Japan is selling off U.S. Treasuries. What does it mean for stocks?

I came across information that Japan has begun selling U.S. Treasuries in order to have funds to buy yen. I dug into it a bit because there are more layers to it than it appears at first glance.

Why is Japan intervening at all

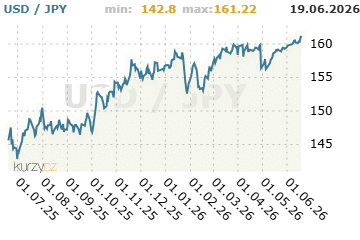

This year alone the yen repeatedly tested the 160-per-dollar mark. That's the level Tokyo considers a red line. A weak yen by itself wouldn't be such a problem; the issue is its combination with expensive imported energy, because oil jumped above $113 per barrel after the Iran war. That made living costs in Japan rise sharply and the Ministry of Finance had to step into the market. By the end of May it had intervened a record roughly $73 billion, which was the largest operation of its kind.

Where they get the money

To finance those yen purchases Japan apparently sold U.S. Treasuries. A small note that media often skip: the BOJ acts only as the executor; the Ministry of Finance makes the decisions. The mechanics are exactly as described: sell bonds, obtain dollars, and buy yen with them. Hard data backs this up too — Japan's holdings of foreign securities fell by more than $75 billion at the end of May compared to April, which matches the scale of the intervention.

A quieter and possibly more important flow

More important than the one-off intervention, it seems to me, is a second, less visible movement. Japanese investors, insurers and pension funds sold nearly $30 billion net in U.S. Treasuries in the first quarter — the largest quarter in almost four years — and the pace is accelerating month by month.

The reason is elegant. The BOJ is limiting purchases of domestic Japanese bonds, so yields at home are rising and Japanese institutions can finally earn returns domestically without currency risk. Suddenly they don't have to go to the U.S. for yield.

Why shareholders should care

Japan is the largest foreign holder of U.S. debt, holding over $1.2 trillion. When it sells or simply buys less, bond prices fall and U.S. yields tend to rise. Estimates suggest pressure on the 10-year yield on the order of 20 to 50 basis points in the medium term. And higher long-term rates flow through to mortgages, corporate financing costs, and stock valuations.

A bigger risk, however, is the carry trade — those hundreds of billions to a trillion dollars borrowed cheaply in yen and poured into riskier assets around the world. If the yen suddenly strengthens sharply, whether due to intervention or rate hikes, investors have to rush to close these positions. That exact mechanism knocked markets down in August 2024.

I'm curious how you see it. Do you take the strengthening yen and Japanese sales as a real risk for equities, or as noise that nobody will care about in a few months?