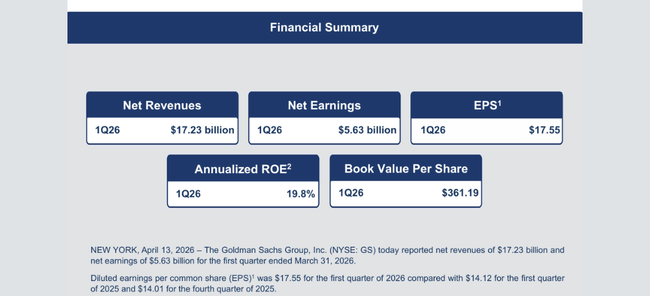

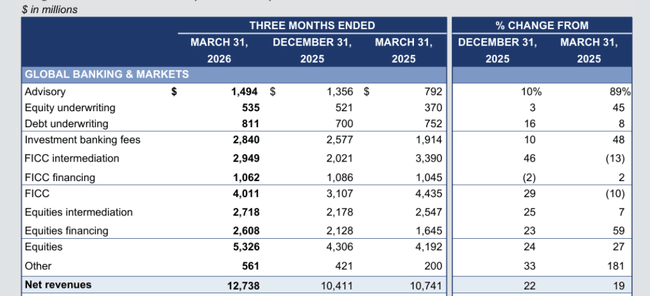

Goldman didn’t just put up a “good quarter” to start 2026 – it printed the kind of profitability regulators usually try to beat out of big banks. First‑quarter earnings per share came in at 17.55 dollars with an annualised return on common equity of 19.8%, a level that pushes Goldman much closer to high‑quality asset managers and alternative‑investment platforms than to the average balance‑sheet‑heavy lender. Revenues grew strongly year‑on‑year, driven by a broad rebound in Global Banking & Markets, fee income from advisory and underwriting, and still‑solid trading, confirming that the core engine which investors wanted back after the consumer‑banking detour is firmly in the driver’s seat again.

What matters is how the bank got there. The quarter reads less like a one‑off windfall and more like the payoff from a multi‑year course correction: shrinking or exiting low‑return retail experiments, re‑weighting toward advisory franchises, financing and wealth management, and pushing harder on capital discipline and buybacks. With the stock already up sharply over the past year and the share of earnings coming from fee‑rich, balance‑sheet‑light activities rising, Q1 2026 works as a proof‑of‑concept that the “back to our knitting” strategy can support a near‑20% return on equity even in a world of higher capital requirements – a bar most universal banks still only talk about in slide decks.

How Q1 2026 turned out

Revenue and profit

Net revenues:

Approximately USD 17.2 billion

Approximately USD 15.1 billion in Q1 a year ago

year-on-year growth of around 14%

For a bank that is already very large, double-digit revenue growth in one quarter is clearly a positive signal. At the same time, it is well above the market consensus, which means that Goldman $GS was able to take advantage of the current market situation better than the market expected.

Net Earnings:

Q1 2026 approximately USD 5.6 billion

Q1 2025 approximately USD 4.6 billion

Year-on-year, net income will thus increase by around USD 1 billion, or around 20-25%. This is the main number that "pulls" the story of the quarter - the bank was able to translate much of the revenue growth into profit growth, not just "burn" it in costs.

Earnings per share (EPS):

Q1 2026: $17.55

Q1 2025: approximately USD 14.1

EPS growth of about $3.4 per share corresponds to a year-over-year increase of about 25%. That's a very solid pace for a bank of this size and confirmation that this is not just a cosmetic improvement.

Return on equity

Return on Equity (ROE):

Q1 2026 around 19.8%

a year ago more in the region of 14-15%

A jump close to 20% is crucial - most large US banks typically hover somewhere between 10% and 15%. Nearly 20% means Goldman can earn significantly more per unit of capital than the sector average.

Return on tangible equity (ROTE):

Q1 2026 around 21%. This number strips capital of goodwill and other intangible assets, so it is closer to how efficiently the bank works with "real" capital. Over 20% is a very high level in the banking world, which usually justifies an above-average valuation if it is sustainable.

