McDonald’s closed the third quarter of 2025 with results that once again highlight the durability of its global operating model. Even as consumers in many markets tightened spending and traded down across food categories, the company managed to expand both revenue and traffic. Its ability to adjust pricing, fine-tune promotions and lean on digital engagement illustrates why McDonald’s remains the benchmark for stability in the quick-service restaurant industry.

Long-running investment cycles in restaurant modernization, digital ordering and loyalty integration continued to pay off. International markets outpaced the US, while the domestic business benefited from higher average spending and sharper cost management. Together, these factors underscore a strategy built on local adaptability supported by a scale advantage that few competitors can match.

How was the last quarter?

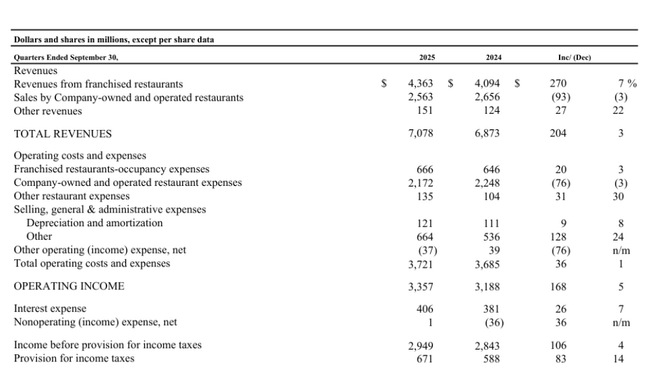

The third quarter brought continued, albeit more moderate, revenue growthfor McDonald's $MCD. Global comparable sales grew 3.6%, with all major geographic segments contributing positively. The US moved up 2.4% on higher average spend per customer, while International Operated Markets added 4.3% and International Developmental Licensed Markets added 4.7%. This broad-based growth confirms the brand's ability to generate stable demand across regions and economic cycles.

Total sales reached $7.08 billion, representing a three percent growth. Profitability remained solid, with operating profit up 5% to $3.36 billion and net profit reaching $2.28 billion. Diluted EPS was $3.18, a two percent improvement. Excluding restructuring costs associated with the Accelerating the Organization initiative, EPS would have remained at $3.22.

The company also grew Systemwide sales to over $36 billion for the quarter and showed very strong performance in its loyalty program, which generated over $34 billion in sales over the past twelve months. This confirms the rapidly growing importance of the digital ecosystem, which is at the core of future growth.

CEO commentary

CEO Chris Kempczinski highlighted that the company has managed to grow across all segments despite the globally challenging environment. He said the key factor is a combination of everyday customer value, affordability and menu innovation, which together maintain stable demand. In addition, marketing campaigns and consistent building of iconic products contribute to high footfall even at a time when consumers are cutting back on discretionary spending.

Kempczinski stressed that the company will continue to invest in digital channels, accelerate operations and develop value propositions to sustain growth momentum even as customers become more price sensitive. Management's message is clear: growth is sustainable through strategic discipline, brand strength and customer loyalty.

Outlook

Management's outlook remains cautiously optimistic. McDonald's expects revenue growth to continue, although it may vary across regions depending on the local economic environment. The company cautions that while inflationary pressures are easing, consumers remain price sensitive, requiring careful work with both value proposition and price elasticity.

Digital will play an increasingly strong role - particularly the growth of orders through mobile apps, loyalty programmes and managed promotions. Systemwide sales should continue to strengthen, driven by franchise expansion, restaurant modernization and a growing share of international markets, including regions that are recovering faster than the U.S. from the pandemic.

Long-term results

Viewed over the past four years, McDonald's shows remarkable consistency. Revenues have grown from $23.18 billion in 2022 to $25.92 billion in 2024. While the rate of growth has fluctuated, the business has maintained high margins - gross margins have remained around 56-58% over the long term, which is exceptional within the industry.

Operating profit in 2024 was US$11.71 billion and remains well above pre-pandemic levels, despite higher operating costs and investments. Net profit for 2024 was $8.22 billion, with EPS of $11.45. These results demonstrate the company's steady ability to generate capital and invest in future expansion, modernization and marketing.

Revenue grew steadily and McDonald's was able to reduce the number of shares outstanding due to its disciplined capital policy, supporting EPS growth. EBITDA remained well above $13 billion, confirming strong cash-flow generation. Thus, history clearly shows the company as a stable leader with high return on capital.

News

- Company continues restructuring initiative Accelerating the Organizationto improve the efficiency of global processes and optimize costs.

- McDonald's has seen exceptionally strong growth in its loyalty ecosystem, which is becoming a major source of repeat visits.

- Some markets, notably Germany, Australia and Japan, are driving global growth through local campaigns and higher visit frequency.

- Pricing strategy is being adjusted in response to changes in customer behaviour and competitive pricing pressures.

Shareholding structure

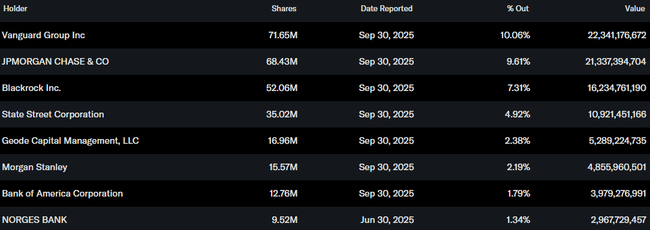

McDonald's has a very strong institutional base, with more than 75% of shares held by institutional investors, confirming the stable confidence of professional capital. The largest shareholders are Vanguard Group (10.06%), JPMorgan (9.61%), BlackRock (7.31%) and State Street (4.92%). Insider ownership is minimal, around 0.23%, which is consistent with the nature of a mature global corporation.

Analysts' expectations

According to the latest analysis UBS the bank affirms its rating on McDonald's Buy and a target price of $350. UBS expects 2026 to bring a recovery in operating margins due to lower labor costs in the U.S. and accelerating growth in key international markets, particularly Germany and Australia. The firm stresses that digital will remain the main growth driver: according to their model, sales generated through mobile app and loyalty program could exceed USD 40 billion in 2026 , significantly increasing visit frequency.

UBS also points out that MCD has one of the most stable cash flows in the QSR sector, which has enabled it to grow its dividend above the rate of inflation over the long term. Analysts also appreciate the firm's ability to pass on inflation to prices without a significant decline in visitation - which they see as a key factor in an environment of geopolitical and macroeconomic uncertainty.