3M’s first quarter of 2026 neatly captures the split between how the business is running and how the legacy legal mess still hits the P&L. Net sales inched up 1.3% year‑on‑year to 6.0 billion dollars, with organic sales actually down about 1.2–1.4%, but GAAP operating margin improved to 23.2% and adjusted operating margin to 23.8%, roughly 230 and 30 basis points higher than a year ago as pricing and cost cuts flowed through. On an adjusted basis, EPS rose 14% to 2.14 dollars, comfortably ahead of expectations and consistent with a company that has largely stabilised after spinning off its health‑care business.

The headline GAAP numbers look far less flattering. GAAP EPS fell 40% to 1.23 dollars per share, with management again flagging litigation and other one‑offs tied to PFAS contamination and combat earplug settlements as the main drag. Those legal outflows have already cost 3M tens of billions of dollars in recent years and are set to continue weighing on cash flow into the 2030s, which is why full‑year 2026 guidance was reiterated without much top‑line ambition: low‑single‑digit sales growth, high‑teens GAAP margin and mid‑20s adjusted margin. For investors, Q1 underlines the core dilemma: operationally, 3M is starting to look more like its old self on margin; on a reported basis, the stock is still chained to a legal bill that makes the gap between GAAP and “clean” earnings too big to ignore.

Q1 2026 results

Revenues and segments

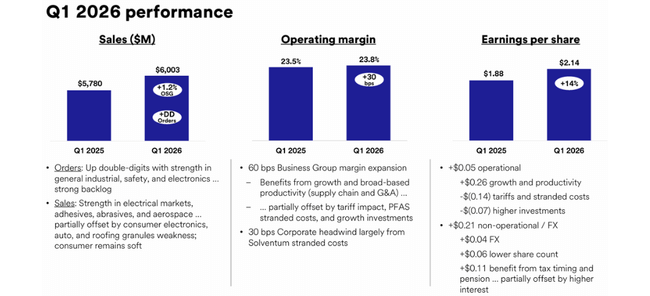

For Q1 2026, 3M's GAAP revenue was $MMM.0 billion, up 1.3% year-over-year. On an adjusted basis, it's the same number, with organic growth of 1.2%. From the perspective of a cyclical industry giant, this is more of a "stagnation with a slight plus" than a return to double-digit growth.

According to the presentation, the segments were mixed:

Safety & Industrial delivered organic growth of around 3% and overall sales were up around 6-7%, which was one of the main drivers.

Transportation & Electronics was slightly negative organically (around -0.3%), but overall sales grew slightly due to currencies and mix.

TheConsumer segment was down around 1-1.5% organically, but total sales were up slightly due to pricing and currencies.

Regionally, China was the main performer, with sales up around 8-9%, while the Americas saw a decline of around 1-2%. This shows well that 3M's business is still very sensitive to the local industry cycle and consumer demand.

Margins and profitability

The strength of the quarter is the improvement in margins. GAAP operating margin rose to 23.2%, up 230 basis points from a year ago. Adjusted operating margin moved to 23.8%, up 30 basis points year-over-year. Thus, management can rightly claim in the presentation that the "value creation framework" is gradually starting to work at the profitability level.

At the net profit level, the picture is more complex. GAAP EPS fell to $1.23, down about 40% from last year and well below consensus of about $1.97. This is due to a combination of higher non-operating expenses and the revaluation of the stake in the spun-off healthcare company Solventum, which translates into "other expense" and pulls down GAAP net income.

In contrast, adjusted EPS of $2.14 implies 14% year-over-year growth and beating the analyst estimate of around $1.97-2.02. So if you "peel away" the impact of Solventum and other one-time items, Q1 is surprisingly solid in terms of net income - but the market has to decide how much it's willing to trust these adjusted numbers.

Cash flow

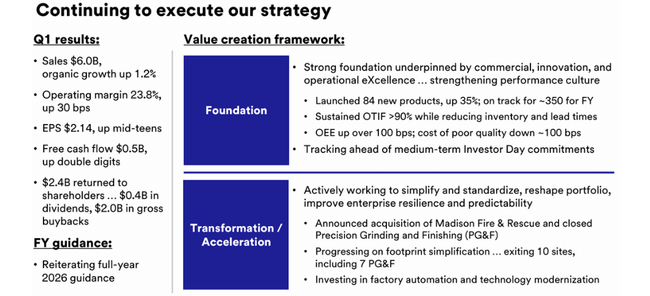

On the cash front, things are looking more sober. Q1 operating cash flow was $0.6 billion and adjusted free cash flow was $0.5 billion. It's not disappointing, but with the size of the company and the volume of legal liabilities, it's not even a number where an investor would think the problem is definitively solved.

What the CEO says and what the tone of management is

The same themes are repeated in the presentation and the press release. Chairman and CEO William Brown talks about a "value creation framework" to transform 3M into a stronger and more predictable enterprise.

