Intel’s first quarter of 2026 is the first one in years where the story of a turnaround is backed by the numbers across the board. Revenue climbed about 7% year on year to 13.6 billion dollars, coming in roughly 1.4 billion above the company’s own conservative January outlook, while non‑GAAP EPS reached 0.29 dollars versus expectations close to breakeven. After a long stretch of falling sales, margin pressure and restructuring charges, this is the first clean quarter where both the top line and profitability move clearly in the right direction instead of just “getting less bad”.

The market reacted immediately. Before earnings, Intel’s shares were trading roughly in the high‑60s; after the report and much stronger‑than‑expected guidance for Q2 (revenue of 13.8–14.8 billion dollars and non‑GAAP EPS around 0.20), the stock ripped into the low‑80s in after‑hours and early trading, a move of close to 20% and a new multi‑decade high for a company that traded under 18 dollars less than a year ago.

Q1 2026 results

Revenue, Margin and Profit

In Q1 2026, Intel's revenue was $13.6 billion, up seven percent year-over-year from $12.7 billion in Q1 2025. More importantly, revenue was roughly $1.4 billion above the midpoint of its own outlook, which called for only $11.7 billion to $12.7 billion for Q1.

GAAP gross margin improved to 39.4 percent from 36.9 percent, and non-GAAP gross margin rose to 41 percent from 39.2 percent. This means that Intel $INTC is not only growing in revenue, but is starting to take back some of the margins it has lost dramatically over the past two years.

On a GAAP basis, operating margin is still deep in negative territory at minus 23.1 percent versus minus 2.4 percent last year. This is due to large write-downs, restructuring costs and effects around the Altera separation. On an adjusted basis, however, the picture looks different. Non-GAAP operating margin is 12.3 percent, more than double last year's 5.4 percent.

On net:

GAAP net loss is $3.7 billion, worse than last year's loss of $0.8 billion, and equivalent to a loss of $0.73 per share.

Non-GAAP net income is $1.5 billion and non-GAAP earnings per share are $0.29, compared to $0.6 billion and $0.13 last year.

Thus, the company more than doubled earnings per share, according to its own adjusted numbers, while sales are up just seven percent. Meanwhile, the market was expecting Q1 non-GAAP EPS to be more around zero after the fourth quarter, as Intel itself was expecting $0.00. So when $0.29 comes in, it's a pleasant surprise for analysts and investors.

In Q1 2026, Intel generated roughly $1.1 billion in cash from operations. That's a low number on the face of it given the size of the company, but after a tough 2024, when it was in the red for the entire year, what's important is that cash flow from operations is steadily positive even with a large investment program.

Segment performance

In the presentation, Intel breaks down Q1 2026 revenue as follows:

Client Computing Group (CCG): $7.7 billion, +1 percent year-over-year.

Data Center and AI (DCAI): $5.1 billion, +22 percent.

Total "Intel Products": $12.8 billion, +9 percent.

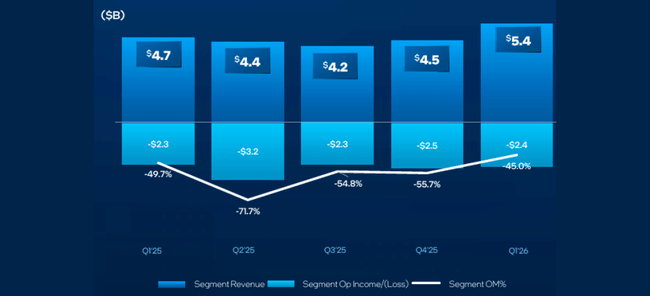

Intel Foundry: $5.4 billion, +16 percent.

Other: $0.6 billion, -33 percent (due to Altera).

Eliminations between segments: -5.3 billion.

Total net sales: $13.6 billion.

Client segment stagnant to slightly increasing. After two years of very weak PC cycles, the one percent growth is more a signal of stabilization than a growth story, but the important thing is that the segment is not falling.

Data Center and AI is key. Here, 22% growth shows that Intel can benefit from the advent of AI not just through GPUs and competitor accelerators, but through the CPU's role as a "guest" processor in AI clusters. Management is saying outright that the next wave of AI will be more about inference and agent models running closer to the user, reinforcing the role of CPU and wafer and packaging services for Intel.

Intel Foundry is growing 16 percent, which is important in terms of the thesis that Intel wants to become an independent foundry player, not just a maker of its own chips. Related to this are new contracts, capacity expansions in Malaysia, and the repurchase of a 49 percent stake in a joint venture around Ireland's Fab 34, which Intel is consolidating fully back on itself.

Management comment

New CEO Lip-Bu Tan describes the quarter as a continuation of the "reset" where Intel has rebuilt the way it operates and is starting to reap the rewards. The key message is that AI is shifting the center of gravity of demand from large training models to inference and agent-based systems closer to the end user, and this dramatically increases the need for CPUs and advanced packaging and wafer services, where Intel has an irreplaceable place.

