Target’s third quarter shows a retailer operating in a restrained consumer environment, where spending remains selective and discretionary categories continue to lag. Revenue pressure persists, but the story is no longer just about weaker demand. The company is deliberately reshaping its business toward areas with higher resilience, including digital fulfillment, advertising services, and membership-driven loyalty.

Rather than signaling a sharp turnaround, the quarter reflects a phase of controlled adjustment. Target is prioritizing margin stabilization and operational flexibility while positioning itself for the most critical shopping period of the year. For investors, the key takeaway is not acceleration, but durability — the ability to adapt while consumer confidence remains fragile.

How was the last quarter?

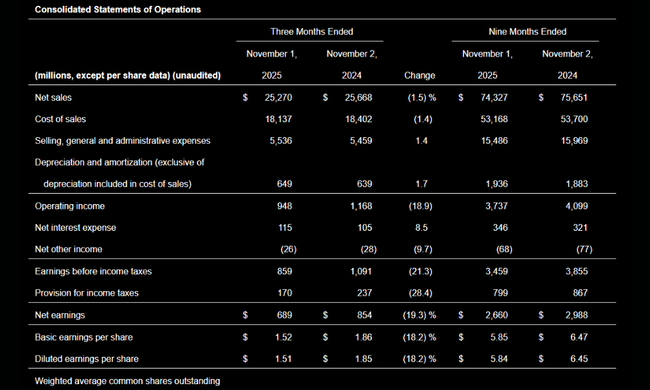

Third-quarter sales were $25.3 billion, down 1.5% year-over-year. This was primarily driven by weaker merchandise sales, where merchandise sales declined 1.9%. Consumers continue to limit purchases of surplus merchandise and favor basic categories, which is particularly negative for fashion, home accessories and higher price segments. Total comparable sales declined by 2.7%, with brick-and-mortar stores recording a 3.8% decline.

On the other hand, digital channels continue to improve gradually. Digital comparable sales increased by 2.4%. This growth is closely linked to the programme Target Circle 360which strengthens purchase frequency and customer loyalty. Digital is thus acting as a stabilising element in an environment of weaker footfall in brick-and-mortar stores.

Positive developments are also evident in the sales structure. Food & Beverage and the Hardlines segment were able to grow in the quarter, confirming that Target maintains a strong position in everyday shopping and affordable categories. Non-merchandise revenue growth was even stronger, up nearly 18% year-over-year. Advertising Platform Roundel, membership programs and marketplace are generating double-digit growth rates and gradually improving the quality of revenues as they are less sensitive to cyclical swings in consumer demand.

Profitability remains under pressure. GAAP EPS was $1.51 versus $1.85 a year ago, while adjusted EPS was $1.78. Operating profit fell to $0.9 billion and was $1.1 billion after adjusting for one-time items. Operating margin and operating margin declined to 3.8% and 4.4%, respectively, on an adjusted basis. Gross margin remained relatively stable at 28.2%, with higher markdowns offset by advertising revenue growth, lower shrinkage losses and improved efficiencies in logistics and digital fulfillment.

Management commentary

Incoming CEO Michael Fiddelke described the results as fully in line with internal expectations and highlighted the company's readiness for the Christmas season. He said management is focused on three key priorities: strengthening business authority in key categories, improving the overall shopping experience and deeper use of technology across the business.

Management's comments indicate that improving margins is not the main focus in the short term. The priority is to stabilize volumes, strengthen customer loyalty and build revenue streams that have higher long-term returns than net merchandise sales.

Outlook

The outlook for the fourth quarter remains conservative. Target continues to expect year-over-year sales declines in the low single-digit percentages, reflecting continued consumer caution during the holidays. Full-year GAAP EPS is expected to be in the range of $7.70 to $8.70, while adjusted EPS is now expected to be between $7.00 and $8.00.

The key question remains whether an aggressive pricing strategy, broader product mix and a focus on value can attract higher volumes without further pressure on margins. The Christmas season will test Target's ability to combine affordability, fast delivery and attractive offerings in an environment where competition is extremely strong.

Long-term results

The long-term view shows Target $TGT as a company that is in a normalization phase after an exceptionally strong 2022. Revenues have hovered around $106-109 billion in recent years, and 2025 brought an interim slight decline. Gross profit remains stable, reflecting resilient pricing and effective cost management at the supply chain level.

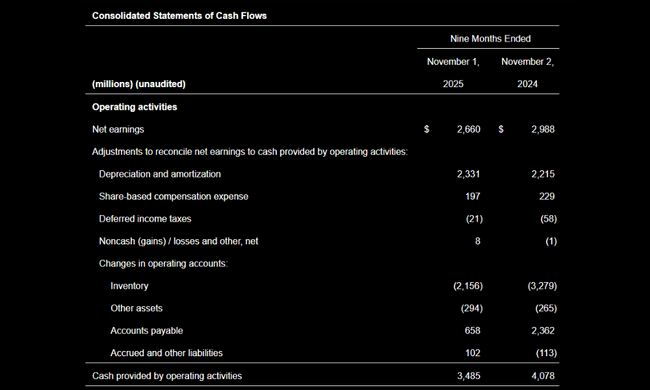

However, operating and net profits are significantly lower than at the peak of the cycle. Net income for 2024 was $4.1 billion and diluted EPS was $8.96, roughly 35% lower than 2022. On the positive side, the stable number of shares outstanding and EBITDA of around $8.7 billion gives the company room for dividends, investments and maintaining a strong balance sheet.

News

Target $TGT enters the holiday season with one of its broadest offerings in years. More than 20,000 new items, more than half of which are exclusive, are set to add to the appeal of the assortment. The company is also pushing hard on the perception of value - from a holiday menu for four under $20 to thousands of gifts priced from $5.

There is also a strong focus on logistics and convenience. Expanding next-day delivery to more than half of the U.S. population and strengthening same-day service is intended to help Target compete not only on price, but also on speed and availability.

Shareholder Structure

Target's ownership structure is highly institutional. Over 85% of the stock is held by institutions, with the largest shareholders being Vanguard Group with nearly 13%, State Street with over 8%, and BlackRock with approximately 8%.

Analyst expectations

Analysts remain cautious in the near term, but are tracking several positive structural trends. Digital revenue growth, advertising platform expansion and stabilizing margins in grocery may gradually improve earnings quality. A key catalyst through 2026 remains the return of discretionary demand and Target's ability to turn digital traffic into sustainable profits.