Procter & Gamble confirmed its role as a defensive portfolio anchor in the third fiscal quarter of 2026. Revenue grew 7% to $21.2 billion, with organic sales up 3%, driven by 2% volume growth and a 1% contribution from higher prices. Diluted EPS rose 6% to $1.63, but part of this growth is a one-time gain from the termination of the Glad joint venture; core EPS, which better captures operating performance, rose 3% to $1.59.

The company generated $4 billion of operating cash flow and adjusted FCF productivity was 82%. It returned $3.2 billion to shareholders in the quarter - $2.5 billion in dividends and over $600 million in cash distributions. USD 600 million in buybacks. P&G also announced another dividend increase, its 70th in a row, maintaining an unbroken streak of payouts dating back to 1890.

Q3 2026 results: growth, but no "wow" effect

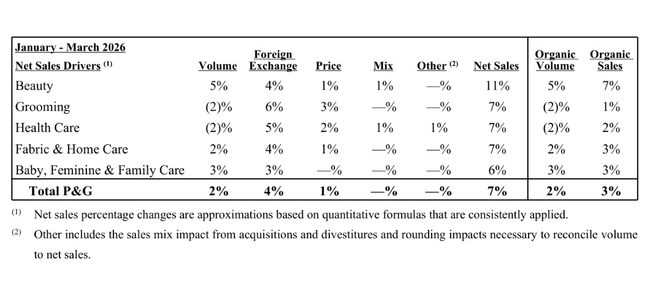

Net sales came in at $21.2 billion, up 7% year-on-year. Organic growth of 3% is a combination of 2% volume growth and 1% price contribution; currency effects and M&A added the rest to the overall number. Mix had a neutral impact on sales in the quarter.

Key Q3 2026 numbers

Revenue: $21.2 billion (+7% YoY)

Organic revenue growth: +3% (volumes +2%, prices +1%)

Diluted EPS: $1.63 (+6%, impact of one-time Glad gain)

Core EPS: $1.59 (+3%)

Operating cash flow: USD 4.0 billion

Adjusted FCF productivity: 82%

Q3 ROE: $3.2 billion ($2.5 billion dividend, >$0.6 billion buyback)

How the segments performed

Beauty - The segment's organic sales grew 7%. In hair care, sales grew in the mid-single digit range due to higher volumes and innovation enabled by higher prices in North America and Europe. In personal care and skin care, sales grew in the upper single-digit range, driven by a more premium mix and volume growth; partially dampened by higher promotional investments in China.

Grooming (shaving, men's grooming) - Organic growth of just 1%. Higher prices and new products in the US and Europe failed to fully offset volume declines. This is a mature segment that generates cash but is not a major growth driver.

Health Care - Organic sales grew 2%. In Oral Care, sales grew at a low single-digit rate due to higher prices and more premium products in North America, but volumes were weakened by China. Personal Healthcare also saw low single-digit growth, driven by pricing and mix, but with volumes declining in the US and Europe.

Fabric & Home Care (laundry, household) - The segment grew organic sales by 3%. In detergents, sales grew at a low single-digit rate, mainly driven by volume growth in North America. In Home Care (Cleaners, Janitorial), growth was in the mid-single digit range due to higher volumes in Europe and higher prices, mainly in Europe and the US.

Baby, Feminine & Family Care (diapers, feminine hygiene, paper products) - The segment grew organically by 3%. Baby Care grew in the low single digits due to volumes in India, the Middle East, Africa and China. Feminine hygiene also grew low single digits - higher prices and a better regional mix hit volumes. Family Care (paper products) grew in the mid-single-digit range, mainly due to restocking at retailers after last year's reductions; partly dampened by higher promotions.

Margins: productivity hits mix, duties and reinvestment

At first glance, margins look weaker than last year. GAAP gross margin was down 1.5 percentage points year-over-year, with adjusted (core) gross margin down 1 point. The main reasons: a worse sales mix (-1.8ppt), higher marketing and brand investments (-1.0ppt), increased costs from tariffs (-0.5ppt) and slightly worse commodities.

Productivity savings (+2.1 pps) and the net price effect (+0.5 pps) are mainly positive. This means that P&G is very efficient internally, but is largely "burning" the money saved to fight for customers and to offset external cost pressures.

Operating margins tell a similar story. The core operating margin has narrowed by 0.8 percentage points year-on-year, although it includes 3.3 percentage points of productivity savings. Some of the savings will be reflected in lower cost of sales, but some is being consciously ploughed back by management into greater investment - particularly in innovation, marketing and brand support in an environment where consumers are more price sensitive after a period of high inflation.

Management comment: "sales acceleration, environmental pressure"

New CEO Shailesh Jejurikar described the results as a "solid acceleration in revenue growth across categories and regions". He said all ten major product categories and all regions grew in the quarter: key markets ("Focus markets") grew 3% and emerging markets ("Enterprise markets") grew 5%.

At the same time, he freely admitted that the environment remains challenging - geopolitically and for consumers. The company is therefore increasing investment in innovation and brand support to maintain momentum and share with customers, although this is putting pressure on margins in the short term. Still, P&G is keeping full-year guidance unchanged, which is interpreted as a signal of some confidence in its ability to manage cost pressures.

Jejurikar also stresses a long-term strategy of "integrated growth", a combination of: strong brands, innovation, productivity improvements and disciplined capital management. The goal is to build the "CPG company of the future" - i.e., classic consumer goods, but with greater efficiency and better use of data.

News

Several important points emerge from the press release and investor blog:

P&G emphasizes that all categories and all regions grew in the quarter - this is a "broad-based" acceleration, not a one-time anomaly in one segment.

The company is stepping up investment in innovation and demand creation to maintain momentum after a series of years where growth was mainly driven by price increases.

It reaffirms its long-term focus on productivity - savings in manufacturing and logistics should free up space for investment in brands without significantly worsening the debt profile or dividend payout ratio.

It is therefore not a fundamental reversal of strategy, but a continuation of the course set: gradually raise volumes, maintain price levels, continue to save internally and return some of the savings to the business.

Outlook for the full fiscal year 2026

P&G $PG is keeping its full-year outlook unchanged:

Total revenue should grow by 1-5%

Organic sales to be between "roughly flat" and +4%

Diluted earnings per share to grow 1-6%

Core EPS to be between "flat" and +4% versus last year's $6.83 per share, in the range of $6.83-7.09

But at the same time, the firm cautions that it expects EPS to be more near the lower end of that range due to a combination of more expensive commodities, higher tariffs, slightly worse interest costs and a higher effective tax rate. These factors, in aggregate, should detract roughly USD 0.25 per share.

Capex should remain at 4-5% of sales, adjusted FCF productivity should be 85-90%, dividend around $10 billion and buybacks around $5 billion for the full year.

Shareholders

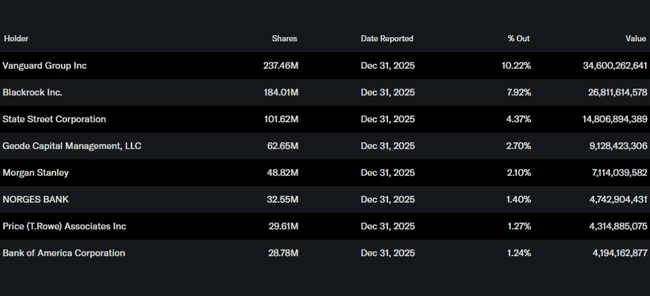

The shareholder structure is typical of a "core blue chip": around 70% of the free float is held by institutions such as Vanguard, BlackRock, State Street or Geode Capital. The combination of a stable business, a long dividend history and high earnings-to-cash conversion makes P&G a title that makes sense as a defensive portfolio component - but only if investors buy it knowing that they are buying stability and a dividend above all, not dynamic growth.