Oracle’s second fiscal quarter marks a clear inflection point. What once looked like a steady enterprise software business is increasingly defined by infrastructure scale, contracted revenue, and long-duration demand tied to AI workloads. The numbers signal more than momentum—they show compounding effects from years of capital deployment into data centers and cloud architecture.

What differentiates Oracle now is positioning. Instead of chasing hyperscalers head-on, it has carved out a hybrid lane that blends databases, applications, and infrastructure with a pragmatic multicloud strategy. This quarter highlights a business expanding its addressable market while locking in visibility through backlog growth rather than relying on short-term consumption spikes.

What was the last quarter like?

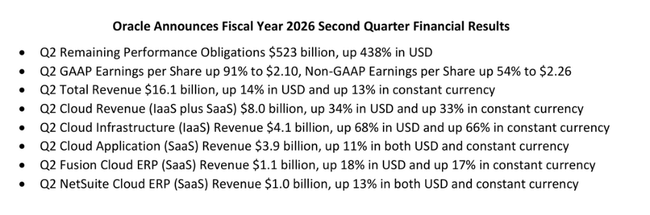

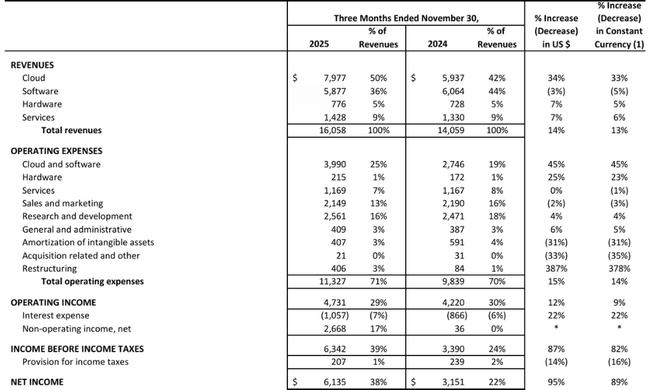

Oracle's $ORCL totaled $16.1 billion in revenue in the second fiscal quarter of 2026, representing year-over-year growth of 14% in dollar terms and 13% in constant currencies. The cloud remains a key driver, with revenue up 34% to $8.0 billion. Virtually half of total revenue is now derived from cloud activities, fundamentally changing the structure of the business.

The fastest-growing component is cloud infrastructure (IaaS), where Oracle reported revenues of USD 4.1 billion, equivalent to 68% year-on-year growth. This figure is extremely important as it confirms that Oracle is not just a secondary player in cloud infrastructure, but can win large and long-term contracts, often associated with AI workloads. Cloud applications (SaaS) grew at a slower but still solid rate of 11%, with Fusion Cloud ERP increasing revenue by 18% and NetSuite Cloud ERP by 13%.

Conversely, traditional software licensing and support saw a year-over-year decline, but this is not a negative signal. This is an expected consequence of customers moving to a cloud model, which reduces short-term license revenue but significantly increases long-term revenue visibility.

Profitability was significantly impacted by a one-time factor in the quarter. GAAP operating profit was $4.7 billion and non-GAAP operating profit was $6.7 billion. GAAP net income was $6.1 billion and non-GAAP net income was $6.6 billion. GAAP earnings per share increased 91% year over year to $2.10 and non-GAAP EPS increased 54% to $2.26. The $2.7 billion pre-tax gain on the sale of the stake in Ampere played a significant role here, which needs to be clearly separated from operating performance when interpreting the results.

Remaining Performance Bonds are an extremely strong signal of future growth. These were up 438% year-on-year to $523 billion, with $68 billion growth in the quarter alone. These are commitments from long-term contracts that will translate into revenue in future years and dramatically increase visibility of future cash flow.

Management Commentary

CFO Doug Kehring identified RPO growth as a key highlight of the quarter and explicitly mentioned new commitments from companies such as Meta and NVIDIA. In his view, it is the long-term cloud and AI contracts that are fundamentally changing Oracle's economics and proving that the company can compete in even the most challenging infrastructure projects.

