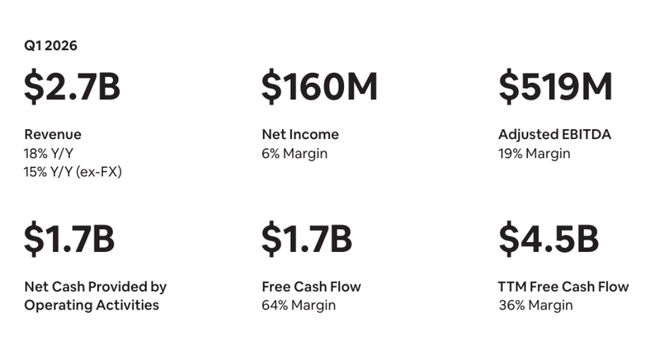

Airbnb started 2026 exactly as the market wanted: revenue grew 18% to $2.7 billion, Gross Booking Value grew 19% to $29.2 billion and Nights and Seats Booked increased 9% despite higher cancellations due to the situation in the Middle East. Net profit was $160 million (net margin 6%), Adjusted EBITDA jumped to $519 million (margin 19%) and free cash flow of $1.7 billion implies an incredible FCF margin of 64% in the quarter and 36% on a trailing 12 month basis ($4.5 billion).

More importantly, the company is seeing acceleration where it needs it: nights booked on the app are up 22% and already account for 63% of all stays, first bookable guests have added 10% (the most since early 2022), and developing markets like India and Brazil are growing twice as fast as the core business.

Q1 2026 results: revenue, profit and cash flow growth

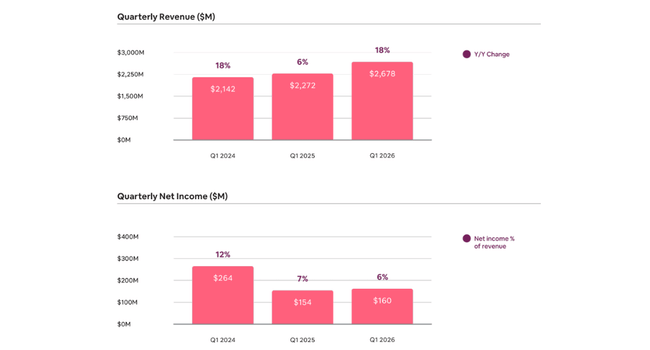

Revenues of $2.7bn imply 18% year-on-year growth (15% at constant currency) and are above the top end of the original range the company was counting on after Q4. The driver is a combination of volume growth (Nights and Seats +9%) and higher average pricing (ADR $187, +9% y/y), with about half of the ADR growth driven by the FX effect and the other by net higher pricing across regions.

Net income of $160m is slightly above last year, and the 6% margin reflects a mix of one-off items: the positive is a c.$70m gain on the sale of a stake in a private company, and the negative is a c.$70m reduction in deferred tax assets due to changes in U.S. Corporate AMT. Adjusted EBITDA of 519mn (+24% y/y) implies margin improvement to 19% from 18%, even as the company continues to invest in marketing and growth.

The free cash flow of $1.7 billion in the quarter (64% margin) is partly due to seasonality - Airbnb traditionally collects cash upfront, and revenue and expenses are spread out over the next few months - but it's still an important signal to investors: the business is generating cash in bulk, which creates room for buybacks, AI investments, and potential M&A. On a TTM basis, FCF is $4.5 billion (36% margin), making Airbnb one of the most "cash rich" platforms in travel.

Business dynamics: GBV, nights, app and geographic mixes

Gross Booking Value of $29.2 billion is growing at 19% (13% ex-FX). Without the impact of the Middle East conflict, Nights and Seats Booked growth would have been around 10% instead of 9%, a slight acceleration from last year.

