After years of shrinking revenue, collapsing margins, and strategic missteps, Intel finally seems to be showing faint signs of revival. The company that once defined the semiconductor industry is starting to rebuild its footing, reporting its first quarter of revenue growth and improving profitability in what feels like ages. It’s not a comeback yet — but it’s the first quarter that tells a coherent story about how Intel might actually earn from the AI boom rather than merely watching it happen.

The recovery rests on three fronts: defending its PC chip dominance, regaining lost ground in data centers, and transforming into a global foundry serving other chip designers. With Washington’s billions flowing into domestic chip production and global demand for compute power surging, Intel is trying to catch the right wave. The challenge now is whether a single good quarter can turn momentum into a sustainable turnaround.

How was the last quarter?

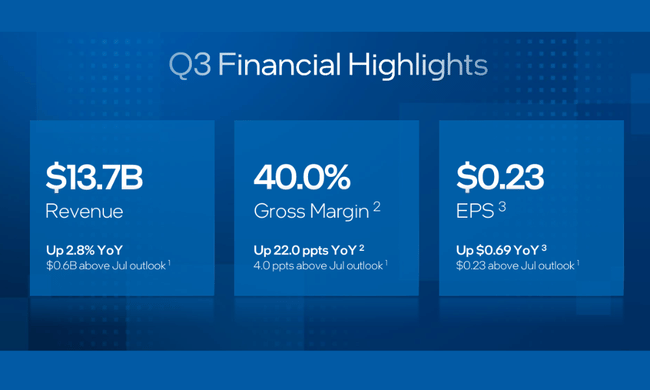

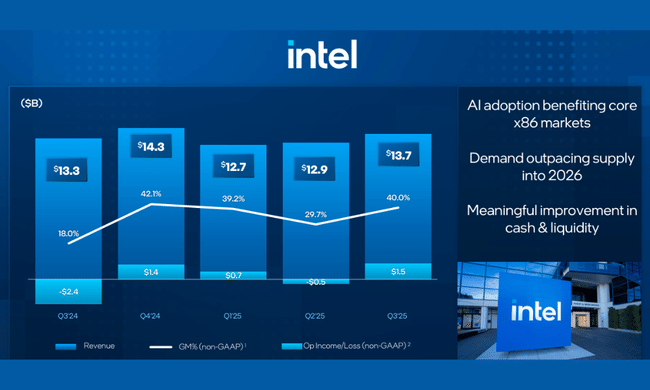

In the third quarter of 2025, Intel $INTC achieved sales of roughly $13.7 billionwhich means 3% year-over-year growth. This is important after several years of declining sales - it shows that the company is no longer in freefall. The growth comes mainly from the fact that demand for PC processors is stabilizing and that new opportunities are emerging in AI, although no significant turnaround is yet visible in data centers.

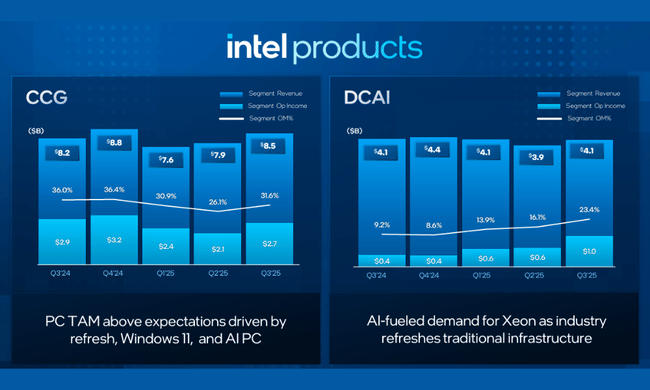

The revenue structure suggests where Intel is really making money today. Client Computing Group (CCG)which is mostly a business around computer processors, made roughly $8.5 billion and grew by about 5 %. This suggests that the PC market has stabilised after the covid boom and subsequent slump and that new generations of chips are being pushed, including platforms targeting AI functions in end devices.

In contrast, Data Center and AI (DCAI) with sales around $4.1 billion declined slightly - by about 1 % year-over-year. In an environment where hyperscale players are massively buying competitors' accelerators, that's not surprising, but it's also a reminder that in data centers Intel is still struggling more to stem erosion than growth. Still, the company's overall product revenue was up roughly 3% year-over-year.

