Nike’s recent quarters sit uncomfortably between recovery and inertia. After years of rapid expansion followed by inventory excesses and shifting consumer behaviour, the company is now focused less on accelerating growth and more on rebuilding its operating foundations. The latest results suggest that revenues are holding, but that alone is not the finish line.

For investors, this phase is about credibility rather than momentum. Management is prioritising portfolio discipline, wholesale relationships, and structural fixes over short-term margin optimisation. The real question is not whether Nike can post stable sales today, but whether these choices lay the groundwork for a durable brand and earnings recovery over the next cycle.

How was the last quarter?

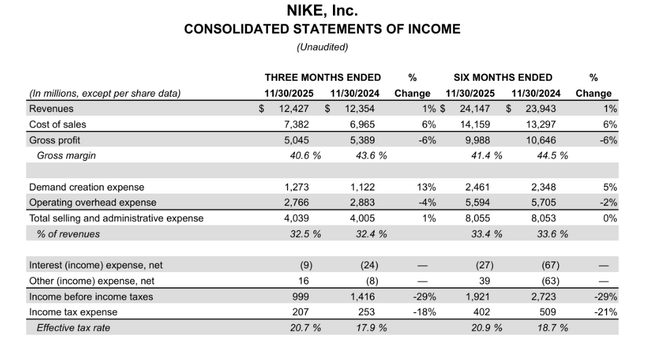

The second fiscal quarter presented a very mixed picture. The company's revenue came in at $12.4 billion, up 1% year-over-year, while adjusted for currency effects, it remained virtually flat. Thus, at the absolute revenue level, Nike $NKE was able to stabilize performance, but the growth structure reveals continued strains in the business model.

A major positive is the return to growth in the wholesale channel. Revenue from wholesale grew 8% to $7.5 billion, driven primarily by strong demand in North America and renewed collaboration with key retail partners. This shift confirms that the company is gradually correcting its previous overly aggressive bet on direct sales to end customers.

Conversely, the NIKE Direct segment remains a weak spot on the income statement. Direct sales fell 8% to $4.6 billion, with Nike's digital sales falling as much as 14%. Its own brick-and-mortar stores fared slightly better, but even here digital failed to fully offset the shortfall. This development confirms that consumers are more price sensitive and less willing to spend in premium online channels.

Converse's performance was also a significant negative factor. Its sales fell 30% year-on-year to USD 300 million, across all regions. Converse thus continues to emerge as a structural weakness in the portfolio that is not acting as a stabilizer at this stage of the cycle.

Margins, costs and profitability

Gross margin declined by a significant 300 basis points to 40.6%. The main reasons were higher tariffs in North America and a generally higher cost base associated with supply chain restructuring. This margin pressure was a key theme throughout the quarter and a major drag on a faster return to higher profitability.

Operating costs remained relatively under control. Total selling and administrative expenses increased only 1% to $4.0 billion. However, there is significant overlap within these: marketing and demand support expenses rose 13%, while overhead costs fell 4%. Thus, Nike is clearly prioritising investment in brand and sports marketing over across-the-board savings.

Net profit came in at $792 million, down 32% year-on-year. Earnings per share fell at the same rate, to $0.53. This decline is not a surprise - it is a direct result of lower margins and a conscious decision by management to sacrifice short-term profitability in favor of long-term stabilization.

Management Commentary

CEO Elliott Hill referred to fiscal 2026 as a comeback period, which aptly describes the current phase of the cycle. He said Nike is following the Win Now plan, which includes reorganizing teams, improving relationships with partners, and returning to the brand's athletic DNA. It is placing particular emphasis on the so-called sport offense - that is, product innovation geared toward specific sports and athletes, not just the lifestyle segment.

CFO Matthew Friend stressed that the company is managing the current turbulence without disrupting its financial stability. He said Nike is making the necessary shifts in its portfolio and distribution to return to full growth once the consumer environment stabilises.

