As payment volumes continue to expand, the real differentiator is no longer usage alone, but monetization. Mastercard’s latest quarter illustrates this shift clearly. Transaction growth remains strong, yet the more important driver sits in the layers built on top of the network—security, authentication, data, and value-added services that deepen relationships and lift margins beyond what pure volume growth could deliver.

That dynamic becomes even more visible in cross-border activity. International spending, typically the most profitable part of the business, accelerated meaningfully and amplified operating leverage. Combined with disciplined cost control, this translated into margin expansion and faster EPS growth. For investors, the appeal lies in consistency: revenue growth, margin improvement, and earnings acceleration reinforcing each other rather than competing for attention.

How was the last quarter?

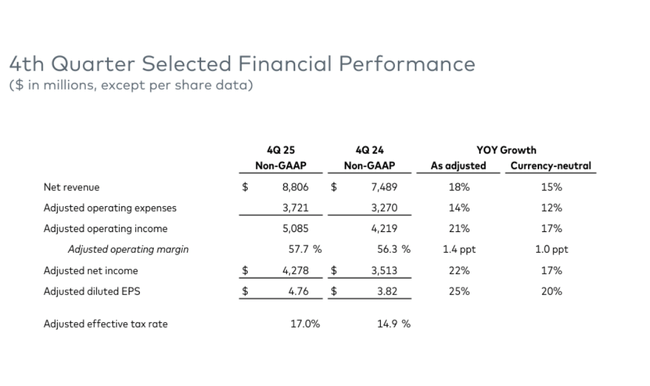

In Q4 2025, Mastercard $MA reported net sales of $8.8 billion, up 18% year-over-year, or 15% on a currency-neutral basis. Operating profit rose to $4.9 billion, up 25%, clear evidence that growth was not "bought" by costs, but that the company was able to leverage its operating leverage. Operating margin rose to 55.8% from 52.6% a year ago, up 3.2 percentage points. Net income came in at $4.1 billion, up +22% year-over-year, and diluted earnings per share increased to $4.52, up +24% year-over-year. On an adjusted basis (after adjusting for selected effects), the company reported adjusted net income of $4.3 billion and adjusted EPS of $4.76, up +25% year-over-year.

The key is that growth was driven by real transaction activity, not a one-time effect. Gross dollar transaction volume grew 7% in local currency terms to $2.8 trillion. Purchase volumes grew even faster, +9%, and the number of "switched transactions" increased by 10%. But the cross-border segment is the most important for monetisation: cross-border volumes grew by 14% in local currency. This is an area that typically generates above-average revenue per unit volume and therefore has a disproportionate impact on both revenue and margins. In other words, even relatively 'normal' growth rates in domestic payments can be offset by a higher proportion of cross-border activity.

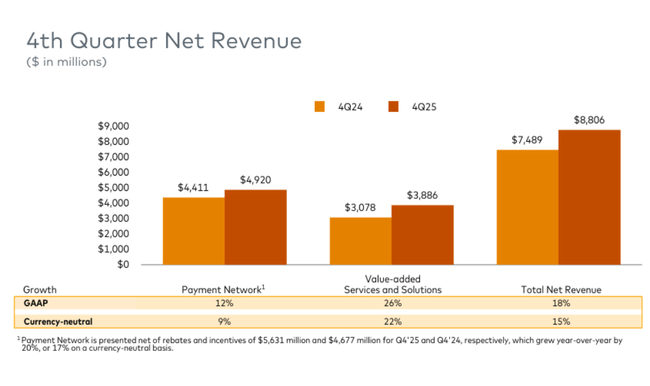

The revenue structure has again shown why Mastercard is not just a pure "payment network". Payment network revenues grew 12% (currency neutral 9%), while value-added services and solutions grew 26% (currency neutral 22%). Here is the strategic point: these services typically carry higher margins, better repeatability and greater cycle resilience as banks and merchants address security, identity, fraud management, authentication or data analytics without regard to short-term fluctuations in consumption. But at the same time, the firm acknowledges competitive pressure in the form of partner incentives: rebates and incentives in the payments network grew 20% (17% currency neutral), which is consistent with an environment where programs are negotiated harder and renewals have a higher price. On the positive side, Mastercard has so far offset this pressure with revenue and margin growth.