A specific chapter is Intel Foundry. The segment formally has revenues of around $4.2 billionwhich represents a slight decline of 2 %However, it includes internal billing to other divisions, so that some of these sales are eliminated at the consolidated company level. More important than the number itself is that the foundry business is no longer just a plan, but a real, reportable part of the company - and that the big players in the ecosystem are starting to revolve around it.

The tipping point comes at profitability. GAAP gross margin has jumped to 38,2 % from just last year's 15 %which is a dramatic improvement. Adjusted for selected items, the non-GAAP gross margin even got to 40 %. This is a combination of two effects: last year's base was extremely weak due to depreciation and non-recurring costs, while at the same time costs and prices are being better managed, especially in the client business.

The picture at the operating profit level has also changed significantly. Last year in the third quarter, Intel reported operating loss with a margin of around -68 % on a GAAP basis; this year it's positive operating margin of about 5%. Adjusted for selected items, the non-GAAP operating margin up to 11.2%again after a jump from a significant negative. This was helped by a hard cut in costs: the sum of R&D and sales/administrative support expenses fell by about a fifth (GAAP) and just under 17% (non-GAAP) year-on-year, respectively.

GAAP net income in the quarter was around 4.1 billionwhich is visually a huge turnaround from last year's loss 16.6 billion. But this number is largely skewed by one-time items - so for current profitability it is more interesting non-GAAP net income of about $1 billion a earnings per share of about $0.23which means a return to the black, but certainly not a return to the levels of the best years.

In terms of cash in the company, the third quarter is solid. Intel generated roughly $2.5 billion of operating cash flowand while that's not yet an amount that alone would offset the massive investments of the last few years, it shows that the underlying business is no longer in "burn cash" mode.

Outlook

Intel's management expects to achieve a revenue between $12.8 billion and $13.8 billion. It's a range that roughly matches what the company has shown now - no big jump, but no return to decline either. More important than the absolute number is that management's commentary is significantly more confident this time around: current demand is outstripping supply, they say, and that should continue in 2026.

At the earnings level, Intel expects the fourth quarter a slight GAAP accounting loss - management forecasts a roughly -0.14 dollars per share - but after adjusting for selected items, it expects positive non-GAAP earnings of about $0.08 per share. In other words, investments and one-time effects continue to weigh on the bottom line, but the operating business is already above zero.

Strategically, Intel is betting that AI will lift demand for computing power across segments - from traditional x86 platforms in PCs, to data centers, to specialized accelerators and custom solutions. It enters this with the ambition of becoming a key manufacturing partner for third parties in the form of foundry services. A combination of government funding, capital injections from large technology investors and new products on advanced manufacturing processes is set to create the scope for both revenues and margins to improve in the years ahead.

Long-term results

Looking at Intel over the longer term of the last four years, it is very clear how deep a downturn the company has been through. In 2021, it will have lost approximately 79 billion dollarsand a year later still over 63 billionbut by 2023, revenues have fallen to about 54.2 billion and by 2024, they've dropped further to 53.1 billion. This means an overall decline of more than a third in three years. It's a combination of a weakening PC market after the covid boom, pressure from competition in data centers, and Intel having slept through several technology generations of chip production.

Even more dramatic is the evolution of gross profit. In 2021, Intel generated over $43.8 billion in gross profitand by 2022, only about 26.9 billionand a year later, about 21.7 billion and by 2024, only about 17.3 billion. This means that gross profit has virtually been cut in half in three years. The reason for this is obvious: a combination of falling sales and pricing pressure that has failed to adequately reduce costs, plus various fluctuations in the cost structure.

On the other side of the equation is operating costs. On the other side of the equation are operating costs, which in 2021 were around 21.7 billion dollarsrising to around $20 billion in 2022. 24.5 billionfalling back to just over $20 billion in 2023. 21.6 billionto jump up to 29 billion. That's an increase of more than a third in a single year. These figures reflect both increased investment in research and development and restructuring, new projects and a generally costly transformation towards foundry business and new production processes.

Together this has created extreme pressure on operating profit. While in 2021 Intel had an operating profit of nearly $19.5 billiona year later, it had fallen to about 2.3 billionand by 2023, it was teetering around 93 million and by 2024, it had fallen into a deep operating loss of over $11.6 billion. Such a steep drop in profitability in three years is exceptional for such a large company and shows well how challenging Intel's rebuild is.

