Realty Income delivered the kind of quarter its investors usually want: stable operations, high occupancy, and better rent terms when leases were renewed. Revenue reached $1.49 billion and net income attributable to shareholders was $0.32 per share. For a REIT, the more useful number is cash generation, and the company reported AFFO of $1.08 per share in Q4.

The bigger message is how the company is setting up 2026. Management is preparing to invest more and to bring in capital from more sources. Besides regular share issuance, Realty Income points to a new open-end fund and a partnership with a large long-term investor. The company’s 2026 outlook calls for AFFO of $4.38 to $4.42 per share, and it suggests that investment volume could be meaningfully higher than in 2025.

How was the last quarter?

In the fourth quarter, Realty Income $O increased total revenue to $1.4879 billion from $1.3403 billion a year earlier. Net income available to shareholders was $296.1 million, or $0.32 per share, compared with $199.6 million and $0.23 per share in the same period a year ago. However, from a "cash performance" perspective, AFFO's headline result was $1.08 per share, a level that is directly linked to the sustainability of the dividend.

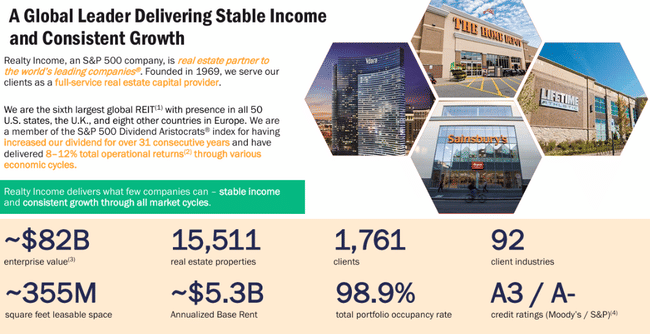

The operating quality of the portfolio is demonstrated by occupancy and the ability to renew contracts without losing rent. Portfolio occupancy reached 98.9%, and in reoccupying units, the company achieved that new annual rents were higher than the original ones: in the quarter, the "return on rent" came out to 104.9% (new rents of $88.30 million versus the previous $84.21 million on the same units). This is significant for an investor because it suggests that even in an environment of higher interest rates and more cautious tenants, the portfolio still has bargaining power.

On the investment side, the firm invested $2.4 billion in Q4 ($2.3 billion for its share) with an initial cash yield of 7.1%. At the same time, it continued to work with capital through its continuous share sale program: in the quarter, it settled 14 million shares from previously negotiated sales, raising gross proceeds of $817.8 million. The net debt to adjusted annual operating earnings before interest, taxes, depreciation and amortization (EBITDAre) ratio was 5.4 times, still a "mid" level for a REIT of this type, and combined with access to the capital markets, gives the company room to grow in 2026.

CEO commentary

Sumit Roy frames 2025 as "consistent returns and targeted actions" to amplify the firm's competitive advantages. Between the lines, the key takeaway is that management is consciously shifting the narrative from mere stability towards growth: it highlights the acceleration of investment in the fourth quarter and argues that the active pipeline for 2026 is strong enough for the company to talk about an initial investment volume of around $8 billion. At the same time, it backs the outlook with two "new sources of capital" - an open-ended fund in the US and a partnership with a major investor - which is expected to reduce reliance on a single source of funding and improve its ability to close deals at scale.

Outlook

Realty Income gives AFFO expectations of $4.38 to $4.42 per share for 2026. Management adds an interpretation that this is roughly 2.8% mid-range growth and approximately 9% total operating income (a combination of cash per share growth and dividend). That's a relatively conservative style of communication: the company isn't promising leapfrog improvement, but it's giving investors a clear framework for what a "normal" year should look like if tenants remain stable and the investment plan can be executed.

The second part of the outlook is the volume of investment. Management talks about the initial investment expectation for 2026 being approximately $8 billion, well above 2025 when the company invested $6.3 billion (for its share of $6.2 billion) at an initial cash yield of 7.3%. For investors, this means a simple thing: AFFO per share growth will largely depend on how effectively the firm combines new sources of capital with the quality of acquisitions, and how much the cost of financing is reflected in the results.

Long-term results

Over the long term, Realty Income is the type of firm where it's important to track two parallel lines: the growth in portfolio scale and whether that growth actually translates into more sustainable cash per share. Revenues have grown strongly in recent years: from $2.08 billion in 2021 to $3.34 billion in 2022, $4.08 billion in 2023 and $5.27 billion in 2024. In 2025, revenues have moved further to $5.75 billion, confirming that the firm is still in an expansion phase and can pick up new properties in volume.

