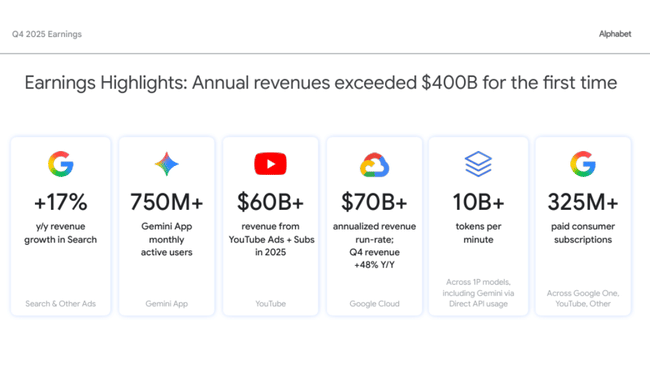

Alphabet closed out 2025 with an exceptionally strong quarter, surpassing $400 billion in annual revenue for the first time in its history. The numbers confirm that the core business - search, YouTube and cloud - remains structurally very strong, benefiting from massive deployment of AI across products and customer segments. In addition, growth clearly accelerated towards the end of the year, both at the level of revenue and operating profit.

At the same time, however, the results reveal the other side of the story: Alphabet is entering a new investment phase. Extremely high capital expenditures on AI infrastructure and the cloud, as well as one-off costs associated with Waymo, while not yet impairing profitability, make it clear that 2026 will be marked by pressure on cash flow and cost discipline. Thus, the market is not only assessing the strength of the numbers, but also the price the company is paying for this expansion.

How was the last quarter?

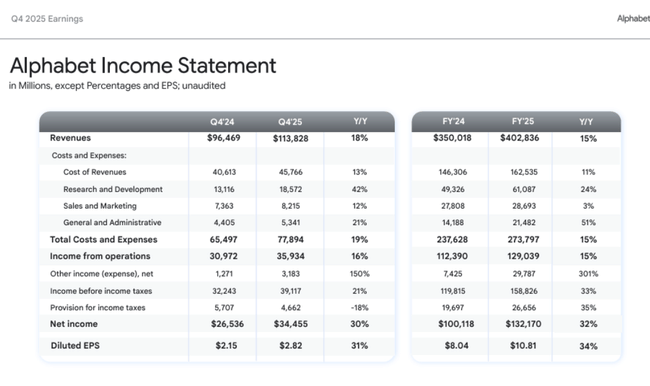

The fourth quarter of 2025 brought Alphabet $GOOG revenue of $113.8 billion, representing 18% year-over-year growth (17% at constant currencies). The acceleration in growth was evident across the board, with the main contributors being both Google Services and, in particular, Google Cloud. Compared to 4Q 2024, when revenue was $96.5 billion, this is one of the strongest quarterly improvements in years.

Operating profit in Q4 rose to $35.9 billion, up 16% year-over-year, while operating margin was 31.6%. That's a solid result, especially considering the fact that costs included a one-time $2.1 billion charge for employee stock compensation at Waymo. Without this effect, operating profit growth would have been even stronger and margins would have been higher.

Net income was $34.5 billion, up 30% year-over-year, and earnings per share (EPS) rose to $2.82, up 31% from $2.15 in the same period last year. The strong EPS growth was supported not only by strong operating performance, but also by a long-term declining share count due to extensive share buybacks.

In terms of segments, Google Services remains the key driver, with revenue growing to $95.9 billion (+14%). Search and related ad formats saw 17% growth, YouTube advertising added 9% and subscriptions, platforms and devices also grew 17%, confirming a shift to more stable, recurring revenue. Google Cloud was the star of the quarter, however, with revenues of $17.7 billion marking 48% year-over-year growth, while cloud operating profit jumped to $5.3 billion from $2.1 billion a year earlier. The cloud is clearly moving from the investment phase to a strong profitability phase.

CEO commentary

Sundar Pichai called the quarter spectacular and highlighted that Alphabet surpassed the $400 billion annual revenue mark for the first time in its history. A key theme of his comments was artificial intelligence, specifically the launch of Gemini 3, which he called a major technology milestone. According to management, Alphabet's own models now process more than 10 billion tokens per minute through direct API usage by customers, illustrating the real commercial adoption of AI.