Outlook

The company did not provide a detailed quantitative outlook, but management comments suggest that margins and profitability will remain under pressure in the short term. Fiscal 2026 is expected to be primarily a year of transformation, not profit maximization. Key variables will be the continued evolution of tariffs, the pace of recovery in the digital channel and the ability to restart growth in China.

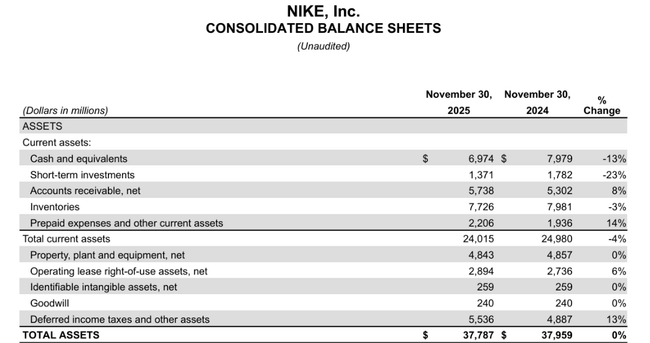

Continued inventory control, down 3% to $7.7 billion, and strong capital discipline are positive signs. Cash and short-term investments of $8.3 billion provide the company with ample room to maneuver.

Long-term results

For Nike $NKE, the long-term financials are primarily a story of a skewed cycle. After a strong post-pandemic period where the company benefited from demand acceleration, high margins and aggressive growth in the Direct channel, the last two fiscal years have seen a significant turnaround. Revenues have virtually stalled since 2023 and are already down nearly 10% year-over-year in 2025, clearly showing that the original growth model has hit its limits.

This break-even is even more pronounced at the level of operating profitability. While Nike generated an operating profit of over $6.5 billion in 2021-2022, by 2025 operating income has fallen to around $3.7 billion. This represents a decline of over 40% in three years, although absolute revenues remain well above pre-pandemic levels. Margin pressure is not coming from a single source, but from a combination of higher production costs, tariffs, inventory revaluation and, most importantly, a change in sales mix.

The experiment with the Direct-to-Consumer strategy has played a crucial role in the long-term trend. In recent years, Nike has systematically prioritised its own digital channels and limited its collaboration with wholesale partners. This approach increased margins in the short term but also weakened brand reach, reduced volumes and increased operating costs. In the long-term numbers, this has translated into stagnating sales and a significant decline in EBIT and EBITDA, which have fallen by tens of percent year-on-year in 2025.

Shareholding structure

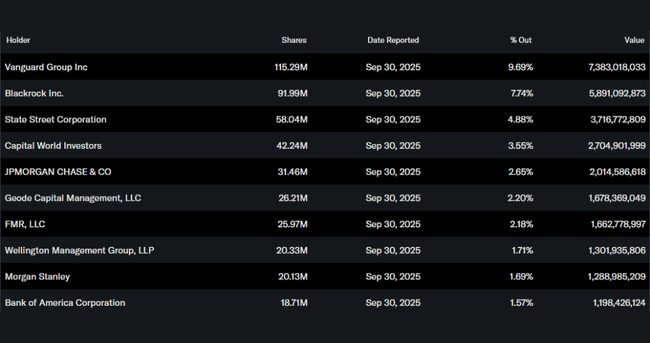

Nike remains a strongly institutionally owned company. Approximately 83% of shares are held by institutional investors, with Vanguard, BlackRock and State Street among the largest. This type of shareholder base typically implies a high emphasis on long-term strategy, cash flow stability, and disciplined capital policy, rather than short-term performance optimization.

Analyst expectations

The analyst community has a generally moderately positive to neutral outlook for Nike stock through 2026, although there is considerable uncertainty about revenue and margin growth in the near term. Consensus from multiple sources indicates that the average 12-month price target is around $77-83, with high estimates as high as $120 and low estimates as low as around $35-38, reflecting differing views among institutional analysts regarding the pace of brand recovery and pressure on profitability.