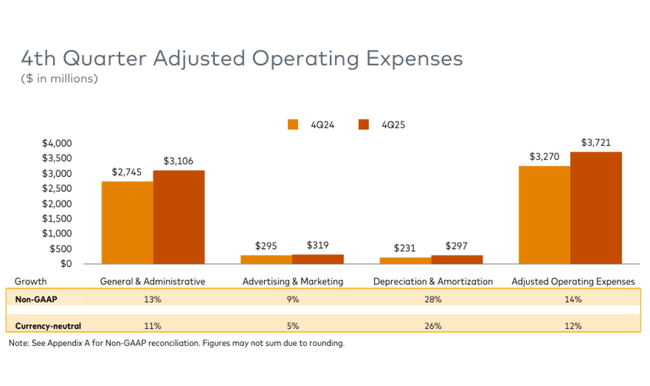

On the expense side, operating expenses grew 10%, slower than revenue, which explains the expansion in operating margin. On an adjusted basis, expenses grew 14% (12% currency neutral), partly due to acquisitions, and the rest went mainly to higher general and administrative expenses. The tax rate in the quarter rose to 16.7% from 14.1%, and the adjusted rate also moved to 17.0% from 14.9%, which the company attributed primarily to the effect of the global minimum tax and geographic mix of earnings. In practice, this means that net income and EPS may be partially "dragged" by taxes going forward, even as operating performance remains strong.

CEO commentary

CEO Michael Miebach described 2025 as another strong year, with net sales up 16% year-on-year (15% currency neutral) and the company, he said, "winning" through a combination of technology confidence, innovation and partnerships. He specifically mentions programs like Apple Card, which illustrate Mastercard's ability to win large and strategically important contracts. At the same time, he builds an investment thesis on the growth of value-added services and solutions, which grew 23% in 2025 (21% currency neutral), confirming the firm's strategic shift away from a pure transaction network and toward a platform over payments.

The key takeaway from his comments is that management sees the results not just as a product of "good macro" but as a result of diversification and the ability to monetise new layers of value - security, digital and authentication solutions, data, engagement and services for merchants and businesses. He also says the company is "agile and diversified" and therefore well positioned to take advantage of opportunities in 2026, which is usually a signal that management expects continued healthy consumption and that it sees investments in products and partnerships as well-timed.

Outlook

Management enters 2026 with expectations of continued double-digit growth, despite less favourable currency effects and a higher tax burden. For the full year 2026, Mastercard is targeting net sales growth at the high end of the "low double digits," approximately around 10-12%, and this outlook is consistent across GAAP and non-GAAP metrics. Adjusted for currency effects and acquisitions, organic, currency-neutral revenue growth should also remain at the high end of low double digits, confirming that the core of the expansion remains the payments business itself and higher value-added services, not one-off effects.

On the cost side, Mastercard expects operating expenses to grow faster than revenue, specifically at the upper end of high single digits, around 7-9%, reflecting continued investment in technology, security, data solutions and value-added services. The outlook also includes a restructuring charge of approximately $200 million in the first quarter of 2026, which is not intended to reduce costs in the short term, but to free up space for reinvestment in long-term growth initiatives. Management also emphasizes that these costs should not disrupt the long-term trajectory of margins.

