Qualcomm entered fiscal 2026 with strong revenue numbers and a clear signal of a structural transformation of the business towards automotive, IoT and data centers. Record quarterly sales confirm that diversification beyond smartphones is moving in the right direction, and that demand for powerful "physical AI" chips remains robust even in a less favorable macro environment.

At the same time, however, the results reveal a weaker part of the investment story - profitability. Although non-GAAP EPS grew slightly year-over-year, net income and GAAP EPS both declined, and the outlook for the next quarter anticipates a noticeable decline in earnings due to memory constraints in the smartphone supply chain. So the market got a combination of strong headline numbers and a cautious outlook, which typically leads to a choppy stock reaction.

How was the last quarter?

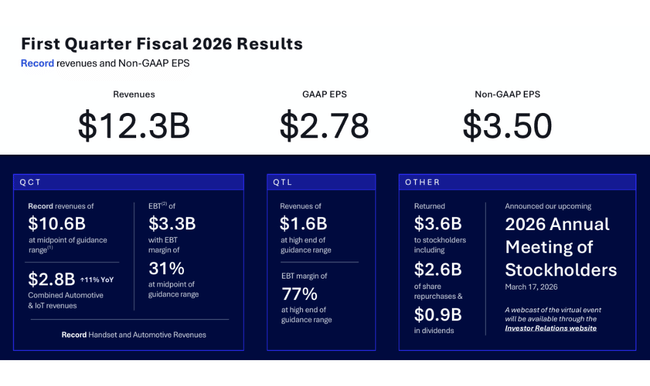

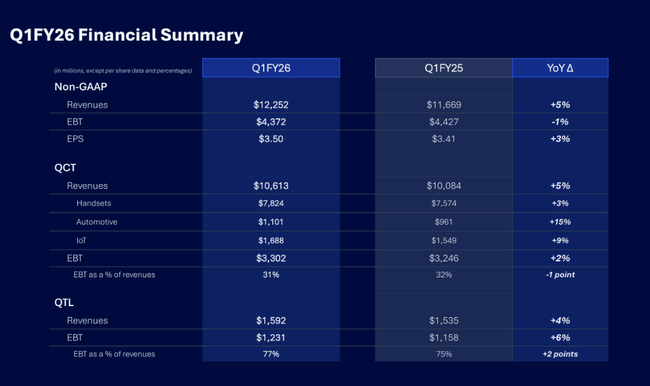

Qualcomm posted record revenue of $12.25 billion in the first fiscal quarter of 2026, up 5% year-over-year. On the surface, this is a solid result, but the structure of the growth is more important than the number itself. While revenue grew, GAAP net income fell 6% to $3.0 billion and GAAP EPS declined from $2.83 to $2.78. The non-GAAP view is slightly more favorable - adjusted EPS rose 3% to $3.50, suggesting that the pressure on profitability is largely related to one-time items and cost structure.

The QCT segment remains a key growth driver, generating $10.6 billion in revenue, or roughly 87% of the company's total revenue. QCT grew 5% year-over-year, while segment profitability remained strong, with QCT EBT margins of approximately 31%. The traditional handset business added only 3%, confirming that smartphones are no longer a growth driver, but rather a stable source of cash flow.

On the other hand, the automotive segment delivered a significantly positive surprise, with sales up 15% to USD 1.1 billion, marking the second quarter in a row that Qualcomm has surpassed the USD 1 billion mark. The IoT business added 9% to USD 1.69 billion, confirming that industrial and embedded applications are starting to play an increasingly important role. QTL's licensing division grew faster than QCT, up 6%, and its EBT margin further improved to 77%, stabilizing the group's overall profitability.

A significant signal of capital discipline is the return of cash to shareholders. Qualcomm returned $3.6 billion to investors in the quarter alone, including $2.6 billion in buybacks and nearly $1 billion in dividends, underscoring the company's strong cash-flow position.

CEO commentary

Cristiano Amon' s comments highlighted that Qualcomm is experiencing growing momentum in the personal, industrial and "physical AI" areas. He said the results are proof that the strategy of diversifying beyond smartphones is working, especially with strong traction in automotive customers and industrial applications. However, he also openly pointed to short-term issues in the handset segment, where memory constraints and related pricing pressures are hampering demand from some device makers.