Structure is important:

Nights via app +22% y/y, 63% of all nights (58% a year ago)

first-time bookers +10% (highest since early 2022)

Expansion markets (Brazil, India, others) growing origin nights at roughly double the rate of core markets

Regionally:

North America: high-single digit nights growth, ADR +7% (mix towards shorter stays, whole houses and larger capacity)

EMEA: mid-single digit growth in nights, ADR +15% (4% ex-FX), slightly higher cancellations due to Middle East

Latin America: high-teens nights growth, ADR +10% (3% ex-FX), Brazil origin nights >20% for third consecutive quarter

Asia-Pacific: high-teens growth in nights, ADR +6% (2% ex-FX), India origin nights +50% for second consecutive quarter, first-time bookers +75%.

Implied take rate (revenue/GBV) is 9.2%, virtually the same as 9.3% a year ago. The take rate is impacted by both FX and the rollout of "Reserve Now, Pay Later", which shifts the timing between booking and actual stay, thus accounting for revenue vs. GBV.

Product, service and AI: why growth is not just about price

Airbnb $ABNB is clearly benefiting from that:

Reserve Now, Pay Later now accounts for about 20% of global GBV - guests are booking more and longer in advance when they don't have to pay everything right away.

"Reserve Now, Pay Later" is also shifting the mix towards higher ADRs and longer stays, which is driving GBV and revenue growth.

On the guest side, the company is simplifying pricing tools (dynamic pricing based on demand and seasonality) and onboarding for new hosts - the goal is to grow supply faster in locations where there is demand. On the supply side, it is also adding services and experiences: pilots of the new "Services" and Experiences show that roughly a quarter of new guests who start with an experience make a booking for a property or service within 90 days. This makes these products a ramp-up channel to the core of the platform.

At the same time, Airbnb is adding hotels: the boutique and independent hotel pilot is expanding into other markets, especially where the supply of homes is limited by regulation or high demand. An important detail: approximately 55% of guests who book a hotel on Airbnb return within a year and book a house. This means that hotels are not "cannibalizing" but another entry point into the ecosystem.

Meanwhile, AI is becoming the essence of execution:

about 60% of the code is co-written by AI

Over 40% of customer support queries are resolved by AI without a human (vs. ~33% in Q4 2025)

cost per booking down ~10% y/y - and the company expects this trend to continue

Partnerships and big events: the Delta, the Olympics and the World Cup

Expanded partnership with Delta - guests can earn miles not only for house stays, but now also for Experiences and Services, with Experiences and Services often earning more miles per dollar than accommodations. This encourages cross-sell and increases customer value.

Large events serve as a growth engine:

Milan and Cortina 2026 Winter Olympics: around 200k guests via Airbnb, +30% supply in host regions, around a billion impressions via global and local campaigns, and dozens of meetings with politicians and cities.

FIFA World Cup 2026: the company is expecting the biggest event in the platform's history - already more than 100k new homes across 16 host cities have registered for the first time just for the championship.

The 2026 outlook and why the stock is up 1.4% after the results

For Q2 2026, Airbnb is projecting revenue of $3.54-3.60 billion, implying 14-16% y/y growth (about 3 percentage point FX tailwind). The company expects GBV to grow in "low double digits" - driven by both continued growth in Nights and Seats and slightly higher ADR. Nights growth is set to slow a bit vs Q1 due to the c.100bp negative impact of the Middle East, but Adjusted EBITDA and margins should both be up YoY.

For the full year 2026, management raises guidance: it expects revenue growth to "accelerate into the low-to-mid teens" and Adjusted EBITDA margin to be at least 35%. It also says it will continue to invest in effective marketing, international expansion and AI - i.e. to maintain a balance between growth and profitability, but without reverting to "growth at any cost".

The stock is responding to this with a modest rise (c. 1.4%) as the market got it:

earnings above the upper end of the range

better than expected GBV growth

improving margins and very strong FCF

and, most importantly, increased full-year revenue and margin growth guidance

At the same time, there are no "red flags": cancellations due to the Middle East are managed, take rate is stable, and while the company is simplifying the fee structure (moving some hosts to a single service fee of 15.5%), it is doing so in a way that hosts maintain net earnings and guests see the full price transparently.