Profitability should remain robust despite the higher cost base. Mastercard also expects non-GAAP operating profit to grow in the low double-digit range, with operating margin expected to remain above 57%, although the pace of expansion will be more moderate than in 2025. N

Long-term results

The long-term numbers for 2022 to 2025 show a consistent "compounding" pattern: revenue growth, earnings growth and even faster EPS growth through a combination of margins and share buybacks. Revenues have grown four years in a row: reaching $22.237 billion in 2022, rising to $25.098 billion in 2023, $28.167 billion in 2024, and $32.791 billion in 2025. The growth rate was double-digit in all years, accelerating to +16.4% in 2025, reflecting a strong mix of cross-border and value-added segment growth, which the company itself describes as a key driver.

Operating profit rose from $12.264 billion in 2022 to $14.008 billion in 2023, then to $15.582 billion in 2024 and $19.401 billion in 2025. Here we see the typical operating leverage: in 2025, operating profit grew faster than sales (+24.5%), which also explains why the market often pays a premium for quality and margin stability at Mastercard. Net profit grew at a similarly consistent rate: $9.93 billion (2022), $11.195 billion (2023), $12.874 billion (2024) and $14.968 billion (2025). Net profit growth in 2025 was +16.3%, broadly similar to sales growth but achieved despite a higher tax burden.

However, the trend in EPS is the most convincing, as it combines profitability growth and the buyback effect. Diluted EPS rose from $10.23 in 2022 to $11.83 in 2023, $13.89 in 2024 and $16.52 in 2025. That's a cumulatively very strong shift that's not just about business growth, but also about the share count declining over the long term. The diluted average share count has declined from 971 million in 2022 to 946 million in 2023, 927 million in 2024 and 906 million in 2025. It is this combination - volume growth, service growth, high margins and a systematic reduction in share count - that has long been at the heart of the investment thesis.

News

The results and commentary show that Mastercard continues to accelerate in areas beyond net transaction fees. Most notable is the growth in value-added services and solutions, where the company is benefiting from demand for digital security, authentication, fraud prevention and data services. At the same time, management signals that it is closing and renewing key programs even at the cost of higher incentives, which is typical in the current competitive environment. In practical terms, it's a battle for distribution and long-term relationships with banks, fintechs and large partners - and if Mastercard can grow faster than payment network volumes, it means it's succeeding in expanding monetization "beyond" transactions.

Shareholding structure

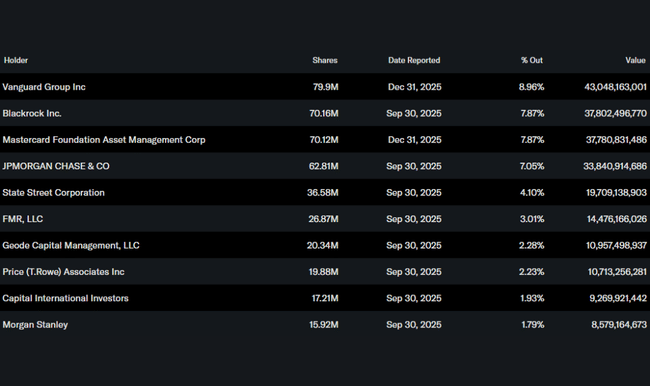

Mastercard's shares are typically very heavily owned by institutions: institutions hold around 91% of the shares and the free float is around 92% institutionally owned. The largest shareholders include Vanguard, BlackRock, Mastercard Foundation Asset Management and JPMorgan. This typically implies a stable ownership base, but also sensitivity to institutional rebalancing during periods of changing macro expectations, particularly around consumption, travel and global growth.

Analyst expectations

From an analyst perspective, the outlook for Mastercard remains positive, even after very strong results. For example, Reuters pointed out after the numbers were released that Mastercard is benefiting from resilient consumer and corporate demand, strong cross-border payments growth and high operating leverage, with analysts expecting the company to be able to maintain double-digit revenue growth in the "low-teens" range and continued earnings per share growth in 2026, despite modest pressure from higher costs and restructuring expenses. At the same time, Reuters points out that it is the combination of a payments network and fast-growing value-added services that makes Mastercard one of the best-performing titles in global fintech.