For most of the past decade, semiconductor investing has been framed as a familiar rhythm of booms and slowdowns. Capital expenditure rises, inventories build, demand cools, and the cycle resets. What has quietly changed is that parts of the chip supply chain no longer behave like cyclical suppliers, but more like structural bottlenecks. As artificial intelligence pushes logic, memory, and power efficiency to physical limits, progress is increasingly constrained not by demand, but by access to the most advanced manufacturing tools.

This is where the current phase becomes more interesting. After a cautious investment pause in 2023–2024, leading chipmakers are once again committing to long-term capacity plans. The difference this time is not scale, but precision. Growth is shifting toward fewer, far more complex systems with disproportionately high economic value. The rising weight of EUV and the early commercial rollout of next-generation lithography are changing the revenue mix, the margin profile, and ultimately the predictability of future cash flows. The underlying question is no longer whether spending returns, but whether technological exclusivity turns volatility into durability.

How was the last quarter?

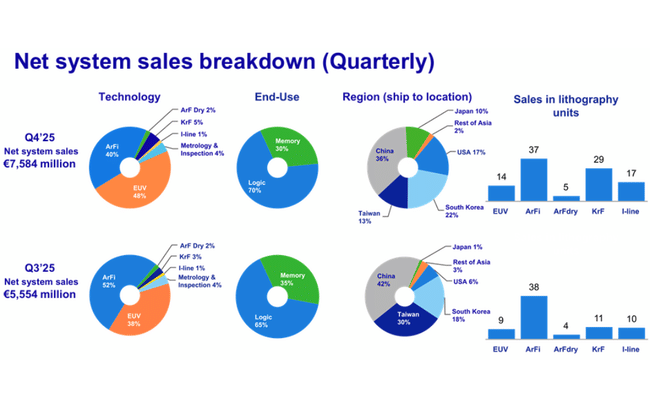

The fourth quarter of 2025 was one of the strongest quarters in the company's history for$ASML Holding $ASML and a key validation of the turnaround of the investment cycle in the semiconductor sector. Revenues of €9.7bn marked quarter-on-quarter growth of around 29% compared to Q3, when ASML reported €7.5bn. This was a significant acceleration year-on-year, driven mainly by higher shipment volumes of EUV systems and the first recognition of sales from two High NA EUV systems, which have a fundamentally higher unit value than standard EUV machines.

Gross profit in Q4 reached €5.07 billion, corresponding to a gross margin of 52.2%, close to the company's historical highs. The margin was supported by the product mix - a higher proportion of EUVs, rising service sales and improving operational efficiency in production. Installed Base Management, i.e. servicing and upgrades of already installed systems, generated €2.13 billion in the quarter, representing approximately 22% of quarterly revenues and confirming ASML's strategic shift towards more stable, recurring revenues with above average margins.

Net profit for Q4 was €2.84bn, while EPS rose to €7.35, a sequential increase of over 33%. In terms of cash position, there was a significant strengthening, with cash and short-term investments reaching €13.3bn at the end of the year, up from €5.1bn at the end of Q3, reflecting both strong profitability and the collection of high volumes of advances for new systems.

A key indicator was net new bookings, which reached €13.2 billion in Q4, one of the highest quarterly figures in the company's history. Of this amount, €7.4 billion was attributable to EUV systems, which clearly shows that investments in the most advanced manufacturing technologies are accelerating, especially in the context of AI, data centers and advanced logic chips. Total backlog grew to €38.8 billion, a level exceeding the entire year's revenue, providing exceptionally strong visibility of future earnings.

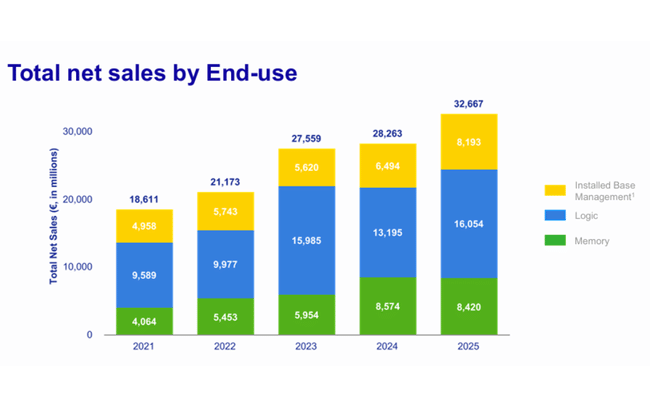

On a full-year basis, 2025 revenues reached €32.7 billion, accelerating from 2024 and confirming the return of the growth trajectory. For the full year, gross margin was 52.8%, net profit €9.6bn and EPS €24.73. Despite the lower number of systems shipped compared to 2024, the overall financial result was better thanks to a significantly higher average price of equipment sold.