We see an even starker picture at the level of net income. By 2021, Intel will have earned nearly 19.9 billion dollarsand by 2022, only about 8 billionand by 2023, about 1.7 billion and in 2024, it will report a loss of over $18.7 billion. This is not just about operating results, but also large tax and accounting items - for example, in 2024, the combination of pre-tax losses and specific tax effects resulted in a tax expense of over $7.5 billionmaking the entire accounting result even worse.

All of this has, of course, translated into earnings per share. From a level of around $4.89 per share in 2021, Intel has fallen to $1.95 in 2022, $0.40 in 2023, and ending with a loss in 2024 -4.38 dollars per share. Meanwhile, the number of shares outstanding is growing slightly - roughly from 4.06 billion in 2021 to about 4.28 billion in 2024 - so even from a "dilution" perspective, earnings per share cannot be expected to return to previous levels without a significant improvement in business.

News

In recent months, Intel has announced several major moves that complement the purely financial numbers well:

- Agreed with the U.S. government on a package of support for the development of U.S. chip manufacturing, totaling 8.9 billion dollarsof which it has already received in the third quarter 5.7 billion.

- Established strategic cooperation with NVIDIA to develop several generations of custom data center and PC products to combine Intel's x86 platforms with NVIDIA's accelerated solutions via NVLink.

- NVIDIA also announced a $5 billion investment in Intel stock, signaling that it counts Intel as a major supply chain partner.

- SoftBank Group added another capital signal of confidence with an investment $2 billion in Intel stockfocused on the future of advanced chip manufacturing in the US.

- Intel unveils client processor architecture Intel Core Ultra Series 3 ("Panther Lake") on the Intel 18A processwhich is expected to be the first major test of next-generation manufacturing technology in end devices.

- In the server area, it showed Intel Xeon 6+ ("Clearwater Forest") on 18A, highlighting the leap in performance/consumption ratio, while also outlining the details of the new inference-oriented GPU "Crescent Island".

- Deepened collaboration with Microsoftincluding around Windows ML and the integration of Intel vPro remote management with Microsoft Intune.

Shareholding structure

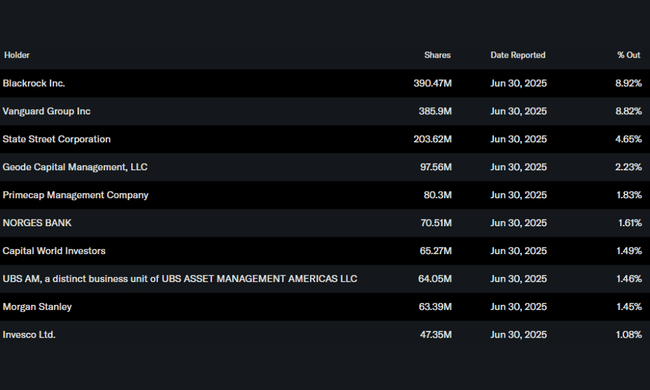

Intel is a typical global blue chip whose shares are dispersed among large institutions and a broad investor base. Insiders - that is, management and people within the company - hold only about 0.07% of the shareswhich is fairly common for a company this size and means that institutional investors have a decisive influence.

They own roughly 63-64% of the shares and the free float. The largest shareholders include BlackRockwhich holds approximately 8.9% of the sharesfollowed closely by Vanguard Group with a stake of around 8,8 %. It also has a strong position State Street (about 4,7 %) a Geode Capital (roughly 2,2 %). The rest is spread among thousands of other institutions around the world and retail investors.

Analysts' expectations

Intel today is primarily in the eyes of the market turnaround story. On one side is the fresh, brutal experience of a profit slump and huge loss in 2024, on the other side is the visible first sign of improvement in Q3 2025 and a series of steps that make sense: collaborations with AI leaders, big government funding, the rollout of foundry services and a new generation of products on more advanced manufacturing processes.

Analysts will be watching three things in particular in the coming quarters. First, whether the maintain and gradually increase gross and operating marginswithout making the results dependent on one-off items. Second, whether the foundry business will actually gain commercially significant contracts and begin to generate growth that is not just internal shifting of numbers between segments. And third, how quickly Intel can to get back on the AI hardware map - not just in marketing, but in real-world delivery, especially in data centers.

Q3 2025 shows that Intel is no longer in a state of free fall, but rather at the beginning of a long road back. For investors looking for a combination of potential with significant risk, it's an interesting bet that the company will manage one of the most challenging technology transformations in the history of the semiconductor industry. But only the next few quarters will tell if the current improvement is not just a short-term blip, but the beginning of a more sustained turnaround.