The acquisition of Alphawave Semi is also an important strategic move, which Amon called an acceleration of Qualcomm's expansion into the data center space. This is a clear indication from management that the company wants to be relevant in the long-term in the AI infrastructure layer, not just on the end-device side.

Outlook

The outlook for the second fiscal quarter of 2026 is cautious and represents a major source of investor nervousness. Qualcomm expects revenue in the $10.2-11.0 billion range, a sequential decline from record Q1. QCT is expected to be in the $8.8-9.4 billion range, while QTL is expected to add $1.2-1.4 billion.

Profitability is expected to decline significantly in the short term. Non-GAAP EPS is only expected to be in the range of USD2.45-2.65, noticeably below Q1's USD3.50. Management explicitly states that this decline is due to memory constraints in the smartphone supply chain and related price and volume adjustments at key customers. On the other hand, Qualcomm confirms that long-term targets through fiscal 2029 remain unchanged, suggesting that management views the current weakness as temporary.

Long-term results

A look at the last four fiscal years shows that Qualcomm is going through a significantly cyclical period, but at the same time is able to quickly restore growth. After a record year in 2022, when revenues reached about $44.2 billion, came a sharp decline to $35.8 billion in 2023, driven by a global downturn in demand for consumer electronics and a correction in handset segment inventories.

The year 2024 marked a turnaround, with sales rising to US$39.0 billion, and in 2025 Qualcomm accelerated growth again to US$44.3 billion, a near return to all-time highs. Importantly, growth is no longer driven solely by smartphones, but increasingly by automotive and IoT, which are less cyclical and have longer contract visibility.

Profitability is more volatile. Net profit in 2025 has fallen to $5.5 billion, down significantly from $10.1 billion in 2024. However, this decline is largely due to the extreme increase in tax burden, not the collapse of the operating business. In contrast, operating profit is up 23% to US$12.4 billion in 2025, confirming that the core business remains strong.

The continuous decline in the number of shares outstanding is also a positive long-term trend, supporting EPS in growth years and dampening its decline in leaner years. EBITDA increased to $14.9 billion in 2025, indicating solid cash-flow generation even in a less favorable fiscal year.

News

The most significant strategic news of the quarter was the completion of the Alphawave Semi acquisition, which strengthens Qualcomm's position in high-speed interfaces and data centers. This transaction clearly fits in with the company's efforts to expand its footprint in AI infrastructure and reduce reliance on the handset cycle.

Another important point is the record performance of the automotive segment, where Qualcomm further consolidates its position as a key supplier of chips for infotainment, ADAS and connectivity. It is this segment that is often seen by investors as a long-term valuation stabilizer.

Shareholding structure

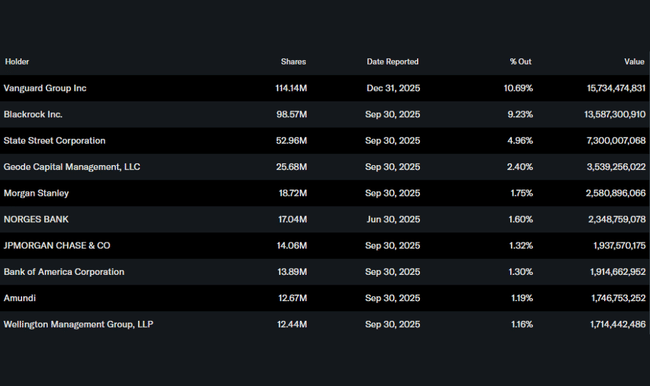

Qualcomm has a very stable institutional base. Approximately 82% of shares are held by institutional investors, with Vanguard, BlackRock and State Street being the largest shareholders. The low insider stake confirms that the title is primarily held by long-term funds, which typically reduces extreme volatility but also implies sensitivity to changes in the outlook.

Analyst expectations

Analysts agree in their assessment that the short-term outlook is weaker, but the long-term story remains attractive. For example, investment bank JPMorgan maintains an Overweight recommendation on the stock, arguing that the current pressure on EPS is temporary and that automotive and AI infrastructure will be key growth pillars in the coming years.