Full-year results 2025

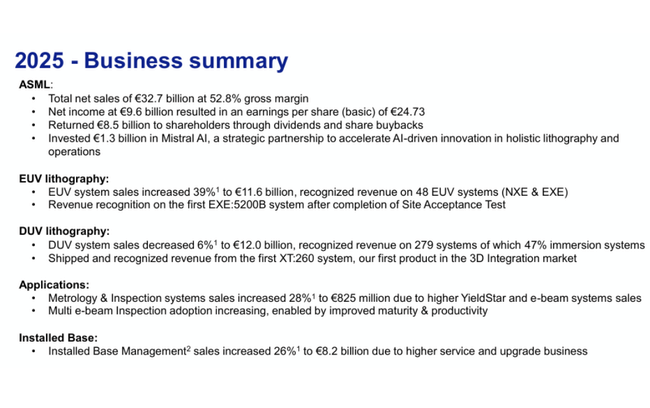

For the full year 2025, ASML reported revenues of €32.7bn, up approximately 16% year-on-year compared to 2024. Gross profit reached €17.3bn and gross margin reached 52.8%, confirming the company's ability to maintain pricing power even with high investment in development. Net profit of €9.6bn represents a slight decline from an extremely strong 2023, but remains well above 2021-2022 levels.

In terms of volumes, 300 new lithography systems were sold in 2025, fewer than in 2024, but their average value increased significantly. This confirms the strategic shift towards more technology-intensive and expensive solutions, where ASML has a virtual monopoly.

CEO comment

CEO Christophe Fouquet described 2025 as another record milestone and highlighted that the medium-term outlook for customers has visibly improved in recent months. A key factor, he said, is the sustainability of AI demand, which is leading to increased capacity plans across the industry. This shift has been directly reflected in record order intake and backlog growth.

The CEO also pointed out that ASML continues to invest heavily in people, development and manufacturing infrastructure to be able to support growth not only in 2026 but also in the years to come. In particular, the focus is on EUV and High NA technologies, which will be key for the next generation of chips.

Outlook

ASML's outlook for 2026 is one of the strongest signals that the current demand is not a short-term cyclical blip, but a structural shift in the semiconductor industry. For Q1 2026, the company expects revenues in the range of €8.2-8.9bn, which even at the low end would represent a very solid start to the year after an extremely strong Q4. Gross margin is expected to remain in the 51-53% range, suggesting that the cost pressure associated with the ramp-up of new technologies is fully offset by pricing power and product mix.

On a full year 2026 basis, management expects revenue between €34bn and €39bn, a potential year-on-year growth range of approximately 4-19% compared to 2025. The upper end of the outlook implicitly assumes a significant acceleration in EUV system shipments, further commercial expansion of High NA EUV and continued growth in Installed Base Management, which should benefit from a record installed base.

The company also anticipates high R&D investment - R&D costs of around €1.2bn per quarter- confirming that ASML is sacrificing short-term cost optimisation for long-term technology leadership. Management repeatedly emphasizes that demand for advanced lithography is increasingly driven by AI workloads that require the most advanced manufacturing nodes and high yields, where ASML has a virtual monopoly.

News and capital allocation

ASML announced a new share buyback program of up to €12 billion to be implemented by the end of 2028. The majority of the repurchased shares will be cancelled, which increases the long-term value per share. The company is also planning a total dividend for 2025 of €7.50 per share, representing 17% year-on-year growth.

In addition, management announced a reorganization of the technology and IT teams to streamline development processes and accelerate innovation in key areas. This is a move designed to foster long-term competitiveness in an environment of increasing technological complexity.

Long-term results

ASML's long-term financial development clearly shows that the company has undergone a transformation from a cyclical equipment supplier to a structural winner in the technology megatrend. Between 2021 and 2025, revenues grew from €18.6 billion to €32.7 billion, representing a cumulative growth of more than 75%. Gross profit increased from €9.8bn to €14.5bn over the same period, with gross margins holding steady above 50%, which is exceptional in a capital-intensive industry.

Operating profit has long been around €9bn per annum, even in years when there has been a slowdown in semiconductor capacity investment. Net profit has fluctuated between €5.6bn and €9.6bn, with declines in some years driven primarily by the timing of shipments rather than deteriorating fundamentals. EBITDA rose from around €7.2bn in 2021 to over €10.1bn in 2025, confirming a strong ability to generate cash even with high investment.

An important structural trend is the gradual decline in the number of shares outstanding due to share buybacks, which supports long-term EPS growth, even in periods when net income is stagnant. Installed Base Management has gone from being a complementary segment to a key stabilising element in the results, significantly reducing cash flow volatility over the cycle.

Analyst expectations and target prices

Following the release of the Q4 2025 results and updated 2026 outlook, analyst consensus remains clearly positive towards ASML, although the emphasis on valuation and high market expectations is more prevalent in commentary. Most large investment banks view ASML as a key structural winner in the AI investment cycle, with exceptional revenue visibility due to its record backlog and dominant position in EUV lithography.

Goldman Sachs

Goldman Sachs ranks ASML among its top picks in the European technology sector. Goldman is working with a target price of €1,050-1,100 per share and notes that if the upper end of its 2026 revenue guidance (€39bn) is met, ASML can generate EPS well above €30 in the coming years without margin pressure.

Morgan Stanley

Morgan Stanley also remains at an Overweight recommendation, but the tone is slightly more cautious compared to Goldman. In particular, the bank highlights the EUV mix and the ramp-up of High-NA systems, which raise the technology barrier to entry and long-term customer ROI. Morgan Stanley's target price is around €980-1,020, with analysts cautioning that the stock's near-term performance will be sensitive to the pace of backlog execution and any shifts in Foundry customers' investment plans, particularly in Asia.