In fiscal Q3 2026, Oracle lifted revenue by 22% to 17.2 billion dollars and non‑GAAP earnings per share by 21% to 1.79 dollars, beating both its own guidance and Wall Street expectations. The engine is clearly cloud: combined IaaS and SaaS revenue jumped 44% to 8.9 billion dollars, with cloud infrastructure alone soaring 84%, while remaining performance obligations climbed to 553 billion dollars, highlighting a multi‑year backlog of contracted work rather than a one‑off AI spike.

For investors, this is the first time in more than 15 years that Oracle delivers organic total revenue and non‑GAAP EPS growth of 20% or more, just as it pours tens of billions annually into AI‑ready data centers and expands its cloud footprint. Oracle has flagged plans to raise 45 to 50 billion dollars in 2026 through a mix of debt and equity to fund this expansion, which raises the stakes on the AI cloud cycle. If demand for AI workloads stays strong for long enough, those heavy capex budgets and the higher leverage could translate into structurally higher profits rather than just a one‑off boom.

How was the last quarter?

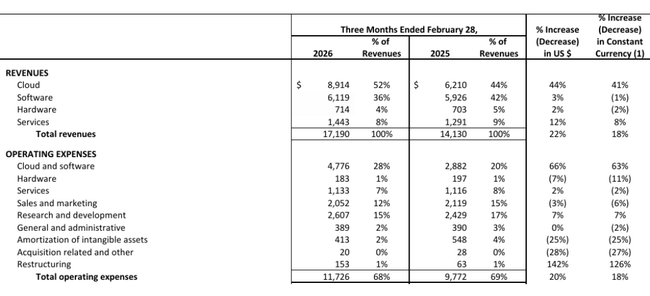

Total Oracle $ORCL revenue in fiscal Q3 2026 was $17.2 billion, up 22% in dollars and 18% in constant currencies. Cloud revenue(IaaS + SaaS) grew 44% to $8.9 billion, while more traditional non-cloud software revenue grew just 3% to $6.1 billion. This confirms that Oracle is becoming primarily a cloud company - growth is being driven by new cloud services while the legacy licensing model stagnates.

Within the cloud, cloud infrastructure (IaaS) was the main driver with $4.9 billion in revenue and 84% year-over-year growth, while cloud applications (SaaS) grew 13% to $4.0 billion. Oracle Cloud Database (IaaS) revenue grew 35%, while multicloud database revenue jumped 531%, reflecting the success of strategies where Oracle databases also run on the infrastructure of other large providers. This lowers the barrier for clients who don't want to leave their existing cloud partners, while strengthening Oracle's role in the era of multicloud environments.

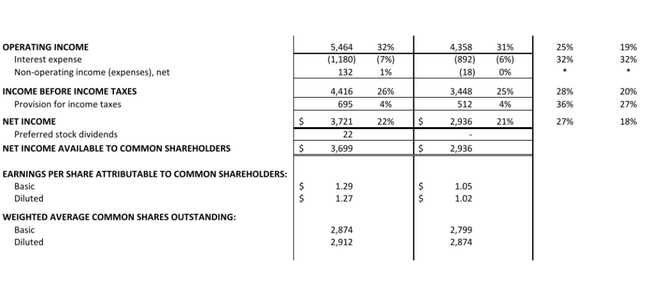

In the financials, this translated into GAAP operating profit of $5.5 billion and non-GAAP operating profit of $7.4 billion, up 19% in dollar terms. GAAP net income was $3.7 billion and adjusted net income was $5.2 billion, up 23% year-over-year. GAAP earnings per share rose to $1.27 (+24%), adjusted earnings per share to $1.79 (+21%), and the company points out that this is the first quarter in more than 15 years where organic revenue and adjusted EPS have both grown 20% or more - so it's not just an effect of acquisitions, but "organic" cloud growth.

Importantly, from a balance sheet perspective, short-term deferred revenue was $9.9 billion and operating cash flow for the last twelve months was $23.5 billion, up 13%. But the item that stands out the most is Remaining Performance Obligations (RPO) at $553 billion, up 325% from last year and up $29 billion from the prior quarter. The vast majority of this jump comes from large AI contracts: some clients pay Oracle up front so the company can buy graphics chips, others supply the hardware themselves - so Oracle is getting a huge future volume of work with relatively less equity, a very shareholder-friendly model.

