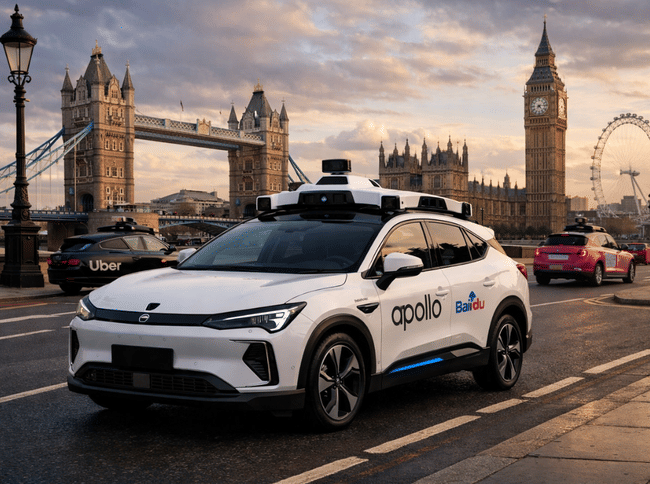

After years of regulatory hesitation, Europe is stepping directly into the frontline of autonomous mobility. London is emerging as the first major European city where robotaxis will not merely be tested, but deployed in real urban conditions. The convergence of Uber, Lyft, and China’s Baidu signals a shift from controlled pilots to competitive, market-driven experimentation.

What makes London unique is not just its size or density, but its regulatory posture. The UK is positioning itself as a proving ground where technology, safety, and scalability collide under real-world pressure. For investors, this moment matters: cities that successfully absorb autonomous transport early tend to shape platform dominance for years to come.

What exactly are Uber, Lyft and Baidu up to

The crux of the deal is the integration of autonomous cars Apollo Go RT6 from Baidu $BIDU into London's Uber $UBER and Lyft $LYFT networks . The deployment is planned for 2026 and will be the first time Chinese robotaxi technology will directly connect with US ride-hailing platforms in a European metropolis.

Key features of the project:

- Driverless vehicles will be available directly on the Uber and Lyft apps

- Baidu to supply autonomous driving technology and fleet of cars

- Uber and Lyft will provide demand, pricing and operational infrastructure

This move makes London the place where three different approaches collide for the first time in Europe: US platforms, Chinese autonomy and the UK regulatory framework.

Why the UK is ahead of the rest of Europe

The main reason why robotaxis are taking off in the UK is Automated Vehicles Act 2024. This law addresses a problem on which the EU has long failed: accountability.

While Europe is still sorting out whether the manufacturer, the software or the 'driver' is responsible for an accident, UK legislation simplifies things. It shifts legal responsibility to the so-called 'driver'. authorised self-driving entity - the company that operates the autonomous system.

This has major implications:

- Regulatory uncertainty is significantly reduced.

- allows commercial operation, not just testing

- opens the door to faster scaling of fleets

For technology firms, this is a clear signal that Britain wants to be a leader in autonomous mobility, not a bystander.

Competition is growing: Waymo, Wayve and the global race

Uber and Lyft are not alone in London. Alphabet's $GOOG-owned Waymo has already begun human-monitored trials in the city, and British startup Wayve is preparing for fully autonomous operation in 2026. What's more, Wayve is betting on a different philosophy - called mapless AIwhich learns to drive without detailed HD maps.

Wayve has made a roughly billion-dollar investment led by SoftBank and Uber, showing that London is becoming a magnet for capital and talent. Similar dynamics can be seen globally:

- Baidu and WeRide are expanding into the Middle East and Switzerland

- US has strong hubs in San Francisco and Austin

- China is building mass operations in Wuhan, for example

This puts London in the top league of the world's robotaxi cities.

Economic reality: technology promising, profit uncertain

Although robotaxis promise safer, cheaper and greener transport, investors remain cautious. Publicly traded companies like Pony.ai or WeRide are still losing money and the cost of autonomous fleets remains extremely high.

For Uber and Lyft, this presents a dilemma:

- robotaxis can reduce driver costs in the long run

- but in the short term, they can squeeze margins due to high investment

- threatens to cannibalize the existing model

That's why analysts are increasingly talking about hybrid model - a combination of autonomous cars and human drivers to manage peaks in demand and better manage prices.

What this means for Uber, Lyft and investors

For Uber, London is the next step in building a global autonomous strategy without the company bearing the full technological risk. For Lyft, the UK project carries even more weight - it fits in with its international expansion following its acquisition of European app FreeNow.

From an investment perspective:

- Uber is strengthening its position as a platform, not a technology maker

- Lyft seeks to reduce dependence on the US market

- Baidu gains coveted entry into the European market

If London's model proves successful, it could become a template for other metros. And therein lies its real significance: it is not just a few autonomous cars, but a test of the future structure of urban mobility.

Conclusion: London as a litmus test for the future of mobility

What happens in London over the next few years will have an impact far beyond the UK. It will not just be a test of autonomous cars in dense urban traffic, but a test of the whole ecosystem: legislation, operational economics, technological reliability and public willingness to embrace fundamental change in transport. London is an extremely challenging environment - chaotic junctions, historic infrastructure, unpredictable road user behaviour - which is why its outcome carries so much weight.

If robotaxis can be operated here safely, smoothly and at least on a path to economic sustainability, it will greatly strengthen the case for their mass deployment in other world capitals. Conversely, failure could slow down the entire sector for years and confirm investor fears that autonomous mobility will remain a capital-intensive experiment for longer without a clear return.

From an investment perspective, it is important to perceive that Uber and Lyft are not playing for immediate profit, but for strategic positioning. Robotaxis are not a short-term revenue catalyst, but a long-term bet to restructure urban transport. Platforms that build regulatory know-how, partner relationships and operational data early on can dominate the mobility distribution layer in the future - regardless of who supplies the hardware itself.

London is thus becoming a kind of global reference market. Regulators in the EU, the US and Asia will be watching its development closely, as will automakers, chipmakers and infrastructure investors. The outcome will influence not only where robotaxis spread first, but also whether autonomous transport becomes a real business or remains a technology with great potential but limited application.