In 2025, Volkswagen kept group sales revenue broadly flat at about 322 billion euros, but operating profit dropped to 8.9 billion euros, more than halving versus the previous year. The hit came mainly from U.S. import tariffs, the costly overhaul of Porsche’s product strategy, weaker pricing and currencies, while underlying operations before these special charges and tariffs would have earned a far higher 17.7 billion euros.

Under the surface, the balance sheet and cash generation look much healthier than the headline margin of 2.8% suggests: the Automotive Division generated around 6.4 billion euros of net cash flow and net liquidity rose to more than 34 billion euros, giving the group financial room to fund its transition. For equity investors, the medium‑term story now stojí hlavně na programech zvyšování efektivity, restrukturalizaci portfolia a úspěchu levnějších elektromobilů, přičemž vedení na rok 2026 počítá jen s mírným růstem tržeb 0–3% a provozní marží mezi 4,0% a 5,5%.

What was 2025 like?

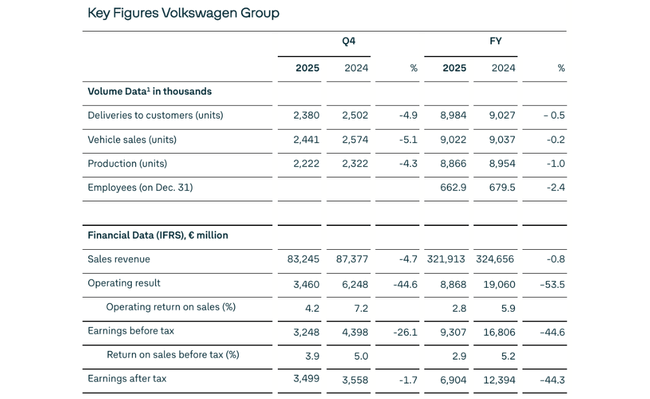

The $VOW3.DE group achieved sales of €321.9 billion in 2025, virtually on par with 2024(€324.7 billion), and sold around 9.0 million vehicles. Regionally, Europe(+5%) and South America(+10%) grew, while North America(-12%) and China(-6%) declined due to challenging market conditions, tariffs and competition. Orders in Europe were up ~13%, with battery electric vehicles (BEVs) growing ~55% and accounting for ~22% of the order book.

Operating profit for the full year was €8.9bn, equivalent to a margin of 2.8%, versus €19.1bn and a margin of around 5.9% in 2024. Management said the decline was due to a combination of:

US tariffs

significant costs of changing Porsche's product strategy

unfavourable exchange rate and price/mix effects

Ongoing cost-saving programmes were positive but failed to fully offset external pressures.

Adjusted operating profit (excluding restructuring and Porsche costs but including US tariffs) was €14.8 billion, a margin of 4.6%. Adjusting for the impact of US tariffs, this also yields an operating profit of €17.7bn and a margin of 5.5% - this shows that the 'underlying' performance is better than the GAAP net result suggests, but the company is very sensitive to political decisions and premium brands.

The automotive division generated €6.4bn of net cash flow, up 24% on 2024(€5.2bn), mainly due to a decline in working capital and tighter investment discipline. The Automotive Division's net liquidity remained very solid at the end of the year at €34.5 billion, giving Volkswagen room to finance its transformation (electromobility, software, batteries) while paying a dividend.

Management commentary

CEO Oliver Blume stressed that the Group "kept the course" in 2025 despite geopolitical tensions and growing headwinds, and recalled the launch of 30 new models and visible progress in restructuring. Management talks of entering the "next phase of transformation": adapting the business model to new conditions, expanding the regional footprint (especially China and the US), consistently reducing costs and delivering superior products.

Specifically, Blume mentions that in 2026, the Group wants to launch affordable electric mobility with premium technology, launch the largest product offensive in history in China, and achieve milestones in batteries, software and autonomous driving. The tone is realistically positive: it acknowledges that the environment is "fundamentally different", but also reassures investors that restructuring programmes are bearing fruit and that the group has "robust substance" - that is, a portfolio of brands and technologies to fall back on.

CFO and COO Arno Antlitz says bluntly that an adjusted operating margin of 4.6% is insufficient in the long term if Volkswagen is to remain competitive with internal combustion cars, invest in attractive electric vehicles and software, and expand its US presence. Thus, it clearly sets a priority: aggressively cutting costs, exploiting synergies and reducing complexity across the group to bring margins back to higher levels. The CFO's tone is thus distinctly disciplined, emphasizing profitability over growth at any cost.

Outlook 2026

For 2026, the Volkswagen Group expects revenue growth in the range of 0% to +3% compared to 2025, i.e. rather flat to moderate growth in an environment of high competition and geopolitical risks. The operating margin is expected to be between 4.0% and 5.5%, slightly above the 2025 level after adjustments, but still below a comfortable level for a capital-intensive automaker.