How management commented on the results

"The geopolitical environment remains very complex - so disciplined risk management must remain at the core of our operations," Goldman Sachs CEO David Solomon said in a statement.

Management built on two main theses in its commentary.

First, that this is an "earned" number, not just a fluke. Management notes that the bank has been making tough moves in recent years - exiting retail banking, cutting back on loss-making projects, realigning its capital allocation. Q1 2026 shows that the puzzle is coming together nicely: capital is concentrated where Goldman has traditionally had a strong brand, people and processes.

Second, that they recognize the cyclicality of the business despite a strong quarter. Market activity, M&A volumes or new issue creation are sensitive to the macro economy and investor sentiment. Management is therefore stressing that it wants to continue to strengthen the more stable pillars of returns - mainly wealth management, investment products and long-term mandates from large clients.

At the core, then, is the message:

The numbers are excellent.

They are not just a fluke, but a result of the changes we have made.

Still, we're not going to pretend it's going to be like this every quarter, and we're going to continue to build a more stable mix of returns.

The long-term picture

When we step back from one quarter and look at the last few years, a clear turnaround is emerging. After the weaker years of 2022-2023, when results were pressured by weaker market activity and retail losses, both annual revenue and net income have gradually started to pick up.

Revenues have been roughly in the range of USD 46-50bn per annum in recent years, with 2025 bringing further improvement thanks to a recovery in investment banking and trading. Net profit in 2025 was somewhere between USD 15-16 billion, a marked improvement on the weaker years before.

Return on equity has gradually moved from levels around 10-12% closer to the bank's previously communicated target of somewhere in the 15-17% range. Q1 2026 builds on this and adds another step: ROE of nearly 20% and EPS of $17.55 are above the average of recent years.

Investors need to ask themselves two questions:

How much of this performance is due to "good markets"? If activity in MA, issues or trading weakens next year, the numbers will go down.

What is the structural change? If a lower cost base, a better mix of business and a greater emphasis on asset management is a permanent change, the average year in the future should look better than the average year in the past even after the current boom is subtracted.

Q1 2026 alone doesn't address this issue, but it makes a good case for saying that Goldman has the potential to steadily hold near the top end of the sector as long as regulation and the environment don't throw it a big pitchfork.

Shareholders

Goldman Sachs is a typical "institutional" title.

Most of its shares are held by large funds - index funds, actively managed funds, pension and insurance portfolios.

The largest holdings include fund groups such as Vanguard, BlackRock and State Street, which together own a significant portion of the free float.

Insider holdings (the share of management and directors), on the other hand, are relatively small, which is common among similar firms.

Practical implications for the share price:

the move after earnings is not about "someone big" selling or buying

but how dozens and hundreds of funds adjust their models

increase their estimates of long-term EPS and ROE → more willing to pay more for the stock

will see Q1 as just the top of the cycle → will be more likely to hedge profits and put the brakes on further price appreciation

Therefore, even after a very good quarter, the market reaction may be muted if investors start to fear that it won't get better in the short term.

News and strategic moves

Q1 2026 not only gives good numbers, but also fits in with a couple of important moves the bank has been making recently:

Completing the retreat from retail and consumer lending - Retail banking projects that have historically generated losses and complicated the balance sheet have either been sold or muted. This has freed up capital and management for key areas.

Focus on core investment banking and trading - Goldman is returning to what it has been doing for decades - advisory, issuance business, equity, bond and derivatives trading. In an environment where capital markets are waking up, it is taking full advantage of this.

Building a more stable pillar in wealth management - Wealth management and investment products (funds, alternatives) are a priority. The Bank wants a greater proportion of future revenues to come from regular fees, not just "hit and run" income from large transactions.

Capital policy - Goldman combines dividend with share buybacks. In a high profitability environment, this helps earnings per share growth, but at the same time the bank needs to hold enough capital for regulatory testing and stress scenarios.

Strengthening its position in the mergers and acquisitions market - Goldman is one of the main advisors in a period when larger deals are starting up again after a hiatus. This is important not only for short-term fees, but also for reputation and future assignments - those who service large deals now are more likely to be called upon next time.