Apple | Q2 2026: Revenue grows 17%, EPS and margins beat estimates

Apple has had a very strong quarter, which gave investors exactly what they needed to hear ahead of the impending change in leadership. Revenue and earnings per share beat expectations, gross margin climbed above analyst estimates, and the company added a confident outlook for the next quarter - revenue growth of 14% to 17% versus consensus of around 9.5%.

Although iPhone sales narrowly missed the estimate, other categories - Mac, iPad, wearables and services - beat expectations and China rebounded strongly after a weaker period. The combination of strong numbers, a new $100 billion share buyback program, and a 4% dividend increase helps keep sentiment positive even as the market views Apple mainly through the prism of AI and succession from Tim Cook.

Q2 FY 2026 results: revenue, profit and margin

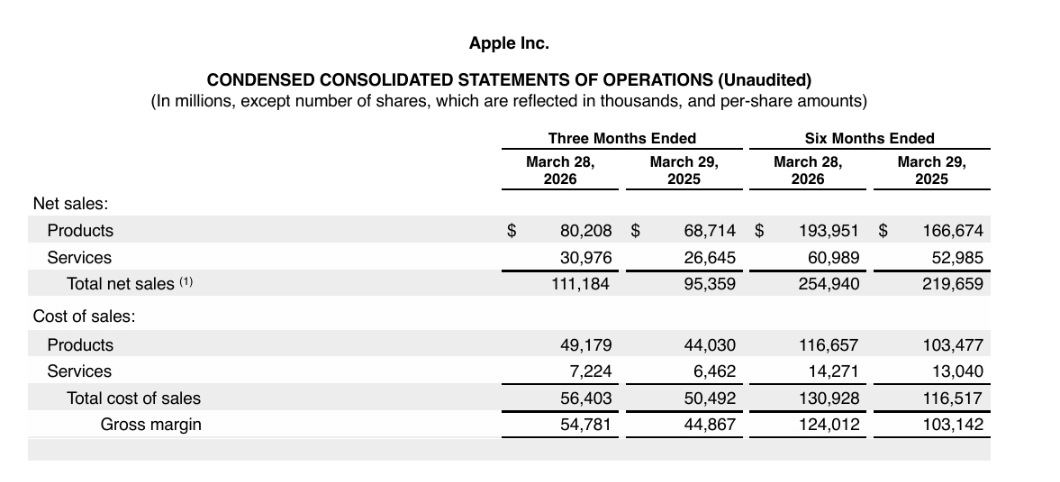

For the quarter ended March 28, 2026, Apple's net sales were $111.2 billion, up from $95.4 billion a year ago, or approximately 17 percent. Compared to analyst consensus of around $109.7 billion, it was a beat of about $1.5 billion, so Apple comfortably beat expectations with sales.

Products earned $80.2 billion (versus $68.7 billion last year), services $31.0 billion (versus $26.6 billion). Gross profit rose to $54.8 billion from $44.9 billion, gross margin increased to 49.3 percent, with the market expecting about 48.4 percent - another beat. The long-term trend of margins moving from the "high 30s" to nearly half of sales continues.

Operating profit came in at $35.9 billion, up from $29.6 billion last year. Net income rose to $29.6 billion from $24.8 billion (+19 percent), and earnings per share (diluted EPS) were $2.01 versus $1.65 a year ago. The consensus was for EPS of $1.95, so Apple beat estimates by about 3 percent.

So for the first six months of the fiscal year, Apple earned $254.9 billion (versus $219.7 billion last year) and netted $71.7 billion (versus $61.1 billion). EPS for the six months is $4.85 versus $4.05 a year ago.

Segments: iPhone, Mac, iPad, wearables and services

By product category, the quarter looks like this:

iPhone: $57.0 billion (vs. $46.8 billion last year), up roughly 22 percent but slightly below market expectations of $57.2 billion.

Mac: $8.4 billion ($7.95 billion last year), above consensus of $8.0 billion.

iPad: $6.9 billion ($6.4 billion last year), above consensus estimates of $6.7 billion.

Wearables, Home and Accessories: $7.9 billion ($7.5 billion last year), slightly above consensus of $7.7 billion.

Services: $31.0 billion ($26.6 billion last year), up about 16 percent, above consensus of $30.4 billion.

Geographically:

Americas: sales of $45.1 billion ($40.3 billion last year).