Pichai also highlighted the rapid growth of the user base - the Gemini app has over 750 million monthly active users, while AI features in search continue to increase engagement. In the area of monetisation, he highlighted YouTube, which has annual revenues in excess of $60 billion, and the total number of paid subscribers across services has exceeded 325 million. The cloud, he said, entered 2026 with an annual run-rate of over $70 billion, driven by demand for AI infrastructure.

Outlook

Alphabet didn't explicitly offer traditional financial guidance at the revenue or profit level, but it did provide a very important signal in terms of investment. CapEx for 2026 is expected to reach $175 billion to $185 billion, an extremely high level and a significant increase from previous years. These investments will be primarily in data centers, AI infrastructure, custom chips and cloud capacity.

Management makes it clear that the goal is not short-term margin optimization, but long-term technology leadership. This means that despite strong revenue growth, the pace of margin expansion may be limited in 2026 and free cash flow burdened by high investment. This is a key point for investors - Alphabet's story is shifting from the "efficient growth" phase to the "strategic dominance at the cost of higher spending" phase.

Long-term results

Looking at the last four years, it is clear that Alphabet has undergone a significant transformation. Revenues have grown from $257.6 billion in 2021 to $402.8 billion in 2025, a combination of structural growth in digital advertising, cloud expansion, and a gradually expanding subscriber model. Meanwhile, the pace of growth has accelerated again after slowing in 2022, largely driven by AI-driven products.

The evolution of profitability is even more pronounced. Operating profit grew from $78.7 billion in 2021 to $129.0 billion in 2025, with a key factor being the slowdown in operating expense growth between 2023 and 2024 and subsequent operating leverage in 2025. This was reflected in net profit, which reached $132.2 billion, up more than 35% from a year earlier.

Earnings per share has been growing over the long term, not only due to net profit growth, but also due to a systematic reduction in the number of shares outstanding. The average number of shares has fallen from more than 13.3 billion in 2021 to about 12.2 billion in 2025, amplifying the effect of growth at the EPS level. Thus, over the long term, Alphabet combines business growth with a disciplined capital policy.

News

Aside from the results themselves, the developments around Waymo are particularly noteworthy, where Alphabet booked $2.1 billion in stock compensation in Q4 in connection with a new investment round. This confirms that autonomous driving remains a strategic but capital-intensive bet. The company also issued $24.8 billion of senior notes, bolstering financial flexibility ahead of massive investments in AI infrastructure.

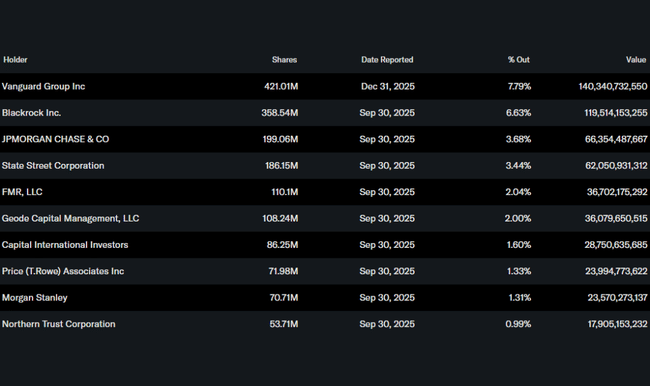

Shareholder structure

Alphabet's shareholder structure remains highly institutional. Approximately 61% of shares are held by institutional investors, with Vanguard, BlackRock, JPMorgan and State Street being the largest shareholders. The significant insider holdings primarily reflect the voting structure of the share class, rather than normal insider activity.

Analyst expectations

Analysts remain mostly positive on Alphabet, though they caution about near-term risks associated with the size of the investment. Goldman Sachs reiterated a Buy recommendation following the results, highlighting the acceleration of Google Cloud growth and the rapid monetization of AI products. At the same time, however, it cautioned that extremely high CapEx in 2026 may temporarily hamper free cash flow growth and keep valuations under pressure.

The market consensus is thus shifting to the view that Alphabet offers a very strong long-term growth story, but will be evaluated in the short term through the prism of returns on massive AI investments. For long-term investors, the key question remains whether today's spending surge will translate into sustained higher earnings capacity between 2027 and 2028.