Management commentary

Oracle management calls the results an "exceptional quarter" that exceeded expectations and confirmed the acceleration of cloud and profit growth. Commenting on Q3, it notes that this is the first quarter in more than 15 years that organic revenue and adjusted earnings per share grew 20 percent or more, and that cloud revenue, total revenue and adjusted EPS were at or above the high end of published guidance. The tone is clearly confident - Oracle is positioning itself as one of the key players in cloud for AI.

The company also describes that demand for cloud capacity to train and deploy AI models is growing faster than supply, and that some of its largest customers have significantly strengthened their financial positions, reducing credit risk and increasing the likelihood that long-term contracts will be fully utilized. An interesting detail is the restructuring of its own development teams: by generating code using AI, Oracle is regrouping product teams into smaller, more efficient units and claims to be able to "write more software with fewer people". This is a signal to investors that AI is not just a product towards clients, but also a tool to increase productivity and margins internally.

Outlook

For the fourth quarter of fiscal year 2026, Oracle expects total revenue growth of 18-20% in constant currencies and 19-21% in dollars. Cloud revenue is expected to grow even faster, by 44-48% in constant currencies and 46-50% in dollars, confirming that management anticipates a continued strong demand cycle in the cloud for AI. Adjusted earnings per share are expected to increase 15-17% to $1.92-1.96 in constant currencies and $1.96-2.00 in dollars.

At the full fiscal year 2026 level, Oracle affirms guidance of $67 billion in revenue and $50 billion in capital expenditures. For fiscal year 2027, the company is raising the outlook to $90 billion in revenue, with the company itself stating that demand for cloud capacity for AI will allow it to "comfortably" meet or exceed that growth. That outlook is ambitious - it implies double-digit revenue growth even after the big jump in 2026, and relies on AI mega-contracts to translate into actual capacity utilization and cash flow over the next few years.

The company also reiterates its funding plan: in February, it announced its intention to raise up to $50 billion in debt and equity, and has already raised $30 billion in a matter of days through investment-grade bonds and convertible preferred stock; it has not yet used some of the funding through a stock market sale. Oracle adds that it has no plans to issue additional debt outside of this program in 2026 - this suggests to investors that it has a clear framework in which to fund data center expansion while trying to keep debt under control.

Long-term results

For the year ending May 31, 2025, Oracle's revenue was $57.40 billion, up 8.4% from $52.96 billion in 2024 and $49.95 billion in 2023. In the previous years, the company grew 6.0% (2024) and 17.7% (2023) from the 2022 level of $42.44 billion, so from a four-year perspective, the revenue trend is steadily upward, although the rate of growth fluctuates based on the cloud investment cycle and currency movements. Thus, the high pace in fiscal 2026 (22% in Q3) marks a clear acceleration against the average of recent years.

Gross profit in 2025 was $55.09 billion, compared to $37.82 billion in 2024, $36.39 billion in 2023 and $33.56 billion in 2022. Notable is the dramatic reduction in the "cost of revenue" line item in 2025 to $2.31 billion from $15.14 billion in 2024 and $13.56 billion in 2023, which in the numbers looks like a massive improvement in gross margin. Part of this effect is related to accounting cost capture (reclassifying items to operating expenses) and service mix, so it's more of a trend to watch: Oracle has been moving the business into high-margin software and cloud for a long time, which improves gross margins structurally, not on a one-off basis.

Operating expenses rose to $37.41 billion in 2025 from $22.47 billion in 2024, while they hovered around $22-23 billion in 2022 and 2023. This jump reflects both higher investment in the development and sale of cloud services, costs related to infrastructure expansion, and likely some one-time items (e.g., acquisitions, restructuring). Still, operating profit rose to $17.68 billion (+15.1%), from $15.35 billion in 2024, $13.09 billion in 2023, and $10.93 billion in 2022; thus, operating leverage is working - revenue and gross profit are growing faster than operating expenses.

Pre-tax profit in 2025 was $14.16 billion, up from $11.74 billion in 2024 and $9.13 billion in 2023; net income rose to $12.44 billion, up 18.9% from $10.47 billion in 2024 and 46% from $8.50 billion in 2023. Earnings per share increased from $2.49 in 2022 to $3.15 in 2023, $3.81 in 2024 and $4.46 in 2025; diluted earnings per share grew similarly from $2.41 to $3.07, $3.71 and $4.34. The number of shares grew only very modestly (roughly 2.70-2.87 billion diluted shares), so EPS growth actually reflects profitability growth, not just financial engineering.

