Realty Income entered 2026 very briskly: net income per share rose to $0.33, core AFFO per share rose 6.6% to $1.13, and the company invested $2.8 billion during the first quarter ($2.62 billion according to its Pro-Rata stake) with an initial cash yield of around 7.1%. The portfolio is doing well - occupancy remains at 98.9%, with releases achieving Realty Income rent recapture of 103.4% and Same Store Rental Revenue up 0.8%.

This alone would be enough for a "solid dividend quarter", but what's more important is what's happening at the capital structure and growth model level. The company is ramping up its private equity platform: it has partnerships with Apollo and GIC, has closed a $1 billion JV investment with Apollo on 492 retail properties, has raised its 2026 investment target from $8.0 billion to $9.5 billion, and has moved this year's AFFO per share estimate into the $4.41-4.44 range (3.0%-3.7% growth). For the dividend investor, this is a clear signal that Realty Income is looking to leverage its size to take an even cheaper and bigger shot at interesting net lease opportunities across the US and Europe.

Q1 2026 results: AFFO, FFO, earnings and dividends

For Q1 2026, Realty Income $O earned $1.55 billion, up from $1.38 billion a year ago (up roughly 12%). Net income for shareholders was $311.8 million, or $0.33 per share, versus $0.28 in the same period in 2025. FFO per share was $1.06, Normalized FFO was $1.07 and AFFO per share was $1.13, with AFFO up 6.6% year-over-year (from $1.06). AFFO is a key metric for REITs like Realty Income because it shows the ability to safely cover dividends and fund growth.

Meanwhile, the dividend continues to grow at its "monthly" pace: for Q1 2026, the company reported its 114th consecutive quarterly dividend increase (and 134th since 1994), with an annualized amount of $3.246 per share. Monthly dividends paid were $0.810 per share in the quarter, up 1.8% from $0.796 in Q1 2025, and represent roughly 71.7% of AFFO per share - so the payout ratio remains comfortable, with room for further growth.

Portfolio and operations

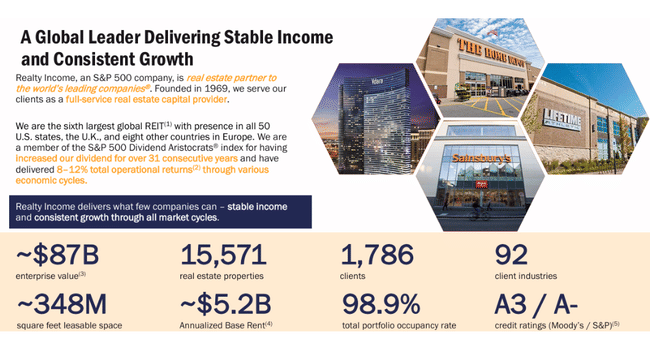

Realty Income $O owned or had interests in 15,571 properties with 1,786 tenants in 92 sectors as of the end of March 2026, with an average remaining lease term of about 8.7 years. Portfolio occupancy was 98.9%, the same as at the end of 2025 and above the Q1 2025 level of 98.5%, with only 172 properties vacant or for sale.

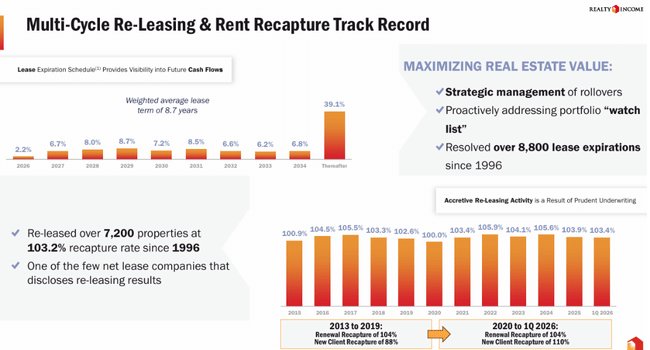

During the quarter, expirations included 320 leases; 220 units were re-leased to the original tenant, 23 to a new tenant and 78 properties were sold vacant. New annual rents on the re-leased units were $73.3 million compared to the previous $70.9 million, a rent recapture of 103.4% - so Realty Income is not only maintaining but slightly increasing rents on the re-leased properties.