In the automotive division, the company is targeting an investment ratio (capex to sales) of 11-12%, a high but understandable level in the context of the shift to electric mobility, batteries and software. Net cash flow for 2026 is expected to be €3-6bn, potentially lower than 2025 due to, among other things, higher investments - but at the same time, management plans to keep the automotive division's net liquidity between €32-34bn, which would still provide a robust financial cushion.

Volkswagen notes that the main risks to the outlook stem from macro factors (weaker growth, inflation), possible new or changed tariffs and trade restrictions, geopolitical tensions, increasing competition (especially from Chinese brands and Tesla), volatility in raw material and energy prices, and tightening emissions regulations. The baseline scenario assumes that current tariffs on international trade remain unchanged - so any new barriers could easily worsen the outlook.

Long-term results

Over the period 2021-2024, Group revenues grow from €250.2 billion (2021) to €279.1 billion (2022), €322.3 billion (2023) and €324.7 billion (2024). This implies double-digit growth between 2021 and 2023 and a stabilisation in 2024 (+0.74%), when volume and price growth offset competitive and mix pressures. Gross margins increased from €47.1bn in 2021 to €52.6bn in 2022 and €62.0bn in 2023 before declining slightly to €61.0bn in 2024 - gross margins were therefore relatively stable, reflecting a balanced mix of mass and premium brands.

Operating costs rose from €28.9 billion in 2021 to €36.3 billion in 2022, before falling slightly to €34.7 billion in 2023 and rising again to €36.6 billion in 2024. Operating profit was €18.19bn in 2021, €16.24bn in 2022, €27.32bn in 2023 (a strong year thanks to pricing, mix and premium brands) and €24.39bn in 2024. This shows that Volkswagen is highly cyclical: it can generate significantly higher margins in good years but is very sensitive to price, volume and external shocks (tariffs, raw materials, exchange rate).

Net profit hovered around €15.4-16.5bn in 2021-2024 before falling to €11.35bn in 2024, a 31% drop from 2023. Earnings per share fell from €31.94 in 2023 to €21.39 in 2024, while the average number of shares remains virtually unchanged at ~501m, meaning that the drop in EPS is due to profit decline, not dilution.

EBIT was between €19.42bn (2021) and €23.08bn (2023), falling to €18.29bn in 2024; EBITDA was relatively stable around €46.7-50.0bn, with a slight decline from €49.84bn in 2023 to €48.22bn in 2024. This shows that at the EBITDA level the Group still has solid earnings power, but costs (depreciation, restructuring, development) and external shocks are "stealing" a large part of the profit at the lower levels of the income statement. In the long term, it is crucial that ongoing cost-saving programmes and a shift towards higher value-added (software, premium brands, services) translate stable EBITDA into higher net profit and return on capital.

Shareholding structure

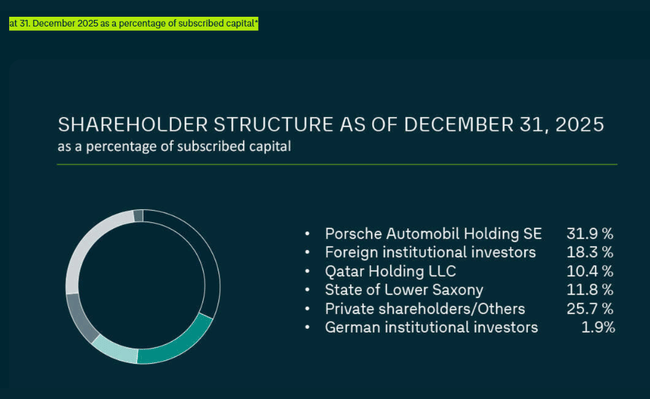

As of December 31, 2025, Volkswagen had 295,089,818 ordinary shares and 206,205,445 preferred shares outstanding, for a total of approximately 501 million shares. The shareholder structure according to the proportion of the subscribed capital is as follows.

Porsche Automobil Holding SE: 31.9%

Foreign institutional investors: 18.3%

Qatar Holding LLC: 10.4%

Federal State of Lower Saxony: 11.8%

Private shareholders / others: 25.7%

German institutional investors: 1.9%.

This structure means that the Group is firmly controlled by the Porsche/Piëch family holding company and the Land of Lower Saxony, while foreign institutions play a significant but not dominant role. For the investor, this means high management stability and a long-term horizon, but also less flexibility in the event of radical strategic changes or pressure to maximise profits in the short term. The split between common and preferred shares also plays a role for voting rights and dividend flow.

Dividend

The Executive Board and the Supervisory Board plan to propose a dividend of €5.26 per preference share and €5.20 per ordinary share for 2025 at the AGM, down 17% on the previous year. The payout ratio remains in line with the policy of "at least 30%" of earnings; management also emphasizes that the non-cash goodwill impairment charge in the Porsche segment has not been included in the dividend calculation so that the one-off accounting item does not artificially depress the dividend. For investors, this means that Volkswagen maintains a solid dividend yield even in a worse year, but signals caution and the need for transformation capital.