CVS Health’s fourth-quarter and full-year results underline a business that continues to expand in scale and deliver record revenue, while operating in an increasingly complex US healthcare environment. Regulatory pressure, reimbursement changes and structural reforms are colliding with CVS’s long-term effort to reshape its business model. This is not a simple cyclical dip, but a multi-year transformation that raises short-term volatility and pushes investors to look beyond a single quarter.

In that context, 2025 was clearly transitional. Revenue growth held up across segments, adjusted operating performance improved and operating cash flow remained strong. At the same time, one-off impairments, legal costs and changes related to Medicare Part D distorted reported operating income and net profit. Understanding the gap between underlying business momentum and accounting results is central to the current investment case.

How was the last quarter?

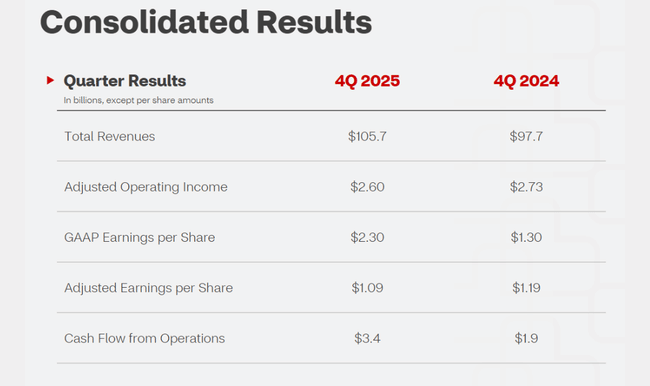

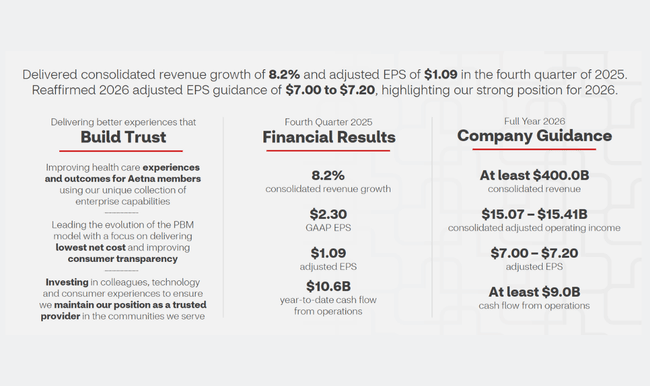

In the fourth quarter of 2025, CVS Health $CVS achieved total revenues of $105.7 billion, up 8.2% year-over-year. Growth was driven by all major segments - health insurance, health services and retail pharmacy. In terms of business volume, it was a strong quarter, confirming that demand for health services and pharmaceuticals remains robust even in an environment of higher costs and regulatory changes.

Operating profit on a reported basis, however, declined from $2.37 billion to $2.11 billion, down approximately 11% year-over-year. Adjusted operating profit was $2.60 billion, also down slightly from last year. The key negative factor was Aetna's health insurance segment, where the seasonality shift in the Medicare Part D program due to the reform measures resulting from the Inflation Reduction Act had a significant impact in the quarter. These changes led to higher year-end costs and impaired the segment's near-term profitability.

Earnings per share show the typical "double track" of CVS results. GAAP EPS increased to $2.30 from $1.30, driven by tax effects and one-time items, while adjusted EPS declined to $1.09 from $1.19. It is the adjusted numbers that better reflect the true operating trend and explain why the market is reacting more cautiously to the results than revenue growth alone would suggest.

Management commentary

CEO David Joyner's comments clearly set the results within a broader strategic framework. He emphasized that CVS is progressively fulfilling its ambition to become the "gateway" to U.S. healthcare - from pharmaceuticals to insurance to primary and preventive care. By 2025, he said, the company has taken tangible steps to simplify healthcare, reduce drug prices and improve patient navigation of the system.

From management's perspective, the key takeaway is that the business transformation is proceeding as planned, even if it is putting pressure on results in the short term. Joyner freely admits that regulatory changes and seasonal shifts in Medicare Part D complicate year-over-year comparisons, but emphasizes that the company's structural performance is improving. Thus, management clearly communicates that 2025 is an investment and transition year, while 2026 is intended to be a year of stabilization and a return to more predictable results.

Outlook for 2026

CVS confirmed full-year guidance for 2026, giving investors a clear point of reference. The company expects GAAP EPS in the range of $5.94-6.14 and adjusted EPS between $7.00-7.20. It also lowered operating cash flow expectations to at least $9 billion, reflecting a more cautious view of working capital and timing of payments in the insurance business.

The outlook implicitly assumes that the negative impacts of Medicare Part D reform will become more manageable and that improvements in operational discipline and cost control will help stabilize margins. Importantly for investors, CVS continues to generate strong cash to reduce debt and maintain its dividend policy.

Long-term results

Looking at the last four years, it is clear that CVS Health has gone through an extremely volatile period. Revenues have grown from $292 billion in 2021 to $373 billion in 2024, confirming a long-term growth trend driven by acquisitions, expansion of health services and growth in the insurance tribe. However, this growth has not been accompanied by stable profitability.

Operating profit has varied significantly from year to year, from $13.3 billion in 2021, to a dip in 2022, a strong recovery in 2023, and a significant decline in 2024, when goodwill amortization and restructuring charges impacted results. Net income followed this trend, with EPS ranging between extremes of around US$3.3 and nearly US$6.5.

The long-term picture thus shows a company with growing sales and a strong market position, but also a business vulnerable to regulatory intervention, accounting revaluations and structural changes in the US healthcare industry. It is the ability to stabilize operating margins that will be a key test of the next phase of the CVS story.

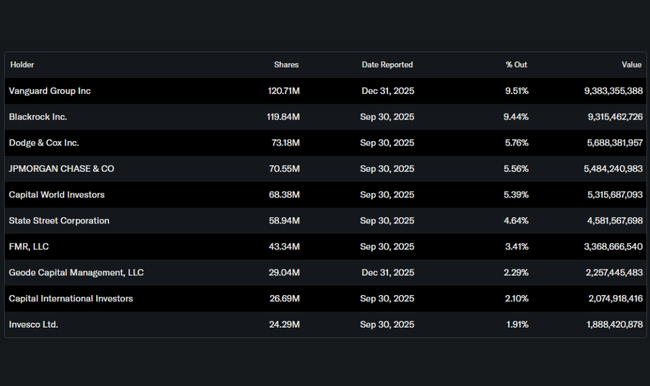

Shareholder structure

CVS has a very strong institutional base. Approximately 90% of the shares are held by institutional investors, which increases the emphasis on long-term return on capital and cash flow stability. The largest shareholders are Vanguard, BlackRock, Dodge & Cox, and JPMorgan, who view the firm as a strategic bet on US healthcare with a defensive nature but transformative potential.

Analyst expectations

Analysts are divided on CVS, but a cautious constructive view still prevails. For example, analysts at JPMorgan have long emphasized that near-term profitability pressure is the price of structural change and that a key catalyst will be the stabilization of the health insurance segment in 2026. The price target is in a range that implies moderate upside potential if the company confirms its ability to generate adjusted EPS above $7 and maintain strong cash flow.