EBIT reached $17.74 billion and EBITDA reached $23.91 billion in 2025, with both metrics growing steadily from 2022 (EBIT 10.40 billion, EBITDA 13.53 billion) through 2023 (EBIT 12.63 billion, EBITDA 18.74 billion) and 2024 (EBIT 15.26 billion, EBITDA 21.39 billion). This shows that Oracle is gradually increasing its operating leverage: as the built infrastructure and software scales to higher volumes, margins increase and further revenue growth translates strongly into profitability. In the context of today's massive investment cycle in AI data centers, it is key that the company has several years of consistent EBIT and EBITDA growth - investors see that the ability to generate profits from new capacity has been proven in the past.

News

Strategically, Oracle is betting on a combination of cloud for AI and multicloud database services. The huge increase in RPO to $553 billion is the result of multi-year contracts with large customers that either pre-fund the hardware or supply it themselves - giving Oracle a long-term committed business without having to carry the full investment burden. The company is also massively ramping up capital spending to $50 billion in 2026, a leap from previous plans and reflecting the global expansion of data centers.

The financing method is also important: Oracle plans to raise up to $50 billion through a combination of debt, preferred stock and market sales, and has already secured $30 billion through bonds and mandatorily convertible preferred stock. This secures capital for expansion without dramatically impairing immediate liquidity, but it also raises debt and future dilution, the "price" for accelerating AI cloud market adoption.

Oracle is also emphasizing the use of AI code generation in its own development: it is regrouping teams, using AI for programming, and claims it can create new cloud applications for more industries faster at lower cost as a result. This is a strategic shift to be more competitive against Microsoft, Amazon and other players in the long term: not just providing infrastructure, but a richer layer of applications (ERP, industry modules, industry solutions) at higher margins.

Shareholding structure

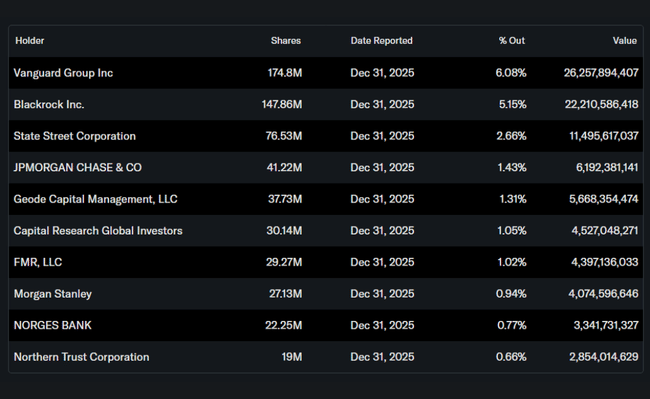

Around 40-41% of Oracle's shares are held by insiders (including founders and management), around 44% by institutions and around 14% by retail and other investors. The largest institutional owners include Vanguard Group (about 6% of shares, about 175 million shares), BlackRock (about 5%, about 148 million shares), State Street (over 2.6%, about 76 million shares), and JPMorgan to the tune of about 1.4%. This structure implies a combination of a high insider share - which promotes stability and a long-term horizon - and a broad institutional base dominated by large index and passive funds, so that the stock is relatively well "anchored" but responsive to changes in the large-cap technology sector and indices.

Oracle also pays a stable dividend: the board has approved a quarterly dividend of $0.50 per share, payable on April 24, 2026 to investors enrolled on April 9, 2026. Combined with earnings growth and the use of debt instead of net dilution, this gives shareholders a mix of growth and yield profile - but investors should watch how the ratio of free cash flow to dividends and interest evolves as debt grows.

Analyst expectations

Based on available commentary and quick market reactions, Oracle beat consensus expectations in Q3 2026, delivering revenue of $17.2 billion versus approximately $16.9 billion, and adjusted EPS of $1.79, above the midpoint of estimates. Analysts generally emphasize two main theses: first, that Oracle's high RPO and fast-growing AI contracts make it one of the major "pure bets" on AI infrastructure; second, that the raised revenue outlook to $90 billion in fiscal 2027 is ambitious but realistic if the company can get its new data centers up and running on time.