PayPal’s fourth-quarter results underline a business that remains profitable and cash-generative, even as growth initiatives struggle to regain pace. Over the past year, the company improved transaction margins, diversified revenue streams, and delivered solid EPS expansion, confirming that the platform can operate effectively in a more challenging macro environment.

The pressure point lies elsewhere. Management acknowledged that execution in key areas, particularly branded checkout, fell short of expectations, triggering leadership changes aimed at improving performance. For investors, the issue is no longer stability, but direction. With competition intense across checkout solutions, the market is looking for clearer evidence that growth can reaccelerate rather than merely hold its ground.

Quarterly results

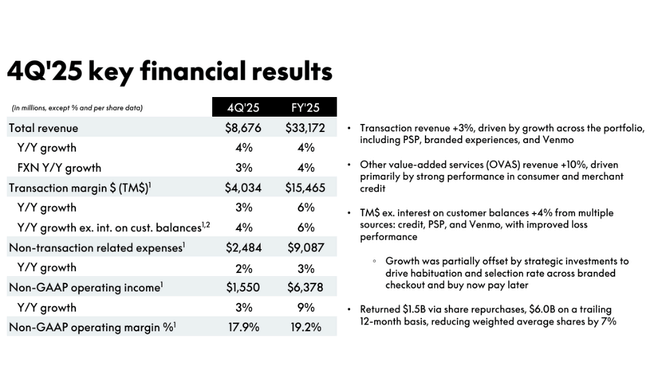

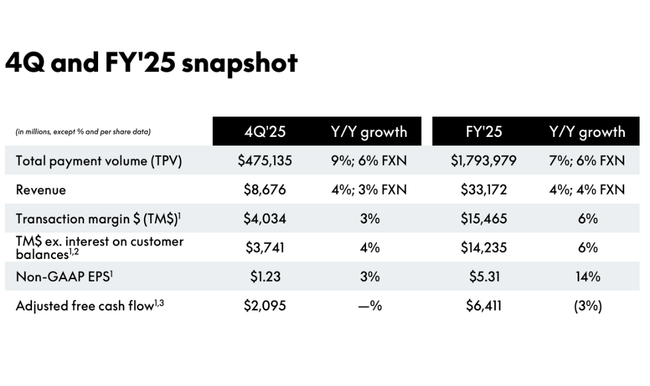

In the fourth quarter of 2025, PayPal $PYPL reported net sales of $8.7 billion, up 4% and 3% year-over-year, respectively, when adjusted for currency effects. While this growth is more modest than the pace of some fintech competitors, it is indicative of solid resilience in the underlying business.

Transaction margin - a key metric for payments companies - rose 3% to $4.0 billion, and 4% after adjusting for interest on customer balances, confirming that the core payments business is generating a solid profit base. GAAP operating profit was $1.5 billion (+5%), and non-GAAP operating profit was $1.6 billion (+3%), resulting in stable GAAP operating margin of 17.4% and non-GAAP operating margin of 17.9%. In terms of net income, Q4'25 was one of the best quarters in recent memory with net income of $1.44 billion and GAAP earnings per share of $1.53 (+38%).

Payment activity was also robust, with total payments volume (TPV) reaching $475.1 billion (+9%), with the number of payment transactions growing 2% to 6.8 billion. When PSP transactions (i.e. transactions facilitated by third-party service providers) are removed, the number of payments grew by 6%, showing that transaction growth is still organic in the primary business. Active accounts increased by 4.7 million to 439 million, further confirming PayPal's ability to attract and retain users despite a highly competitive environment.

Focusing purely on profitability, GAAP EPS of $1.53 represents a significant improvement over prior years and reflects efficient cost management, higher transaction margins and improved platform monetization. Non-GAAP EPS of $1.23 also grew (+3%), with performance driven primarily by the core payments segment.

At the same time, the company announced that its board of directors has appointed Enrique Lores as its new president and CEO with the clear goal of stepping up execution of looming growth initiatives, particularly in the area of custom checkout solutions, which has been identified as a weak link in recent results.

🔴 Reasons for share price decline: CEO change, missed EPS, cash flow and revenue estimates, weaker 2026 outlook.

