Adobe opened fiscal 2026 with record first quarter results. Revenue grew around low double digits to about 6.4 billion dollars, subscription revenue rose 13 percent and AI first annual recurring revenue more than tripled compared with a year earlier. Operating cash flow reached a record 2.96 billion dollars in the quarter, underlining how the subscription model and new AI tools across Creative Cloud, Document Cloud and Experience Cloud are already translating into hard cash, not jen marketingový příběh.

For investors, Adobe still looks like a growth stock with high profitability, not a mature software name living off its legacy base. The key question over the next few years is whether the company can keep AI related revenue growing at a double digit pace while it integrates the planned Semrush acquisition, a roughly 1.9 billion dollar cash deal aimed at strengthening its marketing and data capabilities, without putting sustained pressure on margins.

How was Q1 2026?

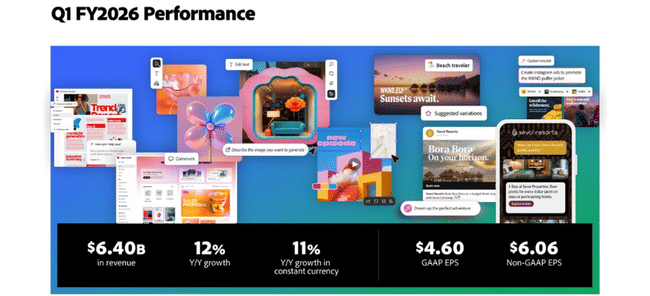

The quarter brought in record revenues of $6.40 billion, up approximately twelve percent year-over-year. Of that, subscriptions accounted for $6.20 billion and grew roughly thirteen percent, while traditional license and service sales remain a small and stagnant part of the business. The company explicitly states that subscription revenues associated with AI-first ARR ("AI-first ARR") features more than tripled year-over-year, showing that customers are actually adopting the news and it is not just a marketing sticker.

Total annual recurring revenue (ARR) reached $26.06 billion at the end of the quarter, a year-over-year growth of approximately 11 percent. In terms of segments, both creative and marketing professionals (around $4.39 billion in subscriptions, up about twelve percent) and "regular" individual and small business users (around $1.78 billion, up about sixteen percent) are doing well. This confirms that Adobe can grow across the customer spectrum - from large marketing teams to freelance content creators.

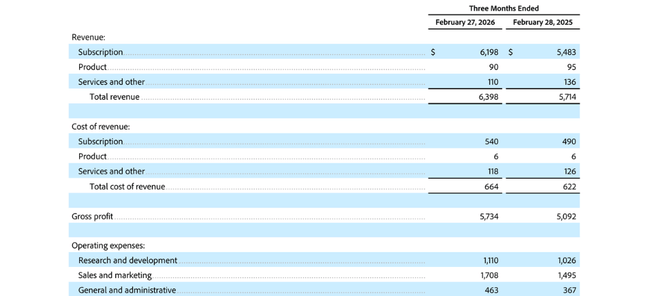

Gross profit in the quarter was about $5.73 billion on cost of sales of about $664 million, which implies very high gross margins typical of software. GAAP operating profit was about $2.42 billion, adjusted operating profit was $3.04 billion, which equates to an adjusted operating margin of about 47 percent. GAAP net income was about $1.89 billion, adjusted net income was $2.49 billion; GAAP earnings per share were about $4.60, adjusted about $6.06.

The highlight is the record operating cash flow of $2.96 billion in the first quarter. This shows that accounting profits are not "paper" - customers are actually paying and subscriptions are generating steady cash. The backlog of future contracts (remaining performance obligations, RPOs) was about $22.22 billion, about two-thirds of which is for the next twelve months. Adobe thus has high visibility of future earnings, which is important for long-term investors in assessing risk.

The balance sheet remains robust: cash and short-term investments exceed $6.8 billion, with total debt obligations of around $6.2 billion. The company repurchased roughly 8.1 million of its own shares during the quarter, which at an average diluted share count of around 411 million represents a noticeable boost to earnings per share and a signal of management's confidence in its own valuation.

