AMD is pushing “AI PCs” beyond laptops and into desktop machines. At MWC it introduced Ryzen AI 400 and Ryzen AI PRO 400 for desktops, aimed at Copilot+ PCs. The chips combine Zen 5 CPU cores, RDNA 3.5 graphics, and an NPU rated up to 50 TOPS, so more AI tasks can run locally on the device.

At the same time, AMD is strengthening its data-center angle. Meta signed a large deal for up to 6 GW of Instinct GPUs, with first deliveries planned for the second half of 2026. For investors, the interesting part is the link between these two tracks: premium AI PCs for steadier client revenue, and hyperscaler GPUs for share gains in a market long dominated by Nvidia. The near-term risk is execution and timing—how fast OEM volumes ramp on desktop AI PCs, and how smoothly AMD delivers multiple large AI projects.

Ryzen AI 400: AI on the desktop

The new Ryzen AI 400 and Ryzen AI PRO 400 for the desktop build on a combination of Zen 5 cores, RDNA 3.5 integrated graphics and second-generation XDNA 2 NPUs with up to 50 TOPS, designed to run assistants, AI applications and language models locally. $AMD is targeting users to run more demanding AI tasks - from design and engineering applications to generative functions and locally running LLM - without relying on the cloud, which has both privacy and latency implications. For the PRO segment, it adds enterprise management and security features so corporations can standardize on a fleet-enabled AI desktop platform.

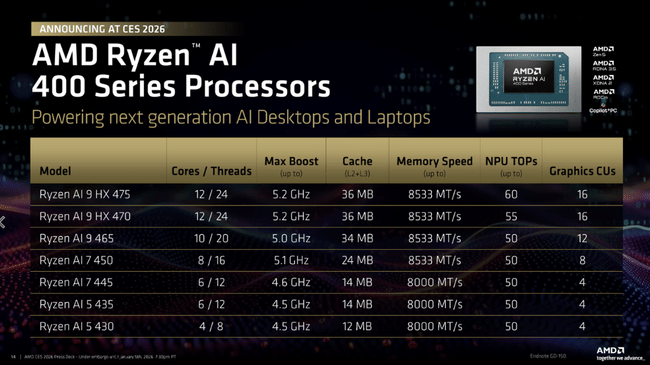

The portfolio includes six desktop models, with an 8-core Ryzen AI 7 450G/450GE configuration (16 threads, up to 5.1GHz, 8 CU Radeon 860M) and two 6-core Ryzen AI 5 models with Radeon 840M, available in 65W and 35W variants. Compared to the Ryzen 9000 with pure Zen 5 cores, the Ryzen AI 400 have a weaker CPU part due to the use of Zen 5c, but better integrated graphics and more importantly NPUs - so it is a different type of product than pure gaming or performance CPUs. AMD states in the press release that AM5 desktop systems with Ryzen AI 400 will be available from Q2 2026 from major OEMs like HP $HPQ, Lenovo $LNVGY and Dell $DELL, which gives a good signal that this will not be a fringe lineup.

AI PCs as a new category, and where AMD is in it

The Ryzen AI 400s are the first desktop processors for so-called Copilot+ PCs, machines designed to handle much of the AI functionality of Windows and applications directly on the device. Microsoft's $MSFT has set a minimum NPU performance requirement for Copilot+, and with 50 TOPS, AMD is putting itself at the parametric base of the future AI PC standard. This creates both a simple marketing story for OEMs ("AI PC") and a technical framework that favors chips with NPUs - conventional CPUs without a dedicated accelerator take a back seat in the premium segment.

Historically, AMD has often been perceived as the choice for performance/price or gaming machines in the desktop segment, while the professional and enterprise segment has been more strongly associated with Intel $INTC. Ryzen AI PRO 400 may disrupt this pattern by offering businesses a combination of local AI, integrated graphics for the regular office, and remote management in a single package. If AI features in mainstream work tools (Office, CAD, creative software) become standard, AMD may move higher up the value chain - from a pure "performance" option to the "preferred base" for AI workstations.

