SoFi delivered fourth quarter 2025 results in very strong growth mode: surpassing the $1 billion quarterly revenue mark for the first time ever while maintaining continued GAAP profitability. On paper, this looks like the textbook combination of growth and profitability that the market typically rewards in fintechs.

But it's with SoFi that the narrative often breaks down after such a significant sprint: investors want to see clearly how record growth translates into steadily higher margins, what the pace of monetization of the one-stop shop will be outside of credit, and what the latest move toward crypto and blockchain realistically means in the context of regulation, costs, and risk management. Therefore, even with strong numbers, the market's reaction may be "mixed" - not because of what has happened, but because of what should be sustainable from it.

What was the last quarter like?

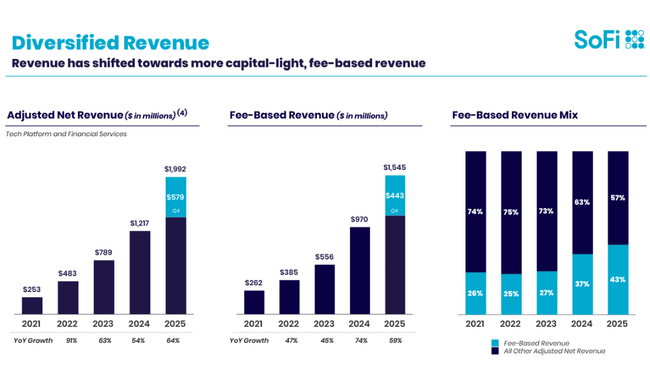

The quarter ended with record revenue and operating performance for SoFi $SOFI. Total GAAP net revenue came in at $1.025 billion, up 40% year-over-year from $734 million. USD. On an "adjusted" basis, the firm reported adjusted net revenue of $1.013 billion, up +37% year-over-year. This is important not only symbolically because of the billion-dollar mark, but mainly because growth is not built on one leg alone: the firm explicitly mentions strengthening the fee-based component and scaling the product ecosystem.

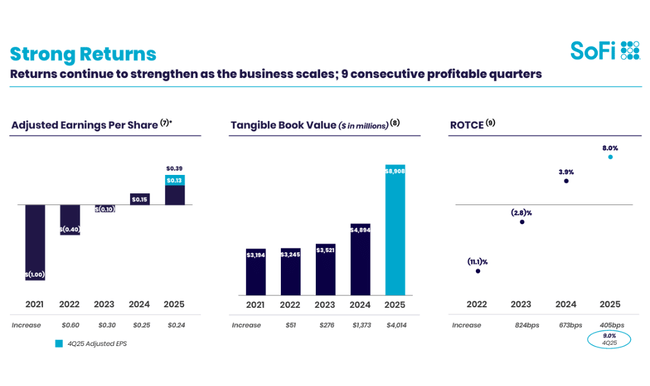

Profitability, meanwhile, has moved into a different league. Adjusted EBITDA (Adjusted EBITDA) jumped to a record $318 million. GAAP net income was $174 million, up +60% year-over-year, corresponding to an Adjusted EBITDA margin of 31%. The company also points out that this is the ninth consecutive quarter of GAAP profitability, a key signal of stabilizing unit economics and cost discipline in a business that until recently "bought growth."

The "engine" of net interest income and financing is also strong. Net interest income was $617 million. The net interest income was USD 617 million (+31% year-on-year). Net interest margin was 5.72% (-19 bps y/y from 5.91%), which SoFi explains mainly by mix - relatively more volume is shifting from high-yield personal loans towards mortgages and student loans. At the same time, the firm describes a significant improvement on the funding cost side: the average rate paid on deposits was 181 bps lower than on warehouse funding, which management translates into c. $680mn of funding. The company has seen USD 680 million in annualized interest cost savings. In practice, this means that the bank balance sheet and deposit base are starting to act as a real competitive advantage, not just a "regulatory costume".

Operationally, SoFi added a record 1.027 million new members in a single quarter to get to 13.7 million members (+35% YoY). More importantly, product depth: 1.6 million products were added in the quarter, bringing the total to 20.2 million (+37% YoY). In addition, management emphasizes the quality of cross-sell: 40% of new product openings came from existing members, with a year-over-year improvement of nearly 7 percentage points. This is exactly the mechanism to turn a one-stop shop into a long-term efficient growth machine - cheaper acquisitions, higher LTV and better margins.

CEO commentary

Anthony Noto builds the results story on three pillars: scaling the platform, accelerating the product ecosystem, and moving to the "next phase" of financial services. In his interpretation, the quarter is groundbreaking mainly because SoFi exceeded $1 billion in quarterly revenue for the first time, while adding 1 million members for the quarter and growing its product base by a record 1.6 million. These are the metrics that are supposed to prove that the one-stop shop model really works - people don't just come for one thing, but gradually pick up other products within the ecosystem.

