billion in 2022 and further to USD 80.2 billion in 2024, with the rate of cost growth outpacing the rate of revenue growth in recent years. This is the exact opposite of the operating leverage that has allowed Tesla to grow profitability explosively in the past. As a result, gross margins have moved significantly lower from levels above 25% in 2021-2022, and the company now operates in a much thinner unit margin environment.

At the operating level, the break even more clearly. Net profit reached a record $13.7 billion in 2022, but fell to $8.9 billion in 2023 and to just $7.1 billion in 2024, a drop of more than 48% from the peak. Operating costs play a major role in this. Operating expenses rose from USD 7.1 billion to USD 10.4 billion between 2021 and 2024, an increase of almost 50%, with growth continuing at over 18% in 2024. Thus, Tesla today carries the cost structure of a company that is still investing as a growth title but generating revenue more in the style of a mature cyclical business. This mismatch is the main explanation why operating margins have fallen from 16.8% in 2022 to around 7% in 2024.

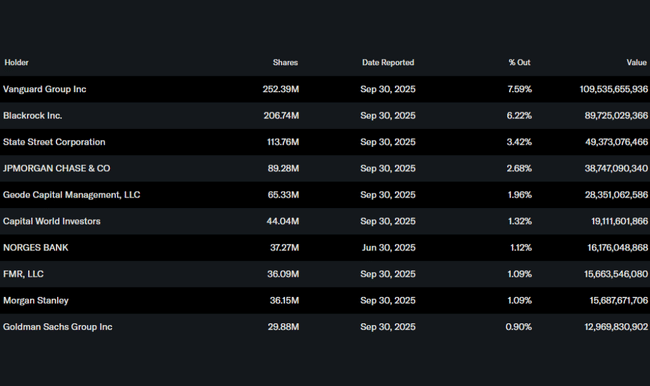

Shareholding structure

Tesla's stock is heavily institutionally owned. Institutions hold approximately 50% of the stock, with Vanguard (7.6%), BlackRock (6.2%), and State Street (3.4%) remaining the largest investors. Insider ownership of around 12.6% continues to ensure management's strong interdependence with the company's long-term performance.

Fair Price

The main reasons why Tesla stock is rising after earnings, even though most metrics are down year-over-year:

Significant margin improvement despite weaker sales - The market is overlooking the decline in sales and earnings and focusing on the fact that Tesla was able to increase its overall gross margin to 20.1% in Q4, up 386bp YoY and over 200bp QoQ. This is a clear signal that the automotive price war is not leading to the destruction of unit economics and that the company has room to re-scale profitability gradually.

Record and accelerating business in Energy & Software - Energy generation & storage achieved record shipments and revenues with 25% YoY and 12% QoQ growth, while the number of active FSD subscribers grew to 1.1m (+38% YoY). It is these segments that have significantly higher long-term margin potential than car sales and reinforce the thesis that Tesla is no longer a pure car company.

Strong Balance Sheet and No Negative Surprises in Outlook - Cash and investments rose to $44.1 billion (+21% YoY) and the company remains FCF positive even in a weaker quarter. The outlook does not contain any shocks in the form of deteriorating liquidity, the need for external funding or a sharp increase in capex, which combined with low market expectations was enough for the stock to react positively.