The latest quarter confirms that CrowdStrike has entered a different stage of its maturity, one where the pace of growth no longer comes at the expense of financial discipline. The company is demonstrating that it can scale quickly while maintaining solid cash generation and increasingly visible operational efficiency. For investors, this is the sign of a business starting to run on autopilot.

But the key change is at the strategic level. CrowdStrike is transforming from a point security solution into a critical layer of modern IT infrastructure. As customers adopt more functionality and integrate the platform into their daily processes, the revenue model becomes more resilient, and vendor dependency grows in a natural, not forced, way.

How was the last quarter?

CrowdStrike $CRWD achieved total revenue of $1.23 billion in Q3 FY2026, up 22% year-over-year. The vast majority of revenue continues to come from the subscription model, where revenue grew 21% to $1.17 billion. This development confirms the stability of recurring revenues and high visibility of future cash flow.

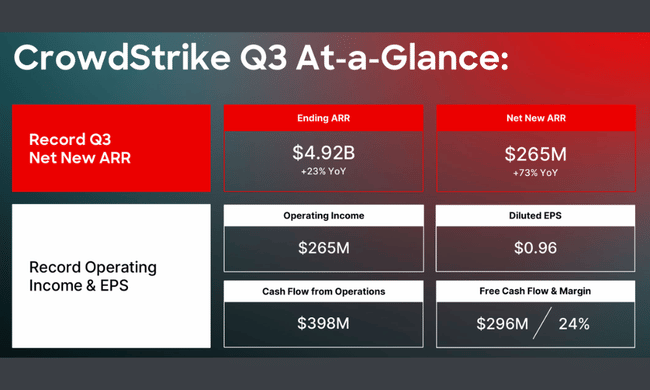

A key indicator for the quarter was net ARR growth, which reached a record $265 million. This accelerated the year-on-year growth rate of net new ARR to 73%, an exceptionally strong dynamic even in the context of the broader software market. Total ARR at the end of October rose to $4.92 billion, up 23% year-on-year.

Profitability moved differently on a GAAP and non-GAAP basis. While on a GAAP basis the company posted an operating loss of $69 million, on an adjusted basis operating profit reached a record $265 million. Non-GAAP net income rose to $245 million and earnings per share reached $0.96, a significant year-over-year improvement.

Cash flow developments were also very strong. Operating cash flow was $398 million and free cash flow was $296 million, confirming that CrowdStrike is no longer just a growing company, but is starting to generate a significant cash surplus. The cash position at the end of the quarter was $4.8 billion, giving the company significant strategic flexibility.

Comment from CEO

George Kurtz called the third quarter one of the best in the company's history and emphasized that CrowdStrike is becoming a key player in the secure AI transformation. He said the combination of the Falcon unified platform and Falcon Flex subscription enables customers to consolidate security tools and reduce IT infrastructure complexity.

The leadership also emphasized that ARR growth is no longer being driven solely by endpoint protection, but increasingly by cloud security, identity and next-generation SIEM solutions. This breadth of the portfolio strengthens the company's long-term competitive advantage.

Outlook

Based on strong momentum in the third quarter, CrowdStrike has improved its outlook for the full fiscal year 2026. The company now expects revenue of approximately $4.80 billion and non-GAAP operating profit of more than $1.0 billion. Adjusted earnings per share are expected to be about $3.70.

For the fourth quarter, the company expects continued solid revenue growth to approximately $1.29 billion to $1.30 billion, with a continued focus on maintaining solid margins and continued acceleration of net new ARRs. Management also suggests that the strong pipeline is a good case for growth in 2027.

Long-term results

From a long-term perspective, CrowdStrike confirms that its business model is structurally highly scalable. The company has repeatedly increased the average number of modules per customer - more than half of its customers now use six or more modules on the Falcon platform, and the proportion of customers with seven and eight modules continues to grow.

This trend translates not only into faster ARR growth, but also improved unit economics for customers. Gross subscription revenue margins have been around 80% for a long period of time, giving the company significant headroom to invest in both development and expansion without significant pressure on profitability.

At the same time, it is clear that CrowdStrike is gradually moving from a phase of net growth to a combination of high growth and profitability. Growing free cash flow and a strong balance sheet increase the company's resilience to cyclical fluctuations in IT spending.

News

In the third quarter, CrowdStrike further expanded its product portfolio, particularly in the area of AI-based security. The company introduced its next generation of identity protection, data protection, IT environment solutions and agent-based AI tools under the name Charlotte AI. These innovations strengthen the company's position in so-called agent-based security, which is increasingly important as AI systems become more autonomous.

Strategic partnerships also play a significant role. Collaborations with AWS, NVIDIA, EY, EY, KPMG and CoreWeave confirm that CrowdStrike is seen as a key security partner for cloud and AI infrastructure by global players.

Shareholder Structure

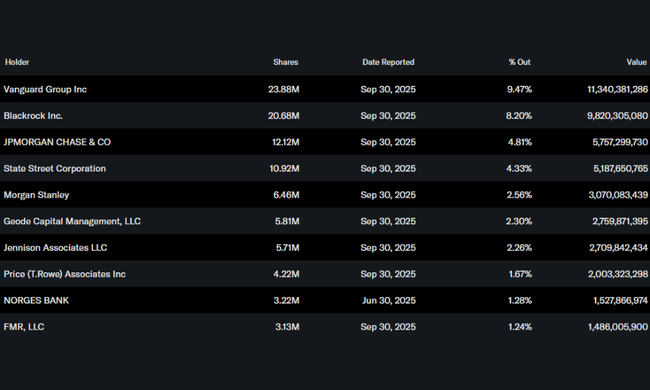

CrowdStrike's shareholder structure is typical of high-quality technology companies. Around three-quarters of the shares are held by institutional investors, dominated by the largest global asset managers, led by Vanguard Group, BlackRock and State Street. The share of insiders remains relatively low, reflecting the company's more mature stage of development and the wide dispersion of capital among institutional investors.

Analysts' expectations

Analysts are very positive on CrowdStrike's results, mainly due to accelerating ARR growth and record cash flow. Consensus is moving toward the view that CrowdStrike has the potential to maintain its growth momentum in the broader cybersecurity market over the next few years.

In particular, the company's ability to monetize trends in artificial intelligence, consolidate security tools with customers, and increase operational leverage are viewed positively. Despite a relatively higher valuation compared to traditional software firms, analysts emphasize that the combination of growth, margins, and cash flow gives CrowdStrike an attractive long-term above-average profile.

According to 12-month price targets 52 analysts for CrowdStrike, the average target is $555.10. The highest price target for CRWD is $706.00 while the lowest price target for CRWD is $353.00.