At first glance, Microsoft's results for the second fiscal quarter of 2026 look very strong. The company delivered double-digit revenue growth, a significant improvement in profitability, and continued acceleration in both cloud and AI. Yet the stock is down after the market close. The reason is not disappointment with the numbers per se, but a clash between very high market expectations and the reality of a quarter that was "only" very good, not surprisingly exceptional.

The market today is not looking to Microsoft for confirmation that AI works - that is already taken as a given. Investors want to see clear signals of further growth acceleration or at least a concrete improvement in the outlook to justify the current valuation. Thus, the quarter confirmed a stable, high-quality growth story rather than taking it to a new level, and it is this lack of "new positive momentum" that explains the stock's cool reaction despite solid results.

How was the last quarter?

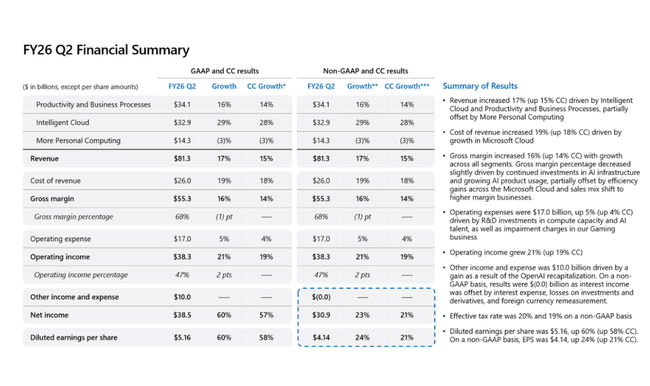

Microsoft $MSFT reported $81.3 billion in revenue in its fiscal second quarter, up 17% year-over-year (15% at constant currency). Not only is the growth rate well above the megacap tech sector average, but it is accelerating in the highest value-added segments. The development was even stronger at the operating profit level - operating income reached USD 38.3 billion, +21% YoY, a clear return of operating leverage.

On the bottom line, the quarter was also exceptionally strong thanks to the impact of the OpenAI investment. GAAP net income rose to USD 38.5bn (+60% YoY) and GAAP EPS reached USD 5.16 (+60% YoY). Adjusted for this impact, non-GAAP net income was USD 30.9 billion (+23% YoY) and non-GAAP EPS was USD 4.14 (+24% YoY), still very robust growth and a clear outperformance of last year.

To make the picture clear, the highlights of the quarter can be summarized as follows:

Revenue: USD 81.3 billion, +17% YoY

Operating income: USD 38.3 billion, +21% YoY

GAAP EPS: $5.16, +60% YoY

Non-GAAP EPS: $4.14, +24% YoY

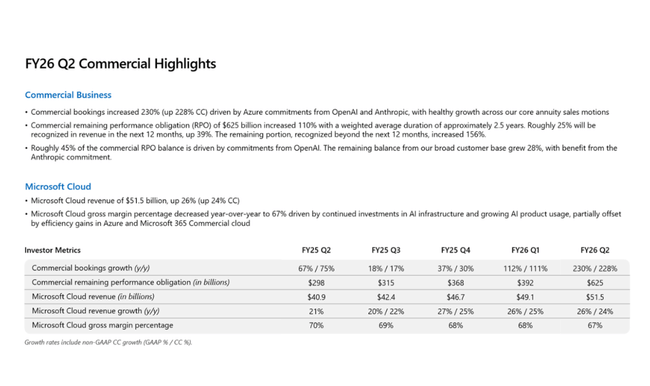

Microsoft Cloud revenue: $51.5 billion, +26% YoY

Commercial RPO: $625 billion, +110% YoY

Segmentally, the quarter was clearly driven by cloud and AI. Intelligent Cloud achieved revenues of USD 32.9bn (+29% YoY), with Azure and other cloud services accelerating to +39% YoY, confirming that demand for AI infrastructure remains extremely strong. Productivity and Business Processes grew to $34.1 billion (+16% YoY), with Microsoft 365, Dynamics and LinkedIn all posting solid double-digit growth. The only weak spot remains More Personal Computing, where revenues were down 3% YoY, mainly due to Xbox, but this does not have a material impact on the overall picture.

CEO commentary

In his comments,Satya Nadella highlighted that Microsoft is still only at the beginning of the AI adoption curve. According to him, Microsoft's AI business is already reaching a size that would be equivalent to one of the company's traditional core segments on its own. He emphasized that Microsoft controls the entire AI stack - from data centers to its own software to the application layer - allowing it to scale faster than competitors.

Nadella's words make clear that the strategy is clearly long-term: the goal is not short-term margin maximization, but building a platform that will become the standard for enterprise AI. It is this tone - a combination of confidence and discipline - that the market has long appreciated.

Outlook

Microsoft traditionally does not provide a detailed numerical outlook in a press release, but several signals are very strong. The most prominent is the commercial remaining performance obligation of $625 billion, which represents 110% year-over-year growth and gives high predictability of future revenues. This is a key figure for investors as it confirms that the current growth is not a one-off.

The firm also suggests that cloud and AI will continue to grow significantly faster than the rest of the portfolio, while more traditional segments remain stable. Investment in data center and AI infrastructure will continue, but management reiterates its emphasis on return on capital and maintaining high operating margins.