Brown emphasizes three main points in his comments:

An emphasis on fundamentals and execution - better cost management, standardization of processes, and simplification of manufacturing and organizational structure.

Portfolio transformation - reducing less profitable or problematic parts, concentrating capital in segments with higher returns and better margins.

Long-term goals - a structure to enable "structurally higher growth" and "stronger margin performance", i.e. gradually moving 3M away from a period defined by litigation and restructuring.

At the same time, Brown says the company has had a "good start to the year" and that despite the volatile environment, management remains confident in achieving its 2026 target, both in terms of revenue growth and profitability. So the tone is cautiously optimistic: no big marketing slogans, but an emphasis on discipline and execution.

Outlook for 2026

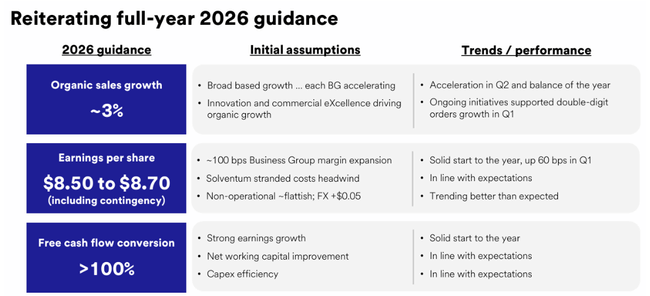

3M confirms its full-year outlook after Q1 2026. It expects approx:

3% growth in adjusted sales in 2026

Adjusted operating margin higher by approximately 70-80 basis points

adjusted EPS in the range of $8.50-8.70 per share, which is roughly in line with market expectations.

In addition, the presentation highlights several newer strategic moves and targets:

Aiming to launch around 350 new products in 2026 to support organic growth and a better mix with higher margins

the company continues its transformation - consolidating production, reducing complexity and thereby freeing up some capital and operating costs

3M wants to remain a large payer of cash to shareholders, but also declares that some of the free cash will be used to invest in growth and strengthen the balance sheet.

Long-term performance

Historically, 3M has been synonymous with steady growth and high margins. However, recent years have brought a combination of stagnant sales and legal issues, which has taken a toll on GAAP numbers as well as valuation and sentiment around the stock.

Analyst reports show that in previous years, sales have averaged declining or stagnant in the low single-digit percentages per year rather than growing. Meanwhile, profitability remained relatively solid on an adjusted basis, but GAAP margins and EPS were roiled by provisions and one-time costs.

Today's Q1 2026 fits the "slowly stabilizing" 3M picture:

Revenues no longer declining, but only growing 1-2%

margins are gradually improving

Adjusted EPS is growing, while GAAP EPS is still under pressure

Not very attractive for an investor looking for a growth story. But for someone looking for steady cash flow, a high dividend, and willing to live with a legal history and slower growth, this could be an interesting value/dividend bet.

Shareholders, dividend and capital policy

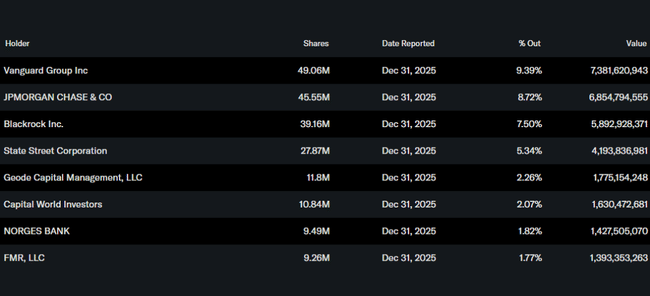

3M is a typical institutional title today. According to ownership summaries, large asset managers like Vanguard and BlackRock hold key positions, each with a few percent stake, supplemented by other funds and ETFs. Insiders own relatively little, which is standard for such a large, established firm.

The dividend remains a key part of the investment story. 3M recently approved a quarterly dividend of $0.78 per share, an increase of roughly 7% year-over-year. At the current share price, the dividend yield is in the higher units of percent, well above the index average.

In Q1 2026, 3M returned approximately $2.4 billion to shareholders through a combination of dividends and share repurchases. That's a strong signal toward shareholders, but it also opens up the debate about whether some of those funds should go more aggressively toward deleveraging and further strengthening the balance sheet until the legal past is definitively closed.

What does this imply for the investor

Q1 2026 and the presentation on the results confirm that 3M today is mainly a stabilization and dividend story, not a growth story:

Revenue only growing in units of percentages

margins are improving and adjusted EPS is rising

GAAP numbers are still weighed down by the past

the dividend is high and the company is actively returning cash to shareholders

If we're looking for momentum, double-digit organic growth and "clean" numbers without legal noise, 3M still doesn't offer it after Q1 2026. But if we're looking for a large, global industrial company with decent margins, a conservative outlook, a high dividend yield and gradual normalization after a series of tough years, then Q1 and the CEO's comments rather confirm that the story is moving in the right direction - just slowly.