The second level of his comment is more strategic: Noto explicitly emphasizes "crypto and blockchain innovation," noting that SoFi wants to be a "bank-grade" player in crypto and tokenized flows - that is, combining innovation with the security and stability of a national banking license. The CEO frames this as an effort to "lead the next phase of financial services," which is an ambitious narrative, but it also automatically opens up questions for investors: what will be the regulatory and compliance costs, what is the return on investment, and how quickly will these initiatives translate into fee-based returns.

Outlook

What is fairly clear from the quarter and management commentary are the key variables that the market will be pricing in 2026. First, the growth rate of fee-based revenue: in 4Q it reached 443 million. The company presents it as a structural driver of diversification beyond the pure credit cycle. Second, NIM stability and order quality: SoFi says credit performance is within expectations and charge-offs on personal loans improved 57bp y-o-y. Third, capitalization and return on capital: the firm said equity rose $1.7bn in the quarter to $10.5bn and that this includes $1.5bn of new capital - and this is often viewed sensitively by the market as higher capital improves safety but also raises the bar on ROE and can mean dilution.

Long-term results

Looking at recent years, SoFi has followed the classic trajectory of "growth at a loss → operational stabilization → first profitability". Revenues have grown very rapidly between 2021 and 2024: from $1.088bn in 2021 to $1.763bn in 2022, then to $2.898bn in 2023 and $3.704bn in 2024. This is an expansion that would mean nothing in itself if it went purely through marketing and acquisition subsidies, only that at the same time the cost profile and especially the ability to monetise has gradually changed.

The gross profit grew from 977 million euro to 977 million euro. USD 1.519 billion (2021) to USD 1.519 billion (2022), USD 2.053 billion (2023) and USD 2.581 billion (2024). Interestingly, OPEX has virtually stabilized in 2024: operating expense was $2.347 billion, -0.3% year-over-year versus $2.354 billion in 2023. This stabilization of OPEX is often the point at which growth companies begin to "tip" into profitability - because the next dollar of revenue no longer needs the same portion of fixed costs.

And that tipping point is visible on the bottom line. Operating income was negative in 2021 (-$481 million), also negative in 2022 (-319 million), remained negative in 2023 (-$301 million), but turned positive in 2024 to $233 million. Net profit in 2024 was USD 499 million. USD 499 million compared to a loss of USD -301 million in 2024. USD -320 million in 2023 and USD -320 million in 2023. EPS therefore went from negative (e.g. -0.36 in 2023) to positive (0.46 in 2024), which is a major change for valuation and the investor "universe" as it opens up completely different types of models and investors.

The 2025 picture fits in as well: for the full year, the company reported GAAP total net revenue of $3.613 billion (+35% YoY) and adjusted net revenue of $3.591 billion (+38% YoY), with adjusted EBITDA for the year of $1.054 billion (+58% YoY). In other words, SoFi is no longer just a growth story, but a growth story that is starting to "pay" for itself while growing faster in operating profit than in revenue - and that is exactly the return of operating leverage that the market is looking for in digital finance.

News

The most important "news" of the quarter is not a one-off event, but a strategic shift: in 4Q, SoFi announced that it became the first national bank (within its charter structure) to launch crypto trading for consumers, while simultaneously launching its own stablecoin, SoFiUSD, on a public permissionless blockchain. It added blockchain-powered international remittances to more than 30 countries. Management frames this as an effort to combine modern crypto products with banking security and stability.

From an investment perspective, however, this is not just an extra "feature". It's a bet that further growth in fee-based revenue and engagement will come not just from lending, but from the infrastructure around payments, remittances, investing and new types of financial flows. If successful, this could improve diversification and margins. If it fails, it can increase the cost base and regulatory friction without adequate monetization. So the market will want to see concrete metrics on adoption, profitability and compliance costs, ideally during 2026.

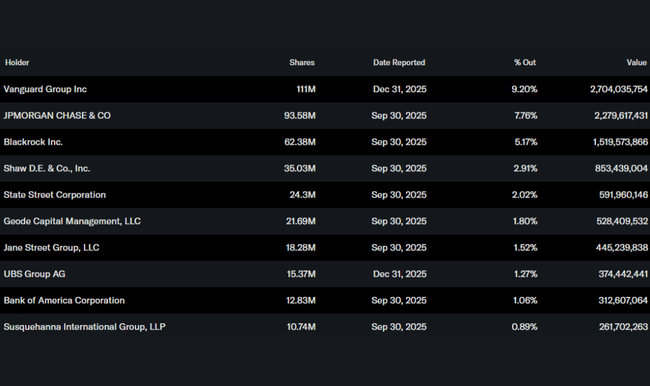

Shareholder structure

SoFi has a relatively "classic" structure for a growth financial technology: insider holdings are at 3.0%, institutional holdings at 52.64% (float 54.27%). This means the title is largely in institutional hands, but still has a significant retail market share, which may increase sensitivity to quarterly surprises and narrative changes around guidance.

The largest institutional holders include Vanguard with about 111 million shares (as of December 31, 2025), followed by JPMorgan (93.6 million), BlackRock (62.4 million) and Shaw (35.0 million). For investors, it's practical to watch mainly to see if the trend changes for the largest holders in subsequent quarters - SoFi is the type of stock where "positioning" often follows confidence in the long-term profitability model.