Europe: 28.1 billion (24.5 billion last year).

Greater China: 20.5 billion (16.0 billion last year), up roughly 28 percent and a clear recovery after weaker periods.

Japan and the rest of Asia also grew, albeit at a slightly slower pace.

Thus, the iPhone remains the key driver (about half of sales), but services and China are becoming increasingly important pillars of growth. Weaker-than-expected iPhone sales are a negative detail, but the overall picture is balanced by stronger Mac, iPad, wearables, and especially services.

Cash flow, balance sheet and capital allocation

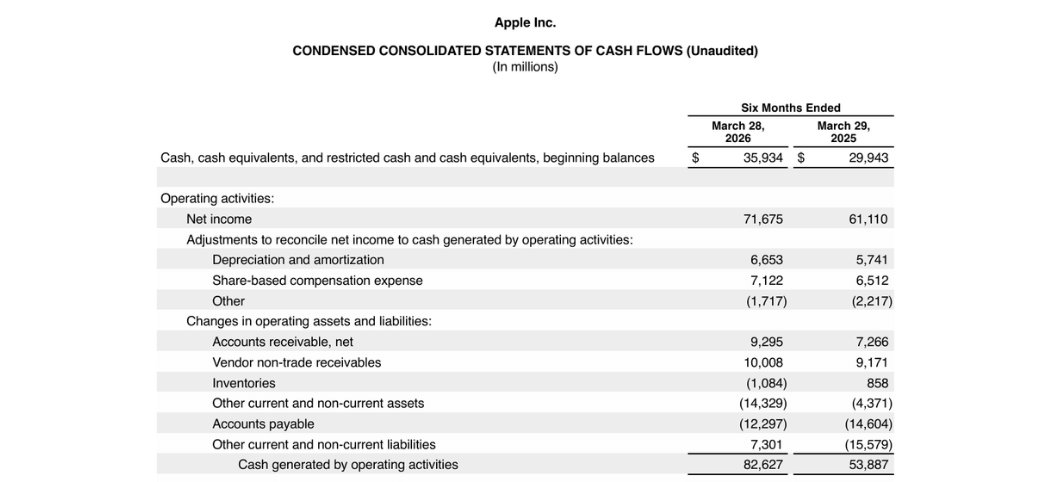

For the first half of fiscal year 2026, Apple $AAPL generated operating cash flow of $82.6 billion, up significantly from $53.9 billion in the same period last year. This reflects not only higher earnings but also favorable working capital development (collections of accounts receivable, reduction in vendor receivables).

Investing cash flow was -$11.1 billion as the firm invested $4.3 billion in assets (capex) while actively managing its securities portfolio - $32.4 billion in purchases and $27.3 billion in collections on securities due and sold.

Financial cash flow was -$61.9 billion, mainly due to:

$37.0 billion of share repurchases

dividends of $7.74 billion

repayment of term debt 7.9 billion and commercial paper 5.9 billion

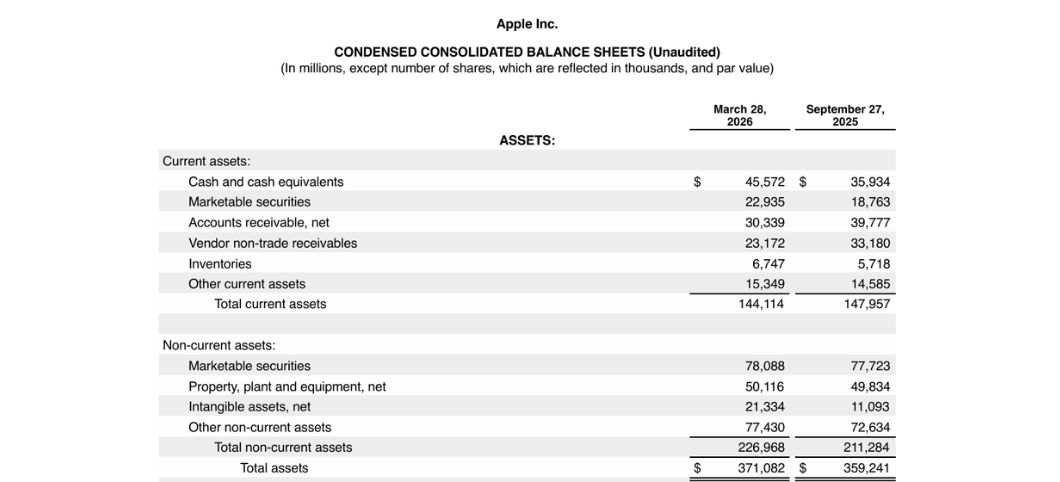

On the balance sheet we see:

$45.6 billion in cash and equivalents (vs. $35.9 billion in September 2025)

short-term securities 22.9 billion, long-term 78.1 billion

for a total of over $146 billion in cash and liquid investments

Total long-term and short-term debt has fallen from roughly $98.7 billion to $84.7 billion, so the net cash position is significantly positive

In addition, the board of directors approved a new $100 billion share repurchase program and increased the dividend to $0.27 per share, a 4 percent increase. This makes it clear to investors that Apple has the capacity to return massive amounts of capital to shareholders even in a time of massive investment in AI and products.

Management Commentary, AI and CEO Change

In the earnings conference call,Tim Cook highlighted that the iPhone 17 is "the most popular lineup in history" and that sales have outpaced internal guidance despite constraints in the supply of memory and other components. CFO Kevan Parekh said they faced supply constraints on both iPhones and Macs in the past quarter, with memory cost increases set to be even more pronounced in the current quarter and likely to remain elevated for longer.

AI is a major theme. Both Cook and Parekh openly say R&D spending is growing faster than sales - R&D shot up 33 percent in the quarter to $11.4 billion from $8.6 billion last year. The main reason is AI: Apple sees AI as a significant opportunity in both products and services, and will invest in it beyond its current product roadmap.

A key strategic element is the collaboration with Google - Apple will use the Gemini model to enhance Siri and other features. Cook says that "the collaboration with Google is going well" and that they are happy with both it and their own internal development. In practice, it's a hybrid AI strategy: partnering where it makes sense for speed and quality, while building out their own capabilities in the cloud and on-premises.

Into this comes a personnel change: after fifteen years, Tim Cook is stepping down as CEO to become executive chairman, and John Ternus, the current head of hardware, will be the new CEO from September. Ternus thanked Cook and shareholders at the call and hinted that Apple has an "incredible product roadmap ahead of us", though he didn't reveal details, of course. For investors, the important signal is that this is an internal successor with a twenty-five-year history at Apple, which reduces the risk of a radical change in direction.

Outlook and why the stock is up 3% after the results

Apple said it expects year-over-year revenue growth of between 14 and 17 percent in its fiscal third quarter (June). Meanwhile, analysts were expecting growth of roughly 9.5 percent to $103 billion, so guidance is well above consensus. The company also indicated that services should continue to grow at a rate similar to the 14 percent growth seen in the previous quarter, and that it plans to maintain high margins despite higher memory costs.

Shares rose about 3 percent after the results as the market got what it wanted despite a minor disappointment with the iPhone:

Sales and EPS beat estimates

gross margin was better than expected

Revenue guidance for the next quarter is well above consensus

Apple announced a new $100 billion share buyback program and raised the dividend

Weaker-than-expected iPhone sales must take a back seat at a time when management says it expects 14 to 17 percent revenue growth in the next quarter despite memory constraints, while clearly communicating an aggressive but controlled AI strategy and continuous management succession. The market reaction is therefore positive, but not overly euphoric - rather, the results confirm that Apple is returning to a growth trajectory after a weaker period, without yet having to dramatically increase capex like some rivals.

Key numbers

Q2 FY 2026 revenue: $111.2 billion, +17% y/y (vs. $109.7 billion expected).

EPS: $2.01 (vs. $1.65 last year and $1.95 expected).

Gross margin: 49.3% (vs. 48.2% last quarter and 48.4% expected).

iPhone sales: USD 57.0 billion, +22% y/y (vs. USD 57.2 billion expected).

Services: USD 31.0 billion, +16% y/y (vs. USD 30.4 billion expected).

Greater China: USD 20.5 billion, +28% y/y.

R&D spending: USD 11.4bn, +33% y/y.

Operating cash flow (6M): USD 82.6bn; buybacks USD 37.0bn, newly authorized buyback program USD 100bn, dividend USD 0.27 per share (+4%).

Stocks mentioned

This article was written and reviewed in line with the Bulios editorial standards.

Follow Bulios on Google News

Be among the first to discover new analyses, news and market moves.