Tan emphasizes three things. First, for the sixth quarter in a row, Intel delivered revenue above its own guidance - i.e. management is conservatively forecasting and execution is better than it expects. Second, that the new management approach is based on working more closely with customers, listening to their needs and leveraging "differentiated IP" across all parts of the portfolio. Third, that it is investing massively in AI, in-house silicon development and advanced manufacturing, while maintaining discipline on costs, which is reflected in an 8-9 percent decline in R&D and MG&A on a non-GAAP basis.

CFO David Zinsner adds that margin and profit growth is the result of a combination of rising DCAI, better utilization of factory capacity and cost management. He stresses that the priority is to maximize the utilization of the global manufacturing chain so that Intel can meet the growing demand for silicon, which he believes will persist in the AI era.

Q2 2026 Outlook

For Q2 2026, Intel forecasts:

Revenue of $13.8 billion to $14.8 billion, another step up from Q1

GAAP gross margin 37.5 percent, non-GAAP 39.0 percent

GAAP EPS of $0.08, non-GAAP EPS of $0.20

Given that Q1 non-GAAP EPS of 0.29 significantly beat earlier expectations, the market views this outlook as conservative - Intel is leaving room for outperformance in Q2. Most importantly, the company is no longer forecasting Q2 as a loss-making quarter (which was not out of the question just a few months ago) and is clearly communicating that it wants to stay on a trajectory of gradual revenue and profitability growth.

Long-term development

The long-term numbers for 2021-2024 show how deep Intel's crisis was:

Revenue fell from 79 billion in 2021 to 63 billion in 2022, 54.2 billion in 2023 and 53.1 billion in 2024

gross profit fell from 43.8 billion to 26.9 billion, 21.7 billion and 17.3 billion

operating profit shrank from about 19.5 billion to 2.33 billion in 2022, 93 million in 2023 and minus 11.7 billion in 2024

In 2024 Intel reported a net loss of $18.8 billion, roughly minus $4.38 per share. That means a total breakdown in profitability and huge restructuring costs, investments, depreciation and tax implications. EBITDA drops from 33.9 billion in 2021 to just 1.2 billion in 2024.

Q1 2026 is important in this context mainly because it shows:

the first clear return to revenue growth

an improvement in gross margin

a return to solid non-GAAP profitability of over $1.5 billion

a move from zero to $0.29 non-GAAP EPS

Steadily positive operating cash flow in an environment of continued high investment

This doesn't mean Intel is "back to where it used to be." From a GAAP perspective, it's still in the red, and profit and margin levels are far behind what the industry leaders are delivering. But compared to 2024, when the company looked more like a structurally damaged giant, Q1 2026 is the first quarter that consistently shows that turning that tanker around is possible.

Shareholders

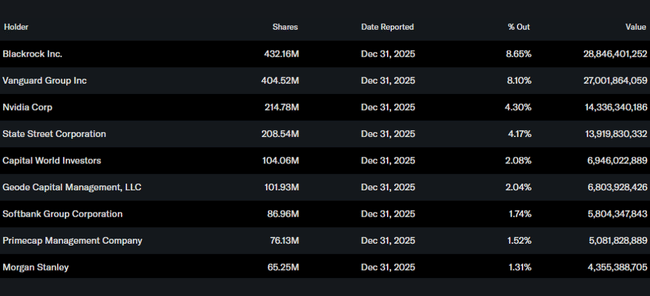

According to the report, insiders hold about 13 percent of Intel's stock, a relatively high proportion for such a large company and reflecting the strong "skin in the game" of management and connected individuals. Institutions own about 61.9 percent of all shares and about 71.1 percent of the free float; over 3,100 institutions hold shares.

The largest shareholders are:

BlackRock with about 432 million shares, or about 8.65 percent

Vanguard with about 405 million shares, or about 8.1 percent

Nvidia with about 215 million shares, about 4.3 percent

State Street with 208 million shares, about 4.2 percent

Nvidia's presence in the top holdings is an interesting signal - whether it's a direct investment or a structured position, it shows that even the AI accelerator leader itself believes Intel will play a role in future AI infrastructure, especially at the CPU and foundry level.

Why the stock jumped nearly 22% after the results

Intel's stock was trading around $66.7 before the results and shot up to around $80 after the results, up nearly 20 percent.

There are basically three reasons:

Non-GAAP EPS of $0.29 is well above its own guidance of $0.00 and above market expectations, which were for marginally positive or zero earnings. In addition, Intel delivered revenue 1.4 billion above the midpoint of the prior outlook.

With Data Center and AI growing 22 percent and Foundry growing 16 percent, the market sees Intel being able to monetize the AI boom not just as a "retro" PC title, but as a relevant player in AI infrastructure, CPU guest role and foundry services.

The outlook for Q2 envisions further growth in sales and profitability, yet looks conservative enough for Intel to outperform it again. This is a big change in sentiment for investors after 2024, when it looked like the company could remain in the red for a long time.

Simply put: this isn't the finish line yet, but the first quarter in which the numbers begin to confirm that Intel's turnaround story in the AI era has a real foundation. That's why the stock is reacting so aggressively to the upside.