Visa continues to exemplify what a high-quality global payments business looks like in execution. Volumes are growing, cross-border activity remains resilient, and operating leverage is working exactly as designed. In most environments, that combination would be enough to justify a positive market response. In this one, it merely confirms what investors already assumed.

The reaction highlights a familiar tension for mature compounders. With expectations already set at an unusually high level, the market is no longer rewarding consistency alone. Investors are scanning for signs of renewed acceleration, either through faster volume growth or incremental margin expansion. The quarter delivered strength, but not surprise, and that distinction matters when valuation reflects near-perfection.

What was the last quarter like?

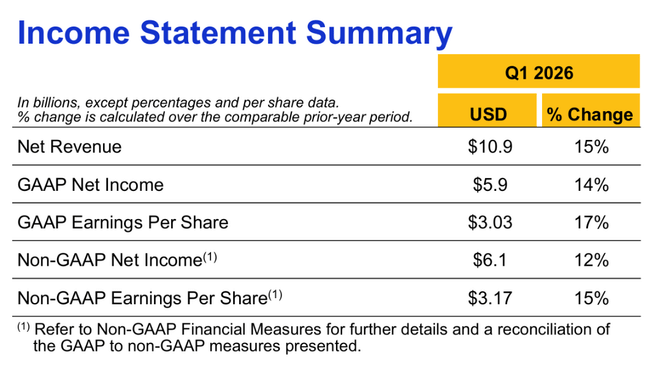

Visa $V reported net sales of $10.9 billion in Q1 FY2026, up 15% year-on-year, or 13% after adjusting for currency effects. Growth was primarily driven by higher payment volumes, continued recovery in cross-border transactions and solid processed payments momentum.

GAAP net income was $5.9 billion, up 14% year-over-year, while GAAP earnings per share increased 17% to $3.03. Adjusted for one-time items, non-GAAP earnings were $6.1 billion and EPS was $3.17, up 15% year-over-year. Even on a constant currency basis, the EPS growth rate remains around 14-16%, which is still a very robust performance for a company of this size.

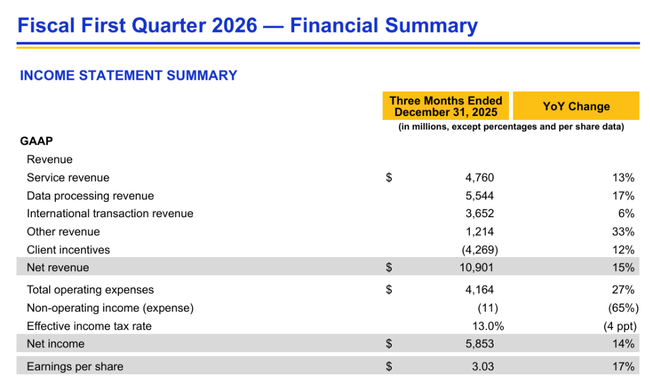

At the operating level, the numbers were also consistent. Payment volume was up 8%, total cross-border volume up 12% and cross-border volume outside Europe up 11%, confirming that international travel and online transactions remain strong structural drivers of growth. The number of transactions processed reached 69.4 billion, an increase of 9% year-on-year.

The revenue structure shows a healthy mix. Service revenue grew by 13% to $4.8 billion, data processing revenue by 17% to $5.5 billion and other revenue by an even 33% to $1.2 billion. The weakest point remains the relatively slower growth in international transaction revenues, which added "only" 6%, one area where the market was expecting more acceleration.

On the expense side, there was a visible increase. GAAP operating expenses were up 27%, primarily due to higher legal reserves related to ongoing litigation. Adjusted for these items, cost growth was 16%, still faster than revenue growth. This is one of the factors that have cooled investors in the short term.

CEO commentary

CEO Ryan McInerney called the quarter very strong and highlighted that Visa benefited from a combination of resilient consumer demand, a strong holiday season and continued expansion in value-added services, commercial payments and money movement solutions. A key strategic message is that Visa is systematically shifting from a pure transaction infrastructure to a broader payments hyperscaler platform that can serve increasingly complex client needs.

It is clear from his comments that the company has long been betting on scalability, technological depth and extending services beyond just payment processing. It is this strategy that is set to be a major source of sustainable growth in an environment where the core payments business is gradually approaching maturity.

Long-term results

A look at recent years confirms the extraordinary consistency of the business. Visa's revenues have grown from approximately $29.3 billion in 2022 to $40 billion in 2025, an average annual growth rate of more than 11%. Each year has delivered double-digit revenue growth, even in a slowing global economy.

Net income has increased from just under $15 billion to over $20 billion over the same period, while EPS has grown from around $7 to over $10. Not only did earnings growth play a significant role, but the systematic decline in share count through aggressive buybacks also boosted earnings per share even in an environment of slightly lower sales growth.

Operating profit and EBITDA have also shown steady growth, although the pace has slowed over the past year. This suggests that Visa is entering a phase where growth will be more dependent on monetization of added services than on transaction volume alone. Fundamentals remain extremely strong, but the scope for margin expansion is less than a few years ago.

News

Legal disputes around interchange fees remain a significant theme of the quarter, with Visa entering into an updated settlement agreement in November, but this is still subject to court approval. The company also deposited $500 million into an escrow account, de facto reducing the number of shares in a similar fashion to the buyback.

Continued discipline is evident in the capital allocation. During the quarter, Visa repurchased approximately 11 million shares for $3.8 billion and still has more than $21 billion authorized for additional buybacks. At the same time, regular dividend growth was confirmed.

Analysts' expectations

The market reaction suggests that analysts and investors were very well prepared for this quarter. The consensus had already anticipated double-digit growth in sales and earnings, and therefore meeting or slightly beating expectations was not enough on its own to positively revalue the stock. The main question for the coming quarters remains whether Visa will be able to re-accelerate its cross-border revenue growth while maintaining cost discipline.