Larry Ellison (ex-CEO and current Chairman of the Board) explained the strategic decision to sell its stake in Ampere as part of a broader change in approach. According to him, Oracle does not want to be tied to its own chip architecture, but is pursuing a policy of chip neutrality. The goal is to be able to deploy whatever CPU or GPU customers choose and remain as flexible as possible in an environment of rapidly changing AI technologies. This approach directly supports the growth of the cloud and reduces the technological limitations of datacenters.

CEO Clay Magouyrk emphasized the operational side of the business and Oracle's ability to build and operate highly automated datacenters. Oracle currently has over 211 live or planned regions worldwide and is more than halfway through building 72 multicloud datacenters integrated into Amazon, Google and Microsoft environments. It is the multicloud business that Oracle has identified as the fastest growing part of the business, growing 817% year-on-year.

Outlook

Although Oracle did not provide a detailed quantitative outlook for the entire fiscal in this announcement, the dynamics of RPO alone fundamentally change the company's forward-looking profile. Contract commitments of $523 billion suggest that cloud revenues will continue to grow at double-digit rates in the coming years, even with a potential macroeconomic slowdown.

The ability to translate RPOs into actual realized revenue while maintaining margins will be a key factor. In particular, investors will be watching to see whether the high growth rate of IaaS will put pressure on operating margins or whether automation and scaling will confirm the long-term attractive economics of this segment.

Long-term results

Oracle's long-term performance shows a company that has undergone a significant transformation without losing financial stability. Revenue grew from approximately $42.4 billion in fiscal 2022 to $57.4 billion in 2025, with growth rates stabilizing in the mid-single to low double-digit range after a strong 2023. This reflects a gradual shift from a licensing model to the cloud, which dampens growth in the short term but enhances quality.

Gross profit has seen significant improvement, particularly in the last year when cost of sales has fallen sharply. This led to an increase in gross profit to over $55 billion and a significant improvement in the margin profile. Operating costs have skyrocketed in the last year, driven by datacenter expansion, AI infrastructure investments and global cloud expansion. Despite this pressure, operating profit rose to $17.7 billion, confirming that cost growth is still fully under control.

Net profit nearly doubled in four years to $12.4 billion. Earnings per share grew consistently at a rate of 17-27% per year, despite a modest increase in the number of shares outstanding. EBITDA grew from USD 13.5 billion to nearly USD 24 billion, clearly illustrating the significant strengthening of the ability to generate cash. It is this cash strength that provides the basis for financing further expansion without materially impairing the balance sheet.

News

The most significant strategic news of the quarter is the definitive confirmation of the cloud and chip neutrality policy. Oracle openly defines itself against closed ecosystems and builds its growth on the ability to run databases and applications in any cloud. The extremely rapid growth of multi-cloud databases suggests that this approach is finding resonance with customers and could become one of the main growth drivers in the coming years.

Shareholding structure

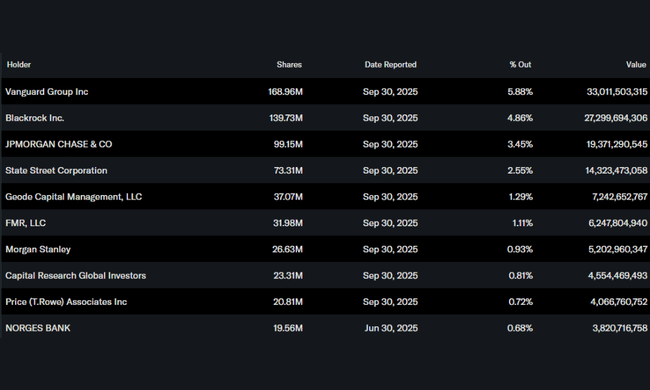

Oracle's shareholding structure is characterised by a high proportion of insiders holding over 40% of the shares, reflecting the strong influence of the founders and long-term management. Institutional investors hold approximately 45% of the shares, with the largest shareholders being Vanguard Group, BlackRock, JPMorgan Chase and State Street. This combination provides both strategic management stability and the presence of large institutional capital.

Analysts' expectations

Analysts view Oracle less and less as a traditional enterprise software firm and more and more as an infrastructure and AI title. A key theme going into the next few quarters is the ability to monetize the massive RPO backlog and confirm that cloud infrastructure growth is sustainable over the long term even with high competition from hyperscalers. If this trajectory is confirmed, Oracle has the potential to reassess its investment thesis towards higher valuations.