TSMC warns of AI chip shortage until 2028

The world's largest contract chipmaker is benefiting from explosive demand for artificial intelligence, but it is also running into a problem that could affect the entire technology sector. Demand for the most advanced chips is growing faster than TSMC can add capacity.

The AI boom is changing the game

CEO C.C. Wei said at the annual general meeting in Hsinchu that demand for AI chips remains extremely strong. He said $TSM is seeing increasing use of AI in consumer applications, enterprise systems and government projects. All of this is increasing the need for computing power, and therefore the demand for state-of-the-art semiconductors.

The problem is that manufacturing capacity cannot be built overnight. New factories, new lines and advanced chip packaging require years of preparation, billions of dollars of investment and an extremely complex supply chain. That's why TSMC suggests that even expansion in the US may not be enough for the company to fully meet the demand of US customers in the coming years.

Revenues are expected to grow by more than 30%

TSMC also raised its revenue growth outlook for 2026 to more than 30%. Back in January, the company was working with an estimate of around 25%.

Shares of $TSM have appreciated sharply over the past year. The market values the company not only as a chipmaker, but as a strategic infrastructure for the entire AI economy. Without TSMC's manufacturing capabilities, much of the plans of Nvidia, AMD, Apple, Amazon, Microsoft or other hyperscalers could not be realized.

The biggest problem

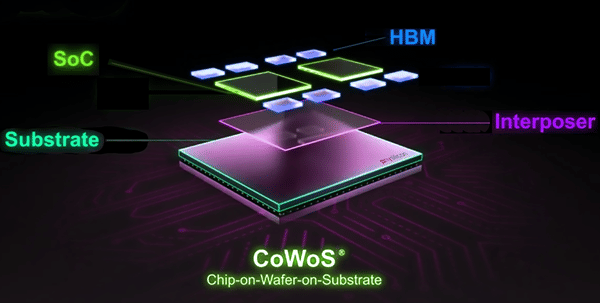

At first glance, the key constraint may seem to be the actual production of chips on a 3nm or 2nm process. But in reality, the situation is more complex. Advanced packaging, especially CoWoS technology, which is essential for powerful AI accelerators, is also becoming a critical bottleneck.

AI chips are not just conventional processors. They require the interconnection of compute units, HBM memory and other components in an extremely compact and powerful package. Without sufficient capacity in advanced packaging, having free wafers is not enough. The resulting chip simply won't get to the customer in time.

That's why the world's largest technology companies are vying for TSMC capacity. Nvidia $NVDA needs manufacturing space for next-generation AI accelerators, AMD $AMD wants to strengthen its position in data centers, and cloud giants are increasingly designing their own chips.

Chip prices and margins

When demand far outstrips supply, pricing dynamics change in parallel. TSMC may move to raise prices for the most advanced manufacturing processes, particularly for 3nm wafers. The market is talking about a possible increase in the second half of 2026 and another in 2027.

C.C. Wei commented:

"TSMC would like to raise prices, but does not want to take an aggressive and short-term approach like some memory companies."

The company is focused on long-term sustainable operations, he said. TSMC doesn't want to maximize profits in just one cycle, but is trying to maintain relationships with customers who are also the largest technology companies in the world.

Higher prices can protect margins

If TSMC is able to make prices more expensive while maintaining high capacity utilization, it can support gross margins. These are one of the most important metrics for investors. Higher margins mean that revenue growth translates better into profits.

On the other hand, TSMC is investing heavily in new factories, technology and geographic expansion. This means high capital expenditure. Investors therefore need to monitor not only revenue growth, but also whether new capacity will fill fast enough and whether the company will maintain pricing power.

Competition

Samsung has long sought to strengthen in the most advanced foundry services and Intel $INTC is building its own foundry model. Yet TSMC still has a huge lead in customer confidence, manufacturing efficiency, and the ability to deliver in high volumes.

From a stock market perspective, TSMC is an indirect bet on the whole AI trend. Nvidia can sell the most powerful accelerators, Microsoft and Amazon can build giant data centers, but without TSMC the supply chain will slow down.

A strategic view

TSMC stands on three pillars:

Long-term growth in demand for AI chips

technological leadership in the most advanced manufacturing

pricing power, which the company gains from a limited supply of capacity

But the risks cannot be ignored either. TSMC is a very capital-intensive business. Each new generation of manufacturing processes costs more money and requires more complex equipment. Another risk is geopolitics, as Taiwan remains a sensitive point in the global economy. Expansion into the U.S. and other regions reduces some of the political risk but also increases costs.

What to watch next

Most important will be capacity development for 3nm and 2nm processes, the pace of CoWoS packaging expansion, and the timing of construction and commissioning of factories in Arizona.

Another key indicator will be demand from Nvidia, AMD and hyperscalers. If orders for AI infrastructure remain high in 2027, TSMC may have room for further revenue and earnings growth. However, if investment in AI data centers slows, the market could begin to reassess current valuations.

The current situation may present both opportunities and risks for TSMC. In the short term, it supports pricing, margins and revenue growth. In the long term, however, it increases pressure on investment, geographic diversification and the ability to maintain a technological edge.

This article was written and reviewed in line with the Bulios editorial standards.

Follow Bulios on Google News

Be among the first to discover new analyses, news and market moves.

Recommended articles