Long-term results

Microsoft's long-term evolution confirms that the company has transformed in recent years from a high-quality software conglomerate into a global digital infrastructure company whose growth is now increasingly driven by cloud and AI. Between fiscal years 2022 and 2025, total revenue grew from $198.3 billion to $281.7 billion, corresponding to average annual growth of around the mid-teens percent. Crucially, the growth rate has not only slowed in the last two years, but has instead stabilized in the high double digits, which is exceptional for a company of this size.

In terms of revenue structure, there is a marked shift towards recurring and highly visible revenue. Cloud services, particularly Azure, are gradually increasing their share of total sales while improving the predictability of future results. This is reflected in the sharp growth in the commercial residual performance obligation, which reached USD 625 billion at the end of Q2 FY2026, creating a strong 'backlog' of future revenues and reducing the cyclical volatility of the business.

At the profitability level, Microsoft has maintained exceptionally strong operating leverage over the long term. Gross profit grew from US$135.6bn to US$193.9bn between FY2022 and FY2025, while cost of sales grew faster than in the past, mainly due to massive investments in data centres and AI infrastructure. Despite this, the company has managed to maintain very high gross margins, which is a testament to the strength of its pricing and scalability of its software model.

Operating costs are one of the key issues in the current investor debate. Operating expenses rose to $65.4 billion, an increase of more than $13 billion from FY2022. This growth is deliberate and reflects investments in developing AI models, expanding cloud infrastructure, and strengthening security and enterprise solutions. At the same time, it is clear that the rate of cost growth is now significantly lower than the rate of revenue growth, allowing for further expansion in operating margin.

As a result, operating income has been steady and gradually increasing, reaching $128.5 billion, nearly $45 billion more than in 2022. Operating margin has been at exceptionally high levels for a long time, confirming that Microsoft can generate huge profits even with massive investments in future growth. This effect is also evident at EBIT and EBITDA levels, which remain robust and provide the company with considerable financial flexibility.

Net income and earnings per share have followed this trend over the long term. Net income rose from US$72.7bn in 2022 to US$101.8bn in FY2025, while EPS increased from US$9.70 to US$13.70. The key factor here is the virtually stable number of shares outstanding, which means that earnings growth is being passed on to shareholders very effectively. This is one of the main reasons why Microsoft has long been seen as a high-quality compounder.

News

During the quarter, Microsoft continued to expand its AI feature offerings across Azure, Microsoft 365 and Dynamics, with an emphasis on enterprise deployment and security. The company also continued to integrate Copilot into key products and expanded collaboration with strategic customers across industries. These moves reinforce Microsoft's long-term position as a leading provider of AI infrastructure for the enterprise sector.

Shareholder Structure

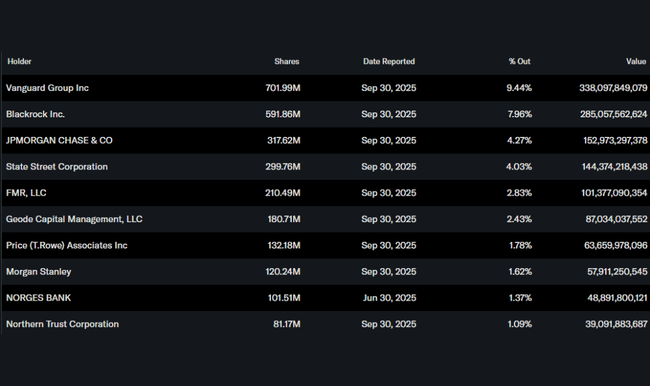

The shareholder structure remains strongly institutional. Institutions hold approximately 76% of the shares, with Vanguard (9.4%), BlackRock (8.0%), JPMorgan (4.3%) and State Street (4.0%) being the largest shareholders. Low insider ownership is a long-standing standard at Microsoft and does not imply poor alignment of interests, as management stock compensation plays a key role.

Analyst expectations

The analyst consensus after earnings remains strongly positive. Wall Street particularly appreciates Azure's acceleration, record contract levels and the return of operating leverage. Although Microsoft's valuation is well above the historical average, analysts defend it with a combination of visible growth, strong cash flow and a dominant position in the AI ecosystem. Thus, for many investors, Microsoft continues to represent a "safe way" to participate in the AI megatrend without extreme risk.

Fair Price

Why Microsoft stock is down after earnings:

Extremely high expectations were already priced in - While the results showed strong double-digit growth in both revenue and profitability, the market expects not just "strong numbers" from Microsoft at this stage, but acceleration. Azure growth of 39% and cloud growth of 26% were very good, but did not represent a significant acceleration from the previous quarter, which at current valuations is not enough to move the stock up further.

Cost and ROI concerns on AI investments - Microsoft is investing massively in AI infrastructure, data centers and development, which while supporting the long-term story, increases uncertainty around margins and free cash flow in the short term. Some investors are choosing caution after the results and realizing gains until it is clear how quickly AI investments will translate into further earnings acceleration.

Valuation sensitivity in the late-cycle megacap - Microsoft is now perceived as a "safe AI play," which has put the stock at high multiples relative to its historical average. In such an environment, even a slightly cautious tone to the outlook or the absence of a significant positive surprise leads to an immediate downward market reaction, not because the story has broken, but because the room for error is minimal.