Meta, 6 gigawatts and AI in data centers

But the desktop isn't the only area where AMD is making strides in AI. Late February brought the announcement of an expanded strategic partnership with Meta Platforms to deploy up to 6 gigawatts of AI infrastructure based on Instinct GPUs and Helios servers. The first gigawatt is scheduled to ship in the second half of 2026 and will leverage custom GPUs on the MI450 architecture and the sixth generation of EPYC "Venice" server processors. This diversifies Meta's suppliers beyond Nvidia and gives AMD long-term visible volumes in a segment where it otherwise competes piece by piece.

Market analyses point out that AMD's AI business rests on two pillars: data centers and client devices. On the server side, the MI400/MI450 is meant to address rapidly growing inference and training, with companies like Meta, Microsoft and other hyperscale players looking for a second vendor alongside Nvidia. On the client side, the Ryzen AI 300/400 are intended to bring AI capabilities directly to PCs and mobile workstations - creating a base on which to push software licenses and services. If the two segments can be rolled out in parallel, it could bring AMD's revenue structure closer to a diversified AI player, not just an "outsider" fighting for share.

Risks and potential impacts

The short-term risk is primarily how fast the AI PC category will realistically take off and what the specific orders from OEM partners will be in Q2 and Q3. If demand remains more of a marketing wave than a real need to upgrade for AI, Ryzen AI 400 growth may be slower than PR suggests. Another near-term risk is technological: AMD needs to deliver stable drivers, software support, and optimizations for key AI applications, or the NPU advantage will turn into a paper parameter.

In the medium term, the execution of large AI contracts plays a big role. The 6 GW Instinct GPU deal with Meta is capital intensive and runs across multiple product generations; any slippage in MI450 or EPYC "Venice" production could shift revenue recognition and increase costs. At the same time, competition from Nvidia $NVDA and other players means that AMD cannot build on a high price premium, but rather on the performance/price combination, which may limit margin expansion. Moreover, in the PC segment, AMD is competing with both Intel and a new generation of chips from other NPU-focused manufacturers, so maintaining share will require a rapid iteration of the product roadmap.

In the long term, the binary risk is whether AI PCs will actually become the standard or remain a relatively narrow category of more expensive devices. If mass deployment of "Copilot+" and similar platforms is delayed, AMD would have to rely more on data centers and servers, where it has a smaller ecosystem and less power compared to Nvidia. Another binary element is large cloud contracts: if a major partner (typically Meta) were to significantly reduce or shift the contract to its own ASIC solutions, this would directly hit expected growth. Export regulation of advanced chips and geopolitical risks are also a factor that may have an "on/off" effect on part of the market, especially in China and other sensitive regions.

What to watch next

In the coming months, the key will be what specific models of AI desktops and workstations with Ryzen AI 400 will be announced by HP, Lenovo and Dell and at what price levels they will be available. Also to watch closely are the metrics listed for AMD's next quarterly results: revenue growth in the client chip segment, AI processor share of the mix, and gross margin trends. On the data center side, how Instinct GPU orders develop, confirmation of other large contracts post-Meta, and market awareness of the MI400/MI450 ramp-up will be important. Signals from Microsoft and other software partners on whether they are optimizing their AI features primarily for NPU platforms and how AMD figures in these integrations will also be significant.

Conclusion

A key variable in AMD's story in 2026 becomes the ability to turn its technical lead in NPUs into a true AI PC standard while delivering large AI contracts in data centers without major hitches. If AI PCs take off according to the OEM's roadmap and the Meta contract translates into visible growth in the server business, the current "AMD as a second source in AI" thesis may shift towards a role as a structural co-leader; the tipping point would come when AI PCs turn out to be a narrow segment and AI servers remain in the hands of one dominant rival, reopening the question of how much of today's "AI premium" in AMD's valuation is actually justified.