Amazon closed the fourth quarter of 2025 in strong operating shape. Revenue grew at a double-digit pace, profitability improved across segments, and AWS reaccelerated at a moment when investors are looking for concrete proof that AI infrastructure can be monetized at scale. The numbers show a business capable of delivering record earnings even amid pricing and logistics pressures.

The market reaction, however, is driven by what comes next. Management is signaling an aggressive investment cycle spanning AI chips, data centers, and satellite infrastructure. While strategically logical, this push weighs on near-term free cash flow and raises capital intensity. The investment debate now centers on timing: how long investors are willing to accept weaker cash generation in exchange for future AI-driven growth.

How was the last quarter?

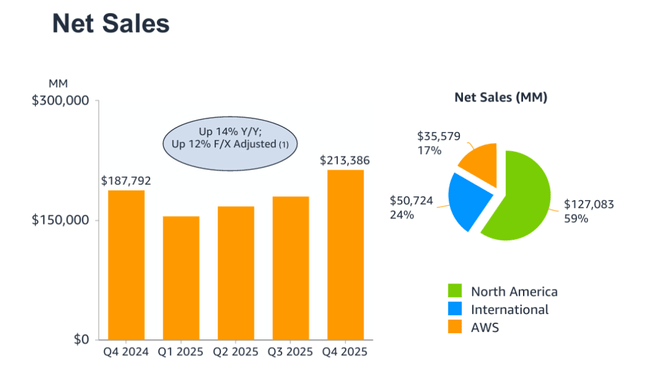

Amazon $AMZN reported Q4 2025 revenue of $213.4 billion, representing 14% year-over-year growth. Adjusted for currency effects, growth was still a solid 12%, confirming that demand remains strong across regions and segments. North America grew sales by 10% to US$127.1 billion, while the international segment grew 17% to US$50.7 billion, with double-digit growth even after adjusting for FX.

The AWS segment was again a key driver of the results, with revenues jumping 24% year-on-year to $35.6 billion. This is the fastest growth rate in 13 quarters and a clear signal that demand for cloud and AI infrastructure is continuing to accelerate. AWS also generated an operating profit of $12.5 billion, a significant improvement from $10.6 billion a year ago.

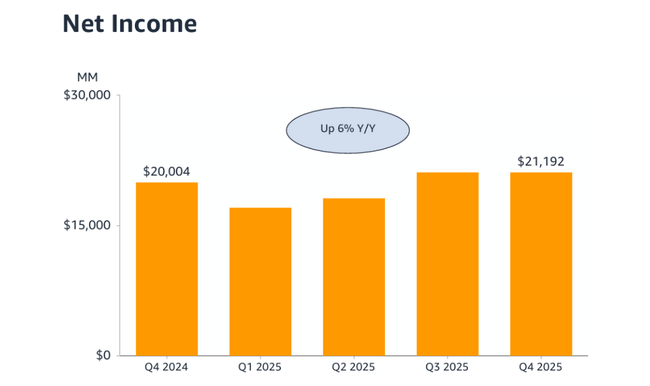

Amazon's total operating profit reached US$25.0 billion, up from US$21.2 billion a year earlier. Adjusted for one-off items, it would have been as high as US$27.4 billion. Net profit rose to US$21.2 billion, or US$1.95 per share, up from US$1.86 in Q4 2024. Profitability therefore grew across the group, despite pressure on international retail.

CEO commentary

CEO Andy Jassy called the quarter one of the strongest in the company's history and highlighted that AWS' growth acceleration is a direct result of its long-term investment in innovation. He said that AWS, advertising and retail are benefiting from the rapid deployment of new technologies, particularly in AI, custom chips and automation.

A crucial part of his comments, however, was about the future. Jassy openly confirmed that Amazon is planning capital expenditure of around $200 billion in 2026, mainly in AI infrastructure, data centres, its own Trainium and Graviton chips, robotics and the Leo satellite project. He said these are investments with very high returns over the long term, but also acknowledged that they will be a strain on cash flow in the short term.

Outlook

For the first quarter of 2026, Amazon expects revenue in the range of $173.5 billion to $178.5 billion, implying year-on-year growth of 11-15%. Operating profit is expected to reach $16.5 billion to $21.5 billion, with the mid-point of the range slightly below what the market was expecting. The outlook already explicitly includes higher costs associated with AI infrastructure expansion, rapid delivery and price investments in international retail.

It is this combination of strong revenue growth but pressure on margins and cash flow that is the main reason for the negative market reaction.

Long-term results

A look at recent years shows a significant structural turnaround in Amazon's profitability. Revenues have grown from $469.8 billion in 2021 to $638.0 billion in 2024, with growth rates steady around 10-12% per year. However, the fundamental change has come at the level of operating profit.

While Amazon struggled with a drop in operating profit and margin pressure in 2022, 2023 marked a stabilization and 2024 has already brought a full return of operating leverage. Operating profit for 2024 reached $68.6 billion, nearly doubling year-over-year, and net income jumped to $59.2 billion. This trend continues in 2025, with Amazon reporting full-year operating profit of $80.0 billion and net profit of $77.7 billion.

In the long term, it is evident that AWS has become a steady cash generator, while retail is once again contributing to margins after years of investment. It is this combination that gives Amazon the room to fund an extremely capital-intensive AI cycle.

News

Amazon $AMZN significantly expanded its AI portfolio in the past quarter. AWS has entered into new strategic agreements with dozens of global clients including large banks, technology companies and the public sector. Trainium and Graviton's proprietary chips have achieved a combined annual run-rate of over $10 billion and demand is growing at triple-digit rates.

The company has also introduced next-generation AI agents, expanded the Bedrock platform, launched advanced Nova models, and enhanced AI functionality in e-commerce through its Rufus assistant, which is already generating billions of dollars in incremental sales. These moves confirm that Amazon is not investing in AI defensively, but is looking to dominate the entire value chain.

Shareholder structure

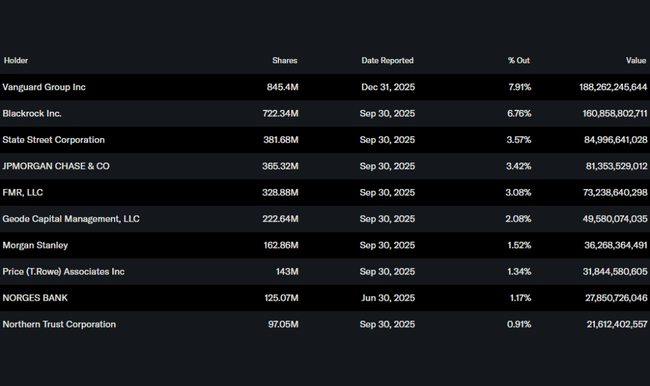

Amazon's stock is heavily owned by institutional investors, who hold approximately 67% of the shares. The largest shareholders are Vanguard, BlackRock, and State Street, which provides high stability in the ownership structure but also increases the stock's sensitivity to changes in cash flow and return on capital expectations.

Analyst expectations

Post-earnings, analysts agree that Amazon's operating performance remains very strong, but see increased risk in the near term in terms of capital intensity. For example, analysts at major US investment banks warn that planned investments of around USD 200bn per year may keep free cash flow under pressure over the next 12-18 months, although long-term return potential remains high.

Target prices are mostly above current market prices, but many analysts are lowering the short-term outlook and shifting the investment thesis more towards a multi-year horizon. The consensus can be summarized as Amazon is seen as one of the major winners of the AI era, but investors must accept a period of lower cash flow visibility and higher stock volatility.