Broadcom’s latest results highlight a shift that investors increasingly reward: moving away from short-term semiconductor cycles toward long-duration infrastructure demand. Rather than benefiting from AI as a peripheral trend, the company has positioned itself as a core supplier to hyperscale data centers and high-performance networking environments that underpin large-scale AI deployment.

What stands out is not just the pace of revenue growth, but the quality behind it. Strong margins and robust cash generation suggest that Broadcom is monetising AI demand in a fundamentally different way than many capital-intensive peers. For investors, this combination of scale, profitability, and visibility reshapes how the business should be valued in an AI-driven market.

How was the last quarter?

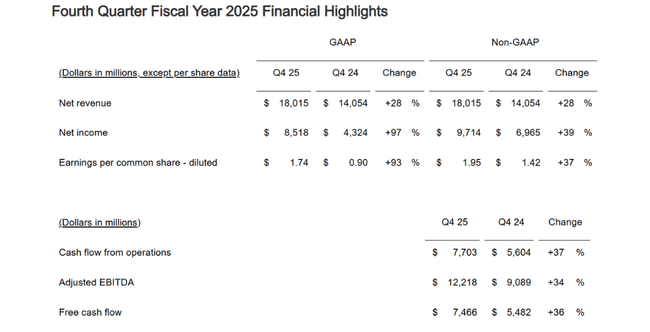

Broadcom $AVGO fiscal fourth quarter 2025 revenue was $18.0 billion, up 28% year-over-year. Growth was driven primarily by the semiconductor division, where revenue grew 35% to $11.1 billion. A key factor was a sharp increase in AI chip revenue, which management said grew 74% year-on-year.

Profitability improved at an even stronger pace than revenue itself. GAAP net income reached $8.5 billion, nearly doubling from the same period last year. GAAP earnings per share rose 93% to $1.74, while non-GAAP EPS reached $1.95, up 37% year-over-year. Adjusted EBITDA was $12.2 billion, equivalent to an exceptionally high margin of approximately 68% of sales.

Cash development was also very strong. Operating cash flow was USD 7.7 billion and free cash flow was USD 7.5 billion, representing about 41% of sales. Thus, even with rapid growth, Broadcom has maintained an extremely high ability to generate cash, which is key for further investments, acquisitions and return of capital to shareholders.

CEO commentary

CEO Hock Tan called the quarter a record quarter and highlighted that the main driver was AI semiconductor growth, particularly in custom accelerators and Ethernet switches for AI datacenters. The trend is not stopping, he said, and the firm expects AI chip revenue to double again year-on-year in the first quarter of fiscal 2026.

CFO Kirsten Spears added that strong EBITDA growth and free cash flow enabled the dividend to increase further. Management, she said, remains disciplined in its capital allocation and aims to continue to combine growth, high profitability and regular increases in shareholder returns.

Outlook

For the first quarter of fiscal year 2026, Broadcom expects revenue of around $19.1 billion, which would imply further year-on-year growth of around 28%. Adjusted EBITDA is expected to be around 67% of revenue, confirming that the company does not expect significant margin pressure even as it continues to expand AI capabilities.

Continued strong demand for AI infrastructure, particularly from hyperscalers and large technology firms investing in proprietary AI models and data centers, remains a key driver of the outlook.

Long-term results

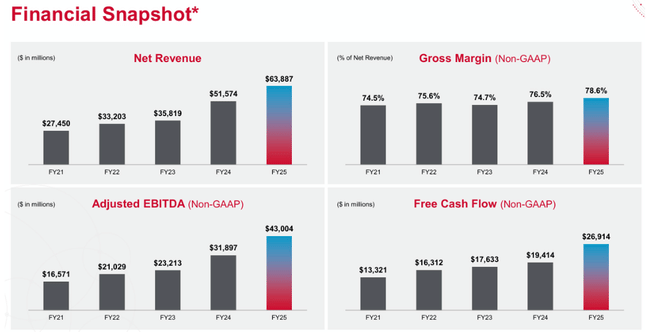

A long-term view of Broadcom's performance shows a company that has undergone a significant transformation towards a highly profitable technology business. Revenue grew from approximately $33.2 billion in fiscal 2022 to $63.9 billion in 2025. This growth has not been uniform, but has accelerated significantly in the last two years, largely due to expansion in AI and infrastructure software.

Gross profit has grown to $43.3 billion and margins have remained very high over the long term. Operating profit reached USD 25.5 billion in 2025, almost double the 2023 figure. Net profit jumped to USD 23.1 billion, with a significant role played not only by operational performance but also by an efficient tax structure.

Earnings per share increased from $2.74 to $4.91 over the past four years, despite a slight increase in the number of shares outstanding. EBITDA rose to $35.5 billion, clearly confirming the company's extraordinary ability to generate cash across cycles.

News

The company announced a 10% increase in its quarterly dividend to $0.65 per share, marking the fifteenth consecutive dividend increase since its introduction. At the same time, Broadcom continues to strengthen its position in custom AI chips and networking solutions that are critical to running modern data centers.

Shareholder Structure

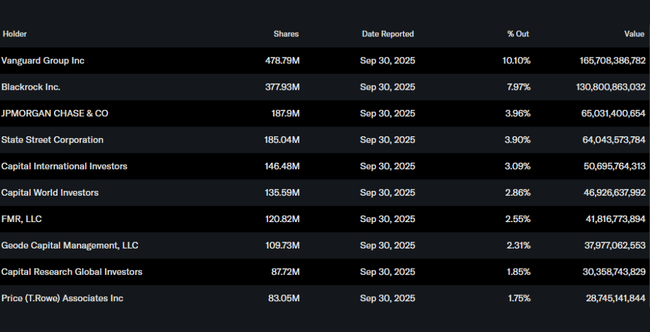

Broadcom has a strongly institutional shareholder structure. Approximately 79% of shares are held by institutions, with Vanguard Group, BlackRock, JPMorgan Chase and State Street being the largest shareholders. Insider ownership is low, which is typical for a firm of this size, and the shareholder base is predominantly comprised of long-term capital.

Analyst expectations

Analysts view Broadcom as one of the best ways to participate in the growth of AI infrastructure. The company is valued not only for its rapid growth in AI segments, but more importantly for its ability to turn that growth into high margins, strong cash flow and a growing dividend. It is this combination of growth and financial stability that makes Broadcom a title that is often ranked among the most attractive large technology stocks today.