Profitability is specific to REITs, however, as net income often "fizzes" due to revaluations, asset sales and one-time items. That's why Realty Income mainly tracks FFO and AFFO. For 2025, the firm reported FFO of $4.25 per share and AFFO of $4.28 per share, with AFFO itself down only slightly year-over-year from $4.19 to $4.28, which is consistent with the year being very much about funding growth and ensuring that portfolio growth doesn't dilute cash per share. From an investor's perspective, the important thing is that management still maintains a moderate growth outlook for 2026 and backs it up with an investment pipeline.

An important detail that is often missed is the handling of the share count. The data shows that the average number of shares has grown significantly in recent years as the company has financed expansion through issuance, among other things. That's why it's critical for investors to monitor whether acquisitions and hiring revenue can "beat" dilution and sustain AFFO per share growth. Q4 2025 has been steady in this regard: the company has been able to increase net income per share as well as maintain AFFO of $1.08 per share, while holding very high occupancy.

News / Strategic shift

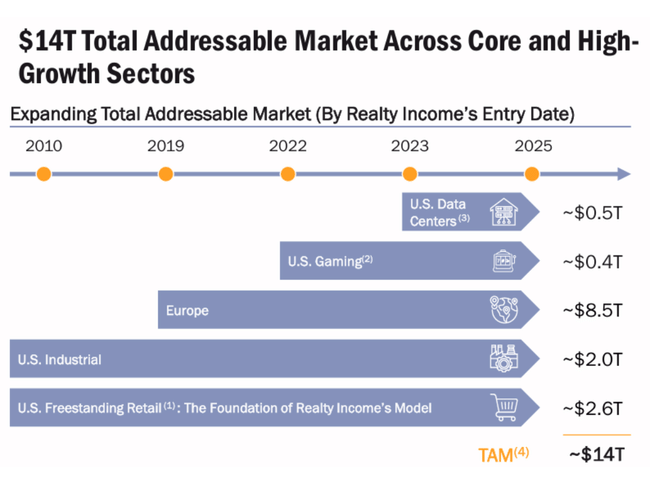

The most obvious strategic shift is the expansion of capital sources and geographic reach. The firm launched its first open-end fund focused on stable commercial real estate in the U.S. in 2025 and had raised $1.5 billion in investor commitments by the end of the year. It then announced a strategic partnership with GIC after year-end and a joint framework for "bespoke" projects with combined commitments of over $1.5 billion. These are steps that may increase the ability to do larger deals without the company having to "push" equity issuance to the same degree in every cycle.

In practical transactional news, the expansion into Mexico is also noteworthy: the commitment to buy out an industrial portfolio for $200 million in dollar-denominated long-term leases is Realty Income's first larger-scale entry into the country. And from a financing perspective, it is key that in January 2026 the company issued $862.5 million in convertible notes due in 2029, creating additional financial flexibility for refinancing and investment.

Shareholder structure

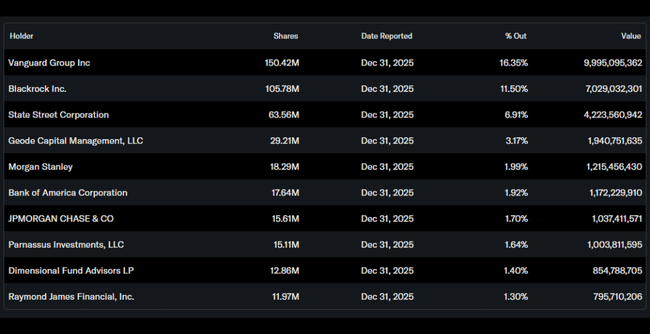

Realty Income is a distinctly institutional title: the institution holds roughly 80.9% of the stock and nearly 81.9% of the free float, while management's stake is approximately 1.24%. This typically means two things: first, high liquidity and a stable shareholder base, and second, sensitivity to interest rate movements, as large money managers often rebalance weightings in the real estate sector as bond yields change.

The largest holdings are dominated by the largest passive and broadly diversified fund managers: Vanguard holds roughly 16.35%, BlackRock 11.50%, State Street 6.91% and Geode 3.17%. For the firm, this typically reinforces the pressure for long-term dividend predictability and disciplined growth funding.

Analyst expectations

For Realty Income, analysts have often agreed in recent months that it is a stable "dividend" title, but there is limited room for significant repricing unless the interest rate environment changes or the company surprises with the pace of AFFO per share growth.