Management commentary

Commenting on the results, the company's chief executive Shantanu Narayen highlighted that Adobe had a record quarter and that ARR from "AI-first" products more than tripled year-on-year. He links this to the company's mission to "empower everyone to create" - in an era of artificial intelligence where content is behind much of the digital experience, Adobe sees an even bigger addressable market than before. The tone is clearly confident: executives are keen to show that they have a head start in generative AI and creative tools, and that AI is not a threat, but the next wave of growth.

CFO Dan Durn highlighted thirteen percent subscription growth and record cash flow, and stressed that the acceleration of AI features across creative, productivity and customer products is set to support "continued profitable growth". Between the lines, he tells investors that Adobe doesn't want to sacrifice margins in the name of growth - AI is meant to enhance the value of products and enable higher prices or broader usage, rather than just drive up costs.

Outlook

For the second quarter of fiscal year 2026, Adobe is targeting revenue of around $6.43-6.48 billion, again double-digit year-over-year growth. Subscriptions for the general user and smaller business segment are expected to be around $1.80-1.82 billion, and for creative and marketing professionals around $4.41-4.44 billion. Management expects an adjusted operating margin of about 44.5 percent, a GAAP tax rate of about 22.5 percent and an adjusted tax rate of about 18 percent, with a diluted share count of about 402 million.

GAAP earnings per share are expected to be around $4.35-4.40, with adjusted earnings per share expected to be around $5.80-5.85. These targets do not take into account the impact of the planned acquisition of Semrush, which is still in the approval process - meaning that any synergies will be reflected later. Overall, the outlook looks rather optimistic, but not overly aggressive: Adobe is on pace for double-digit revenue growth while planning to maintain very high margins.

Long-term results

Over the past four full fiscal years, Adobe's $ADBE revenue has grown from roughly $17.6 billion to $23.8 billion, always at a rate of around ten to eleven percent per year. Gross profit has increased from about $15.4 billion to $21.1 billion, while cost of sales has grown more slowly than revenue - a testament to the high scalability of the software model.

Operating costs (R&D, sales and marketing, administration) have been around $9-12.5 billion per year in recent years. In 2025, they remained almost unchanged at around $12.4 billion, while revenue and gross profit continued to grow, leading to a significant boost in operating profit to almost $8.7 billion - up roughly thirty percent year-on-year.

Net income increased from about $4.8 billion a few years ago to about $7.1 billion in the most recent fiscal year, while earnings per share rose from about $10.1 to $16.7. Part of that growth came from share repurchases: the average diluted number of shares fell from roughly 471 million to about 427 million. The combination of profitability growth and gradual share count reduction is very favorable for the long-term investor.

At the EBITDA level, results have moved from around $7.1 billion to $9.7 billion, while margins remain very high. Thus, Adobe has long shown steady double-digit revenue growth, even faster earnings growth and strong cash flow, a pattern typical of dominant software platforms with a high proportion of recurring revenue.

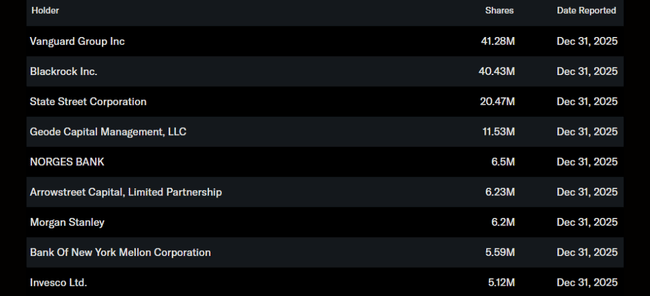

Shareholding structure

Insiders hold only a very small share of the stock (on the order of a few tenths of a percent), while institutions own approximately 85-88 percent of the shares, with retail investors accounting for the remainder. The largest institutional shareholders are the Vanguard Group with a stake of just over 10 percent, BlackRock with around 9-10 percent, State Street with around five percent, and Geode Capital with around three percent; the remainder is made up of a wide range of funds and pension investors.

This structure means that Adobe stock is firmly embedded in index and broad technology funds, and its movement is strongly linked to overall sentiment in the US technology scene. A small insider stake may raise questions about "skin in the game", but on the other hand, a high institutional stake promotes liquidity and stability, as large funds typically react to results and the outlook with gradual rather than panic selling.