Outlook

For fiscal year 2026, PayPal provided an outlook that was slightly below expectations, predicting earnings per share of $5.75 versus the consensus estimate of $5.73. The company also warned of a single-digit decline in Q1 2026 earnings.

CEO commentary

Interim CEO Jamie Miller took an unusually candid tone in her comments. She acknowledged that although PayPal was able to grow across sales, margins and earnings per share in 2025, the company's execution lagged particularly in branded checkout, a key consumer payments product. It was this weakness, according to management, that led to the decision to replace the CEO and bring in Enrique Lores to lead the company.

The management thus de facto confirmed what the market has feared for a long time - PayPal is losing relevance with merchants and consumers in an environment where competitors offer simpler, faster and better integrated payment solutions. At the same time, the words about "investing in future growth" suggest that short-term profitability will be sacrificed in favor of restructuring the product and user experience.

Long-term results

The long-term performance of PayPal $PYPL over the last four fiscal years shows that the company has been able to maintain steady revenue growth despite significant macro pressures and transformations in the payments industry. Revenues have grown continuously: $25.4 billion in 2021, $27.5 billion in 2022, $29.8 billion in 2023 to $31.8 billion in 2024. The growth rate has been in the range of 6-8% per annum, confirming the increasing monetization of existing clientele and diversification of the business across both payment and non-payment segments despite the relatively low growth rate.

In terms of profitability, the company has gradually increased its operational efficiency in recent years. Operating profit grew from $3.8 billion in 2022 to $5.0 billion in 2023 and $5.3 billion in 2024, indicating that the firm was able to improve margins despite slower revenue growth. Net profit showed very strong year-on-year fluctuations - from $2.4 billion in 2022 to $4.2 billion in 2023 and $4.1 billion in 2024. The main reasons were changes in cost structures, tax effects and one-off items related to investment activity.

Long-term earnings per share (EPS) grew steadily, from approximately $2.09 in 2022 to nearly $4.03 in 2024, with the number of shares outstanding declining in recent years, supporting EPS growth despite relatively moderate net income growth.

Cash flow remains a strong aspect of the business, as evidenced by steady operating cash flow in excess of $6 billion per year and free cash flow of over $5.5 billion in 2024, although the absolute value of this has declined slightly in 2025 due to investment and timing effects in our business.

Shareholding structure

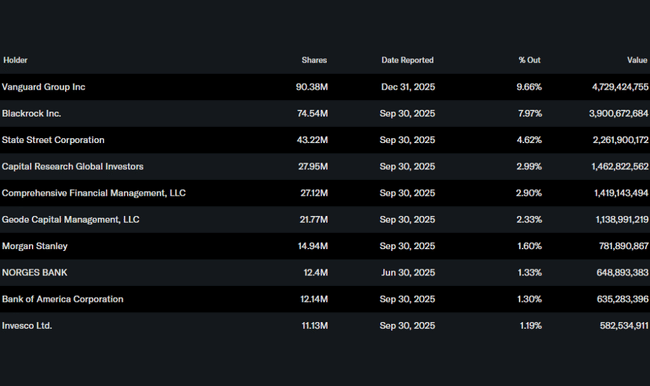

Over 81% of PayPal's shares are held by institutional investors. The largest shareholders include Vanguard Group with ~9.7% stake, BlackRock with ~8.0% and State Street with ~4.6%. The low share of insiders (only ~0.15%) signals that management and the board do not predominantly maintain large equity positions, but this is consistent with the typical structure of publicly traded fintech firms with an emphasis on institutional ownership.

Analysts' expectations

Analysts generally appreciate the stable revenue growth, significant free cash flow and solid margins, but caution that the pace of growth has been moderate in recent years and that PayPal faces significant competitive pressure, particularly in the checkout and digital payment solutions space. Consensus target prices are typically in a range that reflects a moderately positive outlook, while not assuming a dramatic acceleration in growth. Some banks, such as Citi and Barclays, rate the stock a Hold with target prices around $70-75, while others, such as Wells Fargo, see upside potential from improved margins and cash flow with target prices around $80-85.