Retail is increasingly split into two businesses living under one ticker. One is the large, steady store network that wins on scale and price. The other is higher-margin growth layers like e-commerce logistics and advertising. When those layers start to contribute meaningfully, the conversation shifts from “defensive retailer” to “cash machine with optionality.” Q4 2025 showed more of that shift.

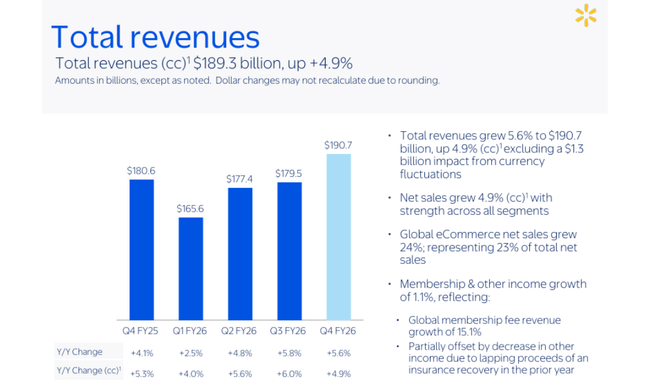

Walmart posted revenue of $190.7B, up 5.6%, while operating income rose faster at 10.8%. Globally, e-commerce grew 24%, and advertising continued to accelerate, both pointing to a better long-term margin mix than pure retail. The stock reaction, however, was shaped less by Q4 and more by what Walmart did not promise: management signaled continued growth but avoided aggressive EPS expectations for the year ahead. Even with a new $30B share repurchase authorization, that “strong quarter, restrained outlook” mix is why the report landed as solid rather than catalytic.

How was the last quarter?

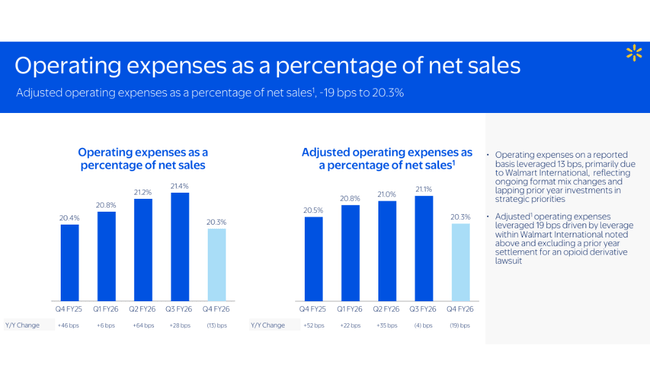

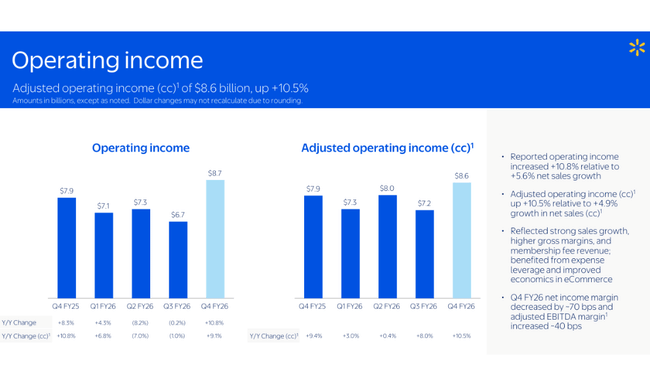

Walmart $WMT reported sales of $190.7 billion, up 5.6% year-over-year and 4.9% in constant currencies. Operating profit grew 10.8%, significantly faster than sales, and even after adjusting (in constant currencies) the company reports growth of around 10.5%. This is a key combination: when operating income grows faster than sales, it means that operating leverage, better mix and cost discipline are starting to filter through more into the results. The gross margin was helped by a 13 basis point improvement, primarily driven by the Walmart U.S. segment.

At the earnings per share level, Walmart reported GAAP EPS of $0.53 and adjusted EPS of $0.74. The difference is particularly important due to items related to revaluation/investment results: the company explicitly states that adjusted EPS excludes the impact of the (after-tax) net loss of $0.21 on equity and other investments. For an investor, this simply means that operating performance was stronger than how the GAAP number itself looks.

Digital was the main driver of the story. Global e-commerce grew 24%, and even 27% in the U.S. The company points out that growth was driven by store-fulfilled channels, i.e. pickup and delivery from stores. Expedited delivery from store-fulfilled channels grew more than 50% year-on-year, which is exactly the part that increases customer "stickiness" and improves purchase frequency. In the U.S., comparable sales excluding fuel grew 4.6%, with transactions up 2.6% and average spend up 2.0%. This shows that growth is not just through price inflation, but also through higher footfall and digital mix.

Advertising is adding a big contribution. Global advertising business grew 37% in the quarter (including VIZIO) and in the US Walmart Connect grew 41%. In addition, membership fee revenue grew 15.1% globally. For an investor, these are two "higher quality" sources of growth than pure retail because they typically have higher margins, better repeatability and often less sensitivity to short-term price cycles in grocery or general merchandise.

From a cash flow perspective, the company confirms that Walmart is not just a "defensive" story, but a high cash flow business. For the full fiscal year, the firm reported operating cash flow of $41.6 billion (YoY +5.1 billion) and free cash flow of $14.9 billion (YoY +2.3 billion). On the balance sheet, the company had cash of USD 10.7bn and total debt of USD 51.5bn. At the same time, the company has repurchased 85.0m shares for USD 8.1bn since the beginning of the year and announced a new buyback authorization of USD 30bn to replace the remainder of the previous program.

Segmentally, the quarter is "clean" and understandable. Walmart U.S. increased revenue to $129.2 billion (+4.6%) and operating income to $7.0 billion (+6.6%), with the company explicitly citing a combination of higher gross margin, better inventory performance and improving e-commerce economics. International grew faster in revenue, but with more volatility in profitability: revenue of USD35.9bn (+11.5%), +7.5% in constant currencies, and operating income of USD1.9bn (+36%), with some of the quarter-on-quarter momentum impacted by the timing of the big Flipkart event. Sam's Club had revenues of USD 23.8bn (+2.9%), comp sales excluding fuel +4.0% and e-commerce +23%, confirming that the membership model continues to grow steadily.

CEO commentary

John Furner comments on the results as evidence that Walmart is "leading" the change in retail towards speed, convenience and personalization. Significantly, management doesn't just talk about revenue growth, but repeatedly emphasizes growing operating profit faster than sales and improving the mix through e-commerce, advertising and membership. Between the lines, it's a clear message to investors: Walmart wants to be valued as a company that can combine defensive stability with higher-margin growth in digital, while guarding return on capital through dividends and buybacks.

Outlook

The Q1outlook calls for revenue growth of 3.5%-4.5% in constant currencies and operating profit growth of 4.0%-6.0% (also in constant currencies). Adjusted EPS is expected to be $0.63-0.65, with the company directly stating a comparable base for Q1 2025. In practice, this looks like a "cautious start to the year": growth continues, but Walmart doesn't want to overshoot profitability expectations in an environment where currencies, geopolitics, inflation and tariff policy can all play a role.

For the full year, Walmart expects constant currency sales growth of 3.5%-4.5% and adjusted operating profit growth of 6.0%-8.0%. Adjusted EPS is expected to be $2.75-2.85. The company also expects higher net interest expense of $200-300 million. USD 200 million, an effective tax rate of 23.5%-24.5% and a capex of about 3.5% of net sales.

Long-term results

For Walmart, the long-term story is that the company can grow even at its size while gradually improving earnings quality. Revenue has been growing at a steady pace in recent years: roughly $572.8 billion in 2022 to $611.3 billion in 2023, $648.1 billion in 2024, and $681.0 billion in 2025. Most recently, the company reports full fiscal year revenue of US$713.2 billion, confirming that growth is holding up even on a higher base. Gross profit is growing with sales, but more importantly, higher margin revenues are increasingly entering the mix: advertising, marketplace, fulfillment and membership.

Operating income shows that Walmart has been working with cost discipline and investment in digital in recent years so that it doesn't become "growth at any cost." In fiscal 2022-2025, operating income has ranged from c. $20.4bn (FY22) to c. $29.3bn (FY25), with the current year bringing an acceleration in adjusted operating income and Q4 profit growth significantly faster than revenue growth. EBITDA is also an important detail in the table, rising from c.USD30.1bn (FY22) to c.USD42.0bn (FY25), confirming that the company has solid operating leverage and can absorb investments in logistics and technology without breaking down cash generation.

Net income and EPS have clearly strengthened in recent years: basic EPS c.1.43 (FY22) → 1.92 (FY23) → 2.42 (FY24) → 2.87 (FY25), and the firm reports further cash flow growth in the current year as well as continued buybacks. In doing so, we see share count work as well: average share count dropped from ~8.376bn (FY22) to ~8.041bn (FY25) and further towards ~8.0bn in TTM.

News

Strategically, Walmart continues to move in two directions that reinforce each other. The first is an omni model(advanced AI systems) built on leveraging the store network as a logistical advantage for digital. You can see this in the results through the rapid growth of store-fulfilled pick-up and delivery and through digital adding hundreds of basis points to comp sales. The second direction is the monetization of traffic through advertising and marketplace. The advertising business has moved to "nearly $6.4bn" for the fiscal and is growing significantly faster than core retail, which is gradually improving the quality of the margin profile across the group.

The combination of membership and efficiency is also significant. Membership fee revenue is growing at double-digit rates and, for Sam's Club, is promoting stability and improved predictability. At the same time, Walmart is keeping inventory under control.

Shareholder structure

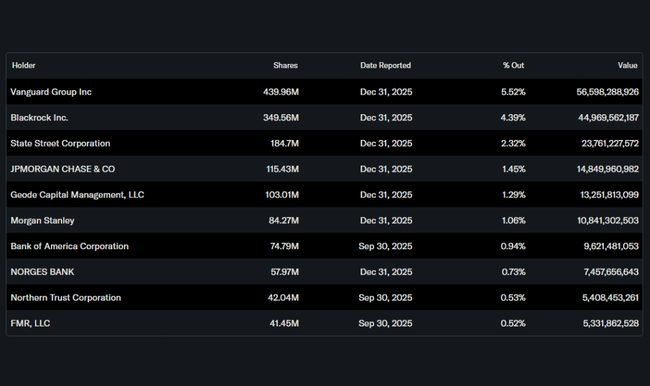

Walmart has a higher-than-average insiders share, which in practice is related to the long-term ownership of the founding family and the fact that the company has a stable controlling element. In addition, institutional investors are significant mainly in the free float: institutions hold around 38.85% of the shares.

The largest institutional holders include Vanguard (about 5.52%), BlackRock (about 4.39%), State Street (about 2.32%), and JPMorgan Chase (about 1.45%). This mix is typically supported by an emphasis on stable growth, disciplined buybacks, and predictable cash flow, as these are the factors that carry the most weight for long-term funds in "mega-cap" retail.