Same Store Rental Revenue, calculated on 14,738 properties at constant currency, increased 0.8% ($1.193 vs. $1.183 billion). This is a "normal" rate for a REIT of this type; the main growth in AFFO comes from the spread between cost of capital and new investment income, not from rent growth on the existing portfolio.

Investment and Growth: US, Europe, Partnerships

Q1 2026 was busy in terms of capital allocation. Realty Income invested a total of $2.77 billion ($2.62 billion on a Pro-Rata basis) with an initial average cash yield of 7.1% and a weighted average lease term of around 6.5 years.

Investment Structure:

Real estate acquisitions of $1.58 billion ($1.43 billion Pro-Rata) with an initial cash yield of 6.7% and a weighted average lease term of 8.3 years.

Development projects $155.8 million ($155.2 million Pro-Rata) with an initial cash yield of 7.4% and an average lease term of 12.4 years.

Other investments (loans and construction financing) $1.03 billion (all Pro-Rata) with a cash yield of 7.8% and an average term of 3.5 years.

About 64% of new tenants by Cash Income are retail, 34% industrial and 2.5% other types, with about 41% of new tenants qualifying as investment grade. Geographically, $1.33 billion was invested in the U.S. (cash yield 7.3%) and $1.29 billion in Europe (7.0%), where Realty Income continues to expand its presence.

The big news is a $1 billion strategic investment from Apollo - for a 49% stake in a newly formed joint venture with a portfolio of 492 retail properties. Add to this the previously announced partnership with GIC and Core Plus Fund in the US, which saw third-party capital raised during the quarter and a reduction in Realty Income's ownership stake to 38.5% (as of January) and then 26.8% (as of April 2026). In practice, this means the firm is retaining a portion of the real estate economy but increasingly financing growth through outside investor capital.

Capital, debt and liquidity

Realty Income maintains very solid liquidity - as of March 31, 2026, the firm had about $3.9 billion of available liquidity on a Pro-Rata basis: $388 million in cash, $2.71 billion of undrawn capacity on revolving credit facilities, and $1.22 billion from open but pending ATM forward stock sales, net of $415 million of commercial paper.

In April 2026, the firm issued $800 million of senior unsecured notes with a 4.75% coupon due 2033; using a $500 million cross-currency swap, it converted a portion of the proceeds into euros, achieving an effective euro yield of about 4.07% and a coupon of 3.81%. On a combined basis, this translates to a roughly 4.16% coupon and 4.44% effective YTM, which at 7.1% cash yield on new investments is still a decent spread.

In March 2026 Realty Income also secured a $693.9 million unsecured term loan due 2036 at a fixed rate of 4.91% and again rolled a portion into euros via swap, so the blended borrowing rate is about 4.34%.

CEO comment

Sumit Roy frames the results as an endorsement of the "strength and resilience of Realty Income's global investment and operating platform". His emphasis is less on the quarterly numbers themselves and more on strategy: the aim is to diversify sources of permanent capital away from the public equity markets through private structures - funds, joint-ventures and platforms such as Managed Insurance and Retirement Annuity.

According to Roy, it is the partnerships with Apollo and GIC, along with the $1.7 billion of "cornerstone" capital for the U.S. Core Plus fund, that represent a fundamental shift in how Realty Income finances growth. It allows the firm to scale investment activity with the support of "deep and stable pockets of capital," increasing returns for existing shareholders and expanding the range of net lease opportunities it can tap - both in the U.S. and in Europe and other regions.

The 2026 outlook and why the stock may be under pressure despite decent numbers

Realty Income raised its 2026 investment volume guidance to $9.5 billion (from $8 billion) and also raised its AFFO per share range to $4.41-4.44 (from $4.38-4.42), implying AFFO per share growth of approximately 3.0%-3.7% this year. Same store rent growth is expected to be 1.0-1.3%, occupancy is expected to remain around 98.5%, cash G&A is expected to be 20-23 bps of gross asset value and property expenses around 1.5% of revenue.

From a stock perspective, it's a typical "steady but not rocketing" dividend growth picture: AFFO is growing in low units, the dividend is roughly 3-4% per year, safety is high, but you don't expect any dramatic growth jump. So in a higher rate environment, where the market sometimes pushes REITs down for comparisons to bonds, even a very solid report can lead to a tepid or mixed price reaction - especially if some investors were hoping